Executive Summary

- Small Finance Banks (SFBs) in India, established by the Reserve Bank of India (RBI) to promote financial inclusion, demonstrated significant growth in revenue and profitability in 2023. There are 12 SFBs, four publicly listed, reflecting investor confidence. Regulatory guidelines ensure their adherence to capital adequacy and governance norms.

- Initiatives promoting digitalization include Pradhan Mantri Jan Dhan Yojana (PMJDY), Unified Payments Interface (UPI), and Aadhaar-based services have furthered financial inclusion. SFB are crucial in this effort, with 67% of their total loan book focused on microfinance.

- In contrast, the UK lacks a dedicated Small Finance Bank sector but supports financial inclusion microfinance and SME banking. Microfinance institutions in the UK, with diverse ownership, have made significant impacts. Success stories from Grameen Bank UK, Big Issue Invest, and Fair Finance illustrate positive impacts.

Industry Challenges

- Though SFBs in India are expanding, particularly in semi-urban and urban areas, reaching underbanked rural centers remains challenging. Success stories from Ujjivan and Equitas highlight positive impacts, but challenges such as the digital divide, cybersecurity risks, and regulatory compliance persist.

- The UK’s regulatory environment, led by the Financial Conduct Authority (FCA), supports microfinance initiatives. The Open Banking framework encourages digital solutions. However, challenges include funding limitations, high operating costs, and barriers to digital adoption.

Outlook

- The outlook for SFBs in India is optimistic, driven by efforts in financial inclusion, digital transformation, collaboration with fintech, regulatory support, and enhanced risk management. These factors position SFBs to contribute to India’s banking ecosystem.

- In the UK, microfinance institutions are expected to increasingly embrace digitalization, collaborate with fintech, and focus on sustainable and responsible lending practices. Regulatory bodies will likely support innovation, fostering a conducive environment for the growth of microfinance.

Table of Contents

| S. No. | Topic | Page no. |

| 1 | Introduction | 4 |

| 2 | Small Finance Banks – Overview & Digital Transformation | 5-9 |

| 2.1 | Scope of Digitalization in SFBs | 6-8 |

| 2.2 | Challenges in Digital Transformation | 8-9 |

| 3 | Global Small Finance & Microfinance Overview | 9-16 |

| 3.1 | Global Microfinance and SME Banking Outlook | 10-12 |

| 3.2 | Case of Europe | 12-13 |

| 3.3 | Case of Africa and Latin America | 13-14 |

| 3.4 | Case of Asia | 14-16 |

| 4 | Digitalization in Small Finance Banks – India | 16-24 |

| 4.1 | Overview of SFBs in India | 16-17 |

| 4.2 | Initiatives and Policies Promoting Digitalization | 17-18 |

| 4.3 | SFBs and Financial Inclusion | 18-21 |

| 4.4 | Success Stories and Case Studies | 22 |

| 4.5 | Challenges and Limitations | 23 |

| 4.6 | SFB Outlook in India | 24 |

| 5 | Digitalization in SFB & Microfinance – UK | 25-29 |

| 5.1 | Overview of Small & Microfinance in the UK | 25-26 |

| 5.2 | Regulatory Environment and Support for Digitalization | 26-27 |

| 5.3 | Success Stories and Case Studies | 27-28 |

| 5.4 | Challenges and Limitations | 28 |

| 5.5 | Small Finance & Microfinance Outlook in the UK | 28-29 |

| 6 | Conclusion | 30-31 |

| 7 | Bibliography | 32-35 |

| 8 | Appendix | 36 |

Introduction

The rise of Small Finance Banks (SFBs) in India marks a pivotal development in the financial landscape, spearheaded by the Reserve Bank of India’s (RBI) bold initiative to advance financial inclusion. These specialised banks serve the critical banking needs of underserved and unbanked segments, including small businesses, micro and small industries, and marginalised individuals. Simultaneously, the global financial landscape has experienced a notable surge in the prominence of microfinance and Small and Medium-sized Enterprise (SME) banking. Worldwide, microfinance institutions have played essential roles in delivering financial services to individuals who traditionally lacked access, fostering entrepreneurship, and driving poverty alleviation. Likewise, SME banking has become vital for supporting the growth of small enterprises, contributing to economic development (Meyer, 1998).

This global rise in Microfinance and SME banking is also evident in developed economies such as the United Kingdom – where rapid FinTech advancements have enabled substantial digital transformation, benefitting small businesses. In this evolving financial landscape, the transformative power of digital technology emerged as a common uniting the rise of SFBs, global microfinance, and SME banking. Digitalisation brings challenges and opportunities, reshaping how these financial segments operate.

Digital transformation has the potential to revolutionise SFBs operations, making financial services more accessible and efficient. The global microfinance sector stands in the brink of a digital revolution, with technology offering new avenues to reach unbanked populations and streamline operations. Furthermore, SME banking globally is undergoing a paradigm shift, with digital tools enabling faster credit assessments, enhanced financial management, and innovative solutions tailored to the needs of small businesses.

This policy paper sets the stage for a thorough exploration of how Small Finance Banks in India, and small finance initiatives in the UK are evolving under the umbrella of digital transformation. It also assesses how global microfinance initiatives and SME banking worldwide navigate digitalisation’s transformative impact. The paper delves into these sectors’ strategies to leverage digital tools to enhance financial inclusion, facilitate entrepreneurship, and contribute to economic growth. Through this exploration, we aim to provide actionable insights and recommendations to policymakers, financial institutions, and stakeholders dedicated to fostering a more inclusive and dynamic financial ecosystem.

Small Finance Banks – Overview & Digital Transformation

Small Finance Banks (SFBs) are specialized financial institutions established by the Reserve Bank of India (RBI) to address the banking needs of underserved and unbanked population segments, particularly in rural and semi-urban areas. These banks aim to promote financial inclusion by catering to small businesses, micro and small industries, and marginalized individuals in the unorganized sector.

SFBs primarily target unserved and underserved segments, including small and marginal farmers, often operating with an initial focus on specific districts or states. They offer a range of basic banking services, including savings accounts, fixed deposits, and credit facilities, aiming to meet the financial needs of low-income groups. Governed by the RBI’s regulatory framework, Small Finance Banks must adhere to guidelines that ensure financial stability and consumer protection (Joshi et al., 2021).

Various entities, including non-banking financial companies (NBFCs) and microfinance institutions, can promote these banks. The introduction of SFBs aligns with India’s broader financial inclusion agenda, striving to integrate a larger portion of the population into the formal banking system and provide them with essential financial services. These banks focus on providing basic banking services such as deposits, loans, remittances, and payment services to small business enterprises, low-income households, and individuals with limited access to formal banking services (Singh and Wasdani, 2016).

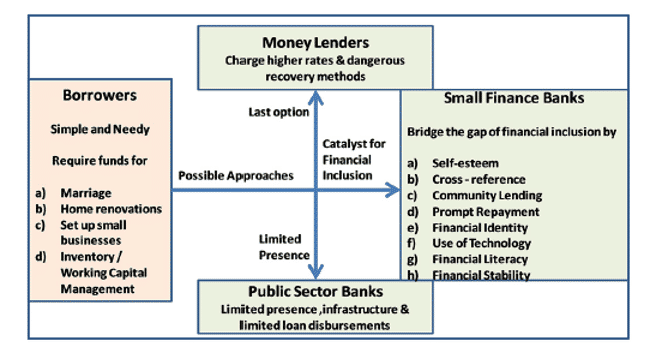

Figure 1 provides an overview of how SFBs cater to needy borrowers, highlighting how these banks bridge the gap in financial inclusion through initiatives and tools such as community lending, financial literacy, financial stability, and cross-referencing (Joshi et al., 2021). SFBs play a vital role in fostering economic growth and enhancing financial stability among the most vulnerable populations by focusing on these critical areas.

These banks have several associated pros and cons. They play a pivotal role in advancing financial inclusion by targeting underserved and unbanked populations, particularly in remote and rural areas. Their tailored approach focuses on specific customer segments, such as small businesses, micro and small industries, and low-income individuals, allowing for customized products and services that meet the unique needs of these customers. SFBs facilitate credit access for small borrowers who may encounter difficulties securing loans from traditional banks, empowering entrepreneurs, and contributing to local economic development. With a more flexible operational structure compared to larger banks, SFBs exhibit agility in adapting to evolving market conditions and meeting customer demands (Ravikumar, 2019).

Scope of Digitalization in SFB’s

Digitalization plays a crucial role in the growth and operational efficiency of Small Finance Banks (SFBs). Digital platforms enable SFBs to extend their services to remote areas where establishing physical branches may not be viable. Through mobile banking apps, internet banking, and other digital channels, these banks can reach customers in geographically dispersed locations, fostering financial inclusion. Digital transformation empowers SFBs to provide seamless and personalized banking experiences to their customers. Self-service functionalities, 24/7 accessibility, and personalized offerings through digital channels enhance convenience, improve satisfaction, and build long-term relationships (Gogisetti, 2021).

Operational efficiency is significantly improved as digitalization streamlines the internal operations of SFBs. Automating processes, reducing manual errors, and optimizing resource utilization through digital platforms lead to cost savings and improved productivity. Efficient loan origination, automated risk assessment, digital onboarding, and real-time transaction monitoring are facilitated by digital platforms (Kangayan and Dhevan, 2020).

Digital technologies also open up avenues for SFBs to introduce innovative banking products and services, driving product and service innovation. These innovations include digital payment solutions, micro-loans through mobile wallets, simplified remittance channels, and customized financial planning tools. Such innovations cater to the specific needs of target customer segments and further drive financial inclusion.

The scope of digitalization among SFBs in India is significant and encompasses various aspects. These banks actively embrace digital technologies to enhance their operations, improve customer experiences, and increase efficiency. SFBs leverage digital channels to facilitate the onboarding process for new customers, including online account opening, e-KYC (Know Your Customer) processes, and the use of digital signatures to streamline account initiation (Kumar, 2023).

Mobile banking applications developed by SFBs offer a range of banking services through smartphones, including balance inquiries, fund transfers, bill payments, and mobile-based authentication for secure transactions. Internet banking and online lending platforms enable customers to access and manage their accounts through web-based interfaces, providing a convenient way to perform various banking transactions without visiting physical branches. Online lending platforms simplify and expedite loan application and approval processes, allowing for quicker credit assessments and disbursements.

SFBs also actively participate in the digital payments ecosystem in India by integrating with popular payment systems such as Unified Payments Interface (UPI), mobile wallets, and other electronic payment methods to facilitate seamless and cashless transactions (Sharma, 2023).

In summary, digitalization not only enhances the reach and operational efficiency of SFBs but also enables them to innovate and offer tailored services that meet the unique needs of their target customers, thereby advancing financial inclusion and economic development.

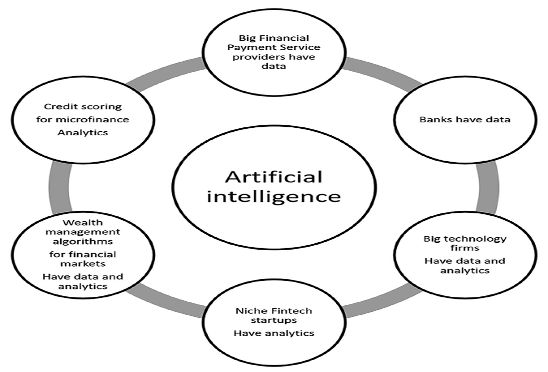

In line with the FinTech revolution, Small Finance Banks (SFBs) increasingly leverage data analytics and artificial intelligence (AI) to gain insights into customer behaviour, personalize services, and enhance risk management. Data-driven decision-making enables SFBs to tailor products to meet the specific needs of different customer segments. While less widespread than in some other sectors, some financial institutions, including SFBs, are exploring the potential applications of blockchain technology for secure and transparent transactions, particularly in areas like remittances and supply chain finance. As digitalization increases, SFBs are also investing in robust cybersecurity measures to protect customer data and ensure the integrity and confidentiality of digital transactions (Kumar, 2023). Figure 2 provides examples of AI’s impact on financial markets, highlighting benefits for the SFB sector and the broader industry.

At the heart of it all, digitalization is a game-changer, a pivotal enabler for advancing financial inclusion. SFBs are at the forefront of this digital revolution, utilizing digital channels to bridge the gap and reach remote and underserved areas. They are providing basic banking services to individuals who may not have easy access to physical bank branches. Moreover, SFBs are actively exploring the feasibility of integrating with third-party services and fintech companies through Application Programming Interfaces (APIs) to broaden their service offerings and provide customers with a more comprehensive range of solutions (Raj and Upadhyay, 2020). By harnessing the power of FinTech, SFBs can significantly improve their operational efficiency, enhance customer experiences, and drive financial inclusion, thereby playing a crucial role in the overall economic development.

Challenges in Digital Transformation

Despite the impressive growth and digital transformation of Small Finance Banks (SFBs) in India and similar institutions worldwide, several barriers and hurdles pose significant threats to their overall advancement. One of the primary challenges is the digital divide. Despite progress in digital infrastructure, segments of the population still have limited access to digital devices, internet connectivity, and digital literacy. Bridging this digital divide and ensuring equal access to digital banking services remains a formidable challenge for SFBs. Upgrading technological infrastructure to support digital transformation is another significant challenge. This includes implementing robust core banking systems, developing user-friendly mobile and online banking platforms, and ensuring seamless integration. Building and maintaining reliable, scalable technological infrastructure require substantial investments and expertise (Singh and Wasdani, 2016).

With increased digital interactions, the risk of cyber threats and data breaches also escalates. SFBs need to implement robust cybersecurity measures to protect sensitive customer information and ensure secure digital transactions. They must invest in advanced security technologies, conduct regular security audits, and educate both customers and employees about cybersecurity best practices (Gogolin et al., 2021).

Consumer-centric issues also present significant hurdles. Encouraging customers to adopt digital banking channels and change their behaviour from traditional banking methods can be challenging. Some customers may be resistant to change, preferring face-to-face interactions and physical branches. SFBs need to invest in customer education and awareness campaigns to promote the benefits and convenience of digital banking and address any concerns or barriers to adoption. Regulatory compliance presents additional challenges. Digital transformation in SFBs brings new regulatory challenges, including compliance with data protection laws, anti-money laundering (AML) regulations, and Know Your Customer (KYC) requirements. Navigating these regulations in the digital space is crucial to maintaining trust and legal compliance (Viritha and Mariappan, 2016).

Finally, integrating legacy systems with new digital solutions poses a significant technical challenge. Many SFBs still rely on legacy systems that may not be easily compatible with modern digital platforms and applications. Integrating these systems with new digital solutions can be complex and time-consuming. SFBs need to carefully plan and execute their digital transformation strategies to ensure seamless integration.

These challenges are not unique to India but are prevalent in SFB alternatives around the world, notably in Microfinance and SME institutions. Overcoming these barriers is essential for SFBs to fully realize the benefits of digital transformation and continue their mission of advancing financial inclusion and economic development.

Global Small Finance – An Overview

Small finance banks (SFBs) are a specific category of financial institutions that exist primarily in India. They are established with a focus on financial inclusion and serving underserved segments. The concept of SFBs is unique to the Indian banking landscape and is designed to cater to the needs of small businesses, micro and small industries, and marginalized individuals who often lack access to traditional banking services.

However, various countries have financial institutions with similar objectives, often called microfinance banks or institutions. These entities aim to promote financial inclusion and provide essential financial services to underserved populations, though they may not share the same regulatory structure as Small Finance Banks in India. For instance, microfinance institutions worldwide have played pivotal roles in delivering financial services to those traditionally excluded from the formal banking sector, fostering entrepreneurship and contributing to poverty alleviation. To understand the structures and operations of these institutions, it is essential to explore the systems of SMEs (Small and Medium-sized Enterprises) and microfinance, along with their respective digital integration capabilities.

In the context of digital integration, SME and microfinance institutions globally are increasingly leveraging technology to enhance their operations, improve customer experiences, and expand their reach. Digital transformation enables these institutions to provide various services, from digital payments and online lending to mobile banking and digital wallets. By embracing digital solutions, they can overcome traditional barriers to financial inclusion, such as geographic limitations and lack of physical infrastructure.

Global Microfinance and SME Banking Outlook

Microfinance and SME Banking: A Global Perspective

The global microfinance market was estimated at USD 200 billion in 2022 and is projected to grow at a CAGR of 12.3%, reaching USD 506 billion by 2030 (Globe Newswire, 2023). Microfinance banks increasingly adopt digital financial services to reach underserved and unbanked populations. This includes digital wallets, mobile banking apps, and other electronic channels to provide clients convenient access to their financial services. Many microfinance banks are implementing digital onboarding processes, including electronic Know Your Customer (e-KYC) procedures, allowing for smooth and efficient customer acquisition while complying with regulatory requirements (Ashta, 2018).

Digital Transformation in Microfinance

Microfinance institutions worldwide leverage mobile banking solutions and Unstructured Supplementary Service Data (USSD) technology to offer basic banking services, especially in regions with limited smartphone penetration. Digitalization streamlines loan application and approval processes, with online loan applications, automated credit scoring, and quick disbursement mechanisms enhancing efficiency and reducing turnaround (Fersi et al., 2023).

Another significant impact of digitalization on the industry is using digital credit scoring. Microfinance banks are exploring models that utilize alternative data sources, such as mobile phone usage patterns and payment histories, to assess the creditworthiness of individuals lacking traditional credit histories. Digitalization enables microfinance banks to harness analytics and intelligence tools, gaining insights into client behaviours and portfolio performance for informed decision-making (Geeta and Sivanand, 2020).

Some microfinance banks partner with fintech companies to leverage technological expertise. These partnerships may involve integrating with digital payment platforms, collaborating on innovative financial products, or adopting fintech solutions to enhance operational efficiency. The overarching goal of digitalization in microfinance is to further financial inclusion. Digital channels enable microfinance banks to reach clients in remote and underserved areas, overcoming geographical barriers and providing essential financial services (Dorfleitner et al., 2022).

SME Banking: Digital Transformation and Growth

SME Banking is another format similar in nature and purpose to Small Finance Banking, with growth and sustainability significantly influenced by fintech and digitalization. The global SME market is well-suited for digital transformation, valued at around USD 350 billion globally in annual revenues, with significant growth potential in emerging markets (Miles, 2023). Research explores the diversity of SME financing, spanning productivity, region, theoretical setup, methodological design, and themes. Meyer (1998) suggests that post-crisis banking regulations limited SME access to finance, leading to non-bank financing alternatives. Temelkov et al. (2018) observed increased lending to small businesses by finance companies and fintech lenders after the 2008 financial crisis. Hryckiewicz et al. (2022) discussed the impact of digitalization on SMEs’ access to credit and its cost, finding a positive effect on access but a non-linear impact on credit costs. Abbasi et al. (2021) explored the positive association between fintechs and SME efficiency, moderated by culture.

Embracing Digital Technologies in SME Banking

The scope of digitalization in SME banking worldwide is substantial, reflecting a global trend towards leveraging digital technologies to enhance business services. Similar to microfinance institutions, SME banks are embracing several tech-enabled features in their operations, such as digital onboarding, online banking platforms, mobile banking apps, and digital payments. These solutions enhance transaction speed and efficiency.

SME finance institutions also utilize data analytics, AI, blockchain technology, and fintech partnerships to enhance their value proposition. Beaumont et al. (2022) highlighted how fintech platforms improve SME credit access by alleviating collateral constraints. In a financial landscape where SMEs often struggle with limited access to finance from conventional banking structures despite significant employment contributions (Rao et al., 2023), SME finance addresses this demand. Education, gender, and ethnicity can further constrain SMEs and small businesses, underscoring the need for dedicated SME banking (Irwin and Scott, 2010). Gopal and Schnabl (2022) examined the positive association between fintechs and SME efficiency, further influenced by cultural factors.

In summary, while SFBs are unique to India, similar models like microfinance and SME banking globally demonstrate the significant role of digitalization in enhancing financial inclusion and operational efficiency. These institutions are crucial in supporting small businesses and underserved populations, driving economic development through innovative digital solutions.

Case of Europe

Europe’s financial services industry is arguably dominated by legacy banks and conventional financial institutions which have maintained a firm foothold over centuries. However, the rise of microfinance and SME banking in Europe has been a notable trend in recent years, driven by a growing recognition of the crucial role that small and medium-sized enterprises (SMEs) play in fostering economic development and employment. European financial institutions have increasingly focused on expanding financial services tailored to the unique needs of micro-entrepreneurs and SMEs. Microfinance, characterized by small-scale lending to individuals and micro-businesses, has gained traction as a tool for promoting financial inclusion. Additionally, SME banking has witnessed advancements in digitalization, with the adoption of online platforms, mobile banking, and fintech solutions to enhance accessibility and efficiency (Pytkowska, 2020; Wagenvoort, 2003). Figure 3 elaborates on the increased dependency on alternative finance among small businesses in Europe – highlighting a growing appetite for Microfinance and SME banking (Lu, 2018).

While acknowledging the necessity for increased digital integration, Pytkowska and Korynski (2017) recorded varying levels of ability and willingness among MFIs to embrace these technologies. Small institutions often cite a lack of financial resources as a primary challenge hindering technological advancements. The survey highlights that the most valued digital services are those automating loan applications and related documentation management. The small scale of operations within many European MFIs acts as a barrier to the widespread implementation of fintech solutions.

Case of Africa and Latin America

Microfinance and SME banking are prevalent in South America and Africa. BancoSol, one of the earliest microfinance banks in Latin America, operates in Bolivia and has successfully provided financial services to underserved populations, including micro-entrepreneurs (Gonzalez-Vega et al., 1996). Similarly, Equity Bank in Kenya is a notable example of a bank with a strong focus on financial inclusion. Although it is not classified as a Small Finance Bank, Equity Bank has implemented strategies to reach unbanked and underbanked populations, offering low-cost banking services as a key strategy to expand its customer base (Kiganda, 2014).

The combination of microfinance and small business finance in two of the most underdeveloped continents—Africa and Latin America—can provide a much-needed boost to economic growth through several factors. The key contributions of these alternative finance avenues include:

- Financial Inclusion: Expanding access to financial services for underserved populations.

- Entrepreneurship Development: Supporting the growth of small businesses and micro-entrepreneurs.

- Poverty Alleviation: Providing financial resources to those in need, fostering economic stability.

- Women Empowerment: Enabling women to access financial services and promoting gender equality.

- Community Development: Investing in local communities and supporting their development.

- Social Impact: Creating positive social changes through improved financial access and stability.

Digitalization of these services can accelerate the realization of these positive contributions, particularly in financial inclusion. However, the pace of digitalization and fintech growth in these regions depends on infrastructural advancements and technological improvements brought about by increased funding (Dapp, 2017). The continued development of digital infrastructure is crucial for maximizing the impact of microfinance and SME banking in Africa and Latin America.

Case of Asia

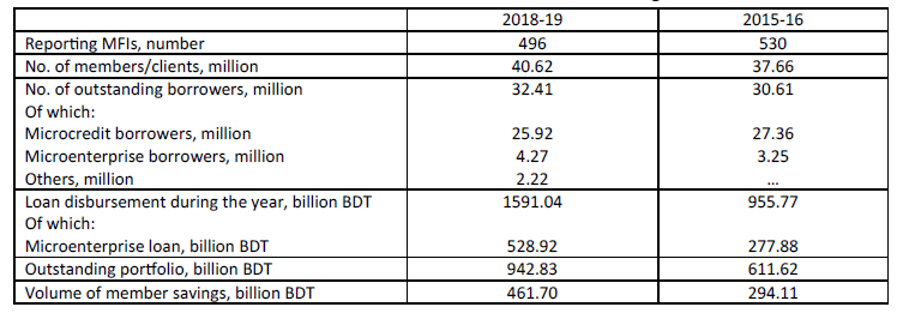

Asia is an established hub for Microfinance and SME banking – as well as being an emerging FinTech giant. One of the key examples of the former is Bangladesh, a country which pioneered one of the earliest and most successful microfinance institutions in Grameen Bank. It was founded by Muhammad Yunus and is known for pioneering microcredit and microfinance to support rural entrepreneurs, particularly women, in lifting themselves out of poverty. Bangladesh has a microfinance and small banking sector poised for growth and profitability, as evidenced in Table 1. Despite a fall in the number of microfinance institutions, the numbers of members, borrowers, loan amounts and total portfolio value have all grown over the four-year period from 2015 to 2019.

Mujeri (2020) provides a comprehensive analysis of the growth of microfinance and small finance banking in the era of digital transformation. The paper’s key findings suggest a promising future for these sectors in the FinTech era. It identifies three crucial aspects for microfinance institutions (MFIs) in the post-COVID-19 period:

- Innovative and Sustainable Measures: Implementing new and sustainable approaches to address financial constraints.

- Tailored Financial Products and Services: Developing financial products and services designed explicitly for excluded poor households and micro businesses.

- Efficient Operations through Technology: Ensuring efficient and cost-effective operations using digital and modern technologies.

The considerations for MFIs include determining where to begin the digitization process, assessing their readiness for digital transformation, and evaluating the challenges and risks associated with this journey. The post-COVID-19 era is an opportunity for MFIs to embrace digital transformation fully.

The relevance of digital transformation in microfinance and small banking is further underscored by case studies from China and Vietnam. Dang and Vu (2020) provide insights into the challenges faced by MFIs in Vietnam and how fintech activities can address these. Their findings demonstrate the positive outcomes of fintech application in the microfinance sector, including improved product and service quality, enhanced access to diverse customer groups, and expansion of operational models.

Zreik et al. (2023) focus on China, investigating the impact of microfinance’s impact on small business owners, particularly microcredit. Their study underscores the significance of digital transformation in microfinance, emphasizing the need for effective digitization strategies to improve access to financial services for underprivileged communities. It also highlights the crucial role of regulatory policies.

Digital Revolution and Microfinance: Challenges and Opportunities

The digital revolution has a significant impact on the microfinance and small finance sectors globally, albeit with its own set of challenges. A closer look at the UK and India provides valuable insights. While India has a dedicated category for Small Finance Banks, the UK does not. However, by examining the microfinance and SME banking sectors in the UK, we can gauge the digital potential of small finance in the country.

In summary, the worldwide push towards digital transformation in microfinance and small finance banking presents significant opportunities for enhancing financial inclusion and service delivery. However, it also requires careful consideration of different regions’ unique challenges and regulatory environments. The experiences of countries like Vietnam and China and the evolving landscapes in the UK and India offer valuable lessons for navigating this complex yet promising frontier.

Digitalization in Small Finance Banks – India

Overview of SFBs in India

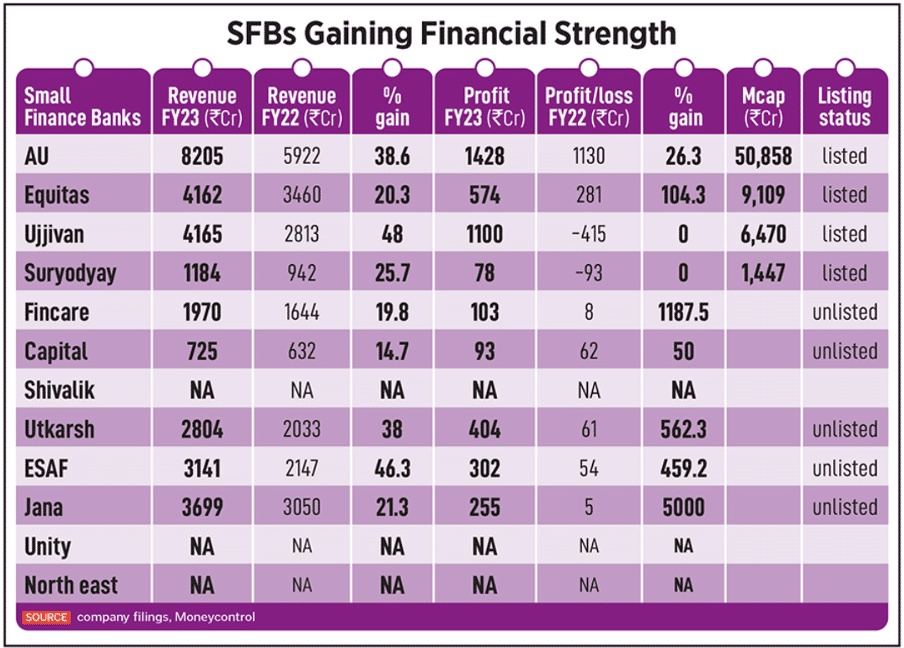

In India, Small Finance Banks (SFBs) were established as part of the Reserve Bank of India’s (RBI) efforts to promote financial inclusion and provide banking services to the underserved sections of society. SFBs are licensed banks that focus on meeting the banking needs of micro and small enterprises, small farmers, low-income households, and other unbanked or underbanked individuals. As of 2023, there are a total of 12 SFBs operating in India, a list included below along with their respective financial performance indicators.

From the snapshot provided below, it can be gauged that the SFB sector has recorded substantial revenue increments in 2023 as compared to 2022. In addition, profitability in 2023 has also been higher as compared to the previous year. Four of the SFB’s (AU, Equitas, Ujjivan, Suryodyay) are also market listed, with impressive capitalisation figures highlighting investor confidence in the SFB sector (Srivastava and Panchal, 2023). These banks are required to adhere to regulatory guidelines set by the RBI and follow prudential norms related to capital adequacy, risk management, and governance.

Initiatives and Policies Promoting Digitalization

In 2015, RBI issued licenses for a new type of bank, called the Small Finance Bank (SFB), to ten applicants engaged in providing financial services. RBI has designed the SFB license with specific business-model-level regulatory prescriptions– SFBs are required to dedicate 75% of their Adjusted Net Bank Credit (ANBC) to priority sector lending and must have at least 50% of their lending portfolio be comprised of loans and advances of up to INR 25 lakhs (2,500,000) each. There are differences in the capital requirement as well for SFBs, among other things – the minimum paid-up capital cannot be below INR 100 Cr (1.0 Bn) (one-fifth that of universal banks), and the minimum capital-to-risk-weighted-assets ratio must not be below 15% (more than 1.5 times that of universal banks) (RBI, 2016). A list of relevant regulations is provided in the appendix.

The Indian government and the RBI have implemented various initiatives and policies to promote digitalization in Small Finance Banks and the banking sector as a whole. Some key initiatives are as below.

- Pradhan Mantri Jan Dhan Yojana (PMJDY): Launched in 2014, this program aims to provide every Indian citizen with access to a bank account. PMJDY facilitates the digitalization of banking services and promotes financial inclusion by offering no-frills accounts, debit cards, and access to various banking services (Sharma, 2023).

- Unified Payments Interface (UPI): UPI is a real-time payment system introduced by the National Payments Corporation of India (NPCI). It enables instant fund transfers between bank accounts using mobile phones. SFBs actively participate in the UPI ecosystem, offering UPI-based payment solutions to their customers (Mohanty, 2018).

- Aadhaar-based Services: Aadhaar, India’s unique identification system, plays a crucial role in digitalizing banking services. SFBs leverage Aadhaar for e-KYC (Know Your Customer) verification, enabling customers to open bank accounts digitally without visiting physical branches (Ravikumar, 2019).

SFBs and Financial Inclusion

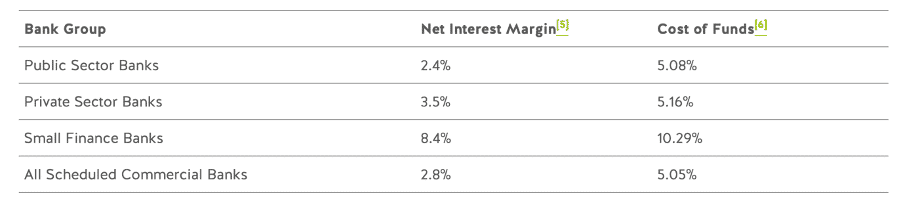

SFBs have largely done well in maintaining profitability despite the more stringent regulatory mandates on PSL and loan sizes. This has been driven by the high spread between deposit and lending rates and holds despite their cost of funds being double that of public and private sector banks (Mohanty, 2018; Raj and Upadhyay, 2020).

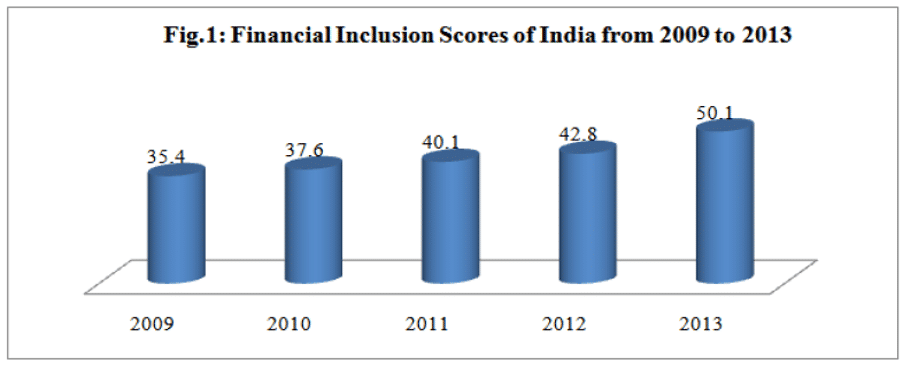

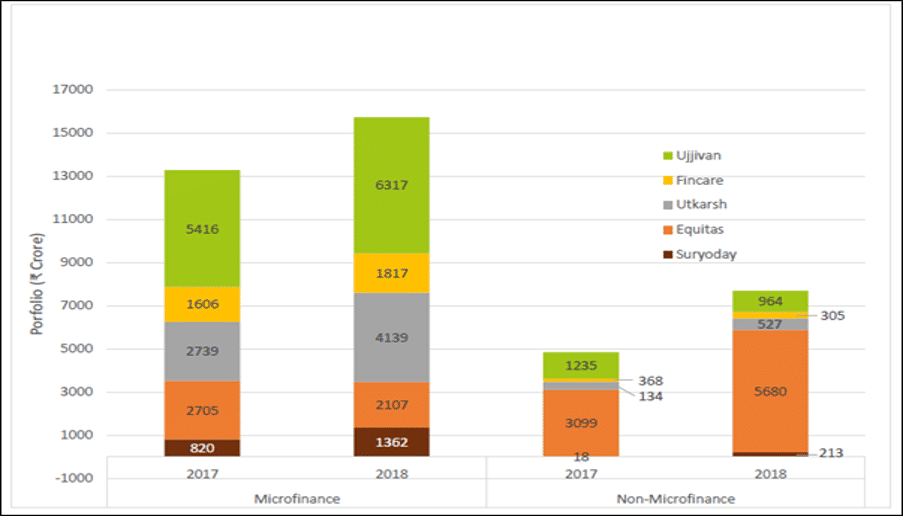

Microfinance still forms a sizeable portion of the loan book for SFBs, this is likely to contribute to keeping the portfolio-level lending rates higher than that of other bank groups. Figure 1 shows the microfinance and non-microfinance components for the five SFBs for which this data was available. Microfinance book formed 67% of the total loan book for these five SFBs. Rising score of financial inclusion in India is illustrated in Figure 4, demonstrating an impact of several improvements in the financial services industry – with substantial contributions made by the Microfinance and SFB sectors (Mohanty, 2018).

The trends in financing preference among small finance banks in India for Microfinance and Non-Microfinance is substantiated in Figure 5. As can be inferred from the data, there is a preference among SFB institutions to provide financing to borrowers of the microfinance category than to those in the non-microfinance segment – although there are gains across both segments. It further augments the critical role the SFB sector plays in promoting financial inclusion among small businesses across the country.

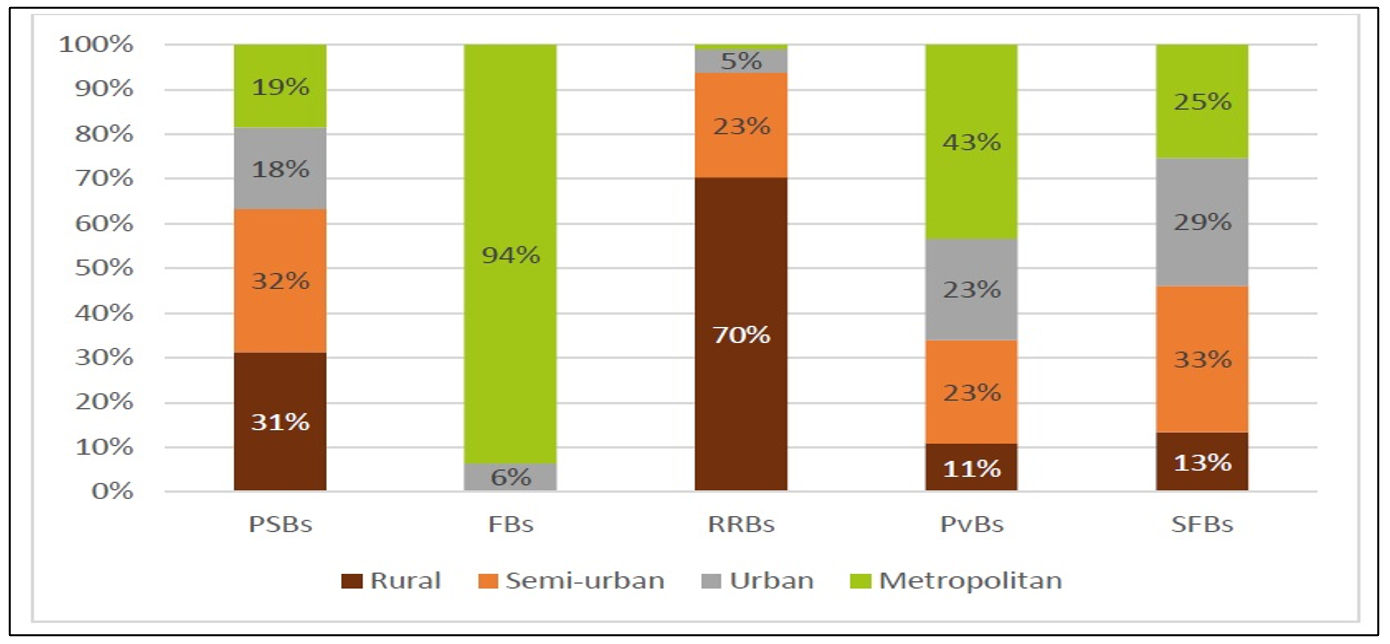

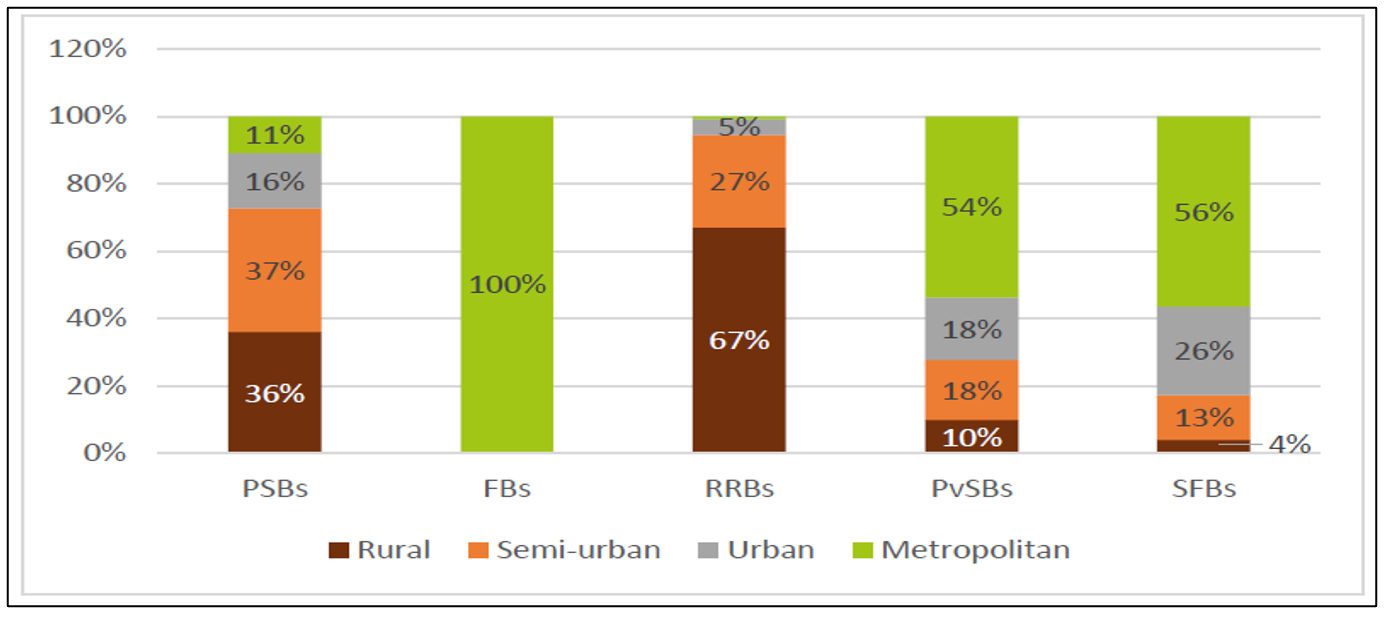

The increase in the non-microfinance component has been through the provision of new products, with MSME, vehicle and gold loans being the most common ones. SFBs’ strategy and expansion seem most akin to that of private sector banks. Much of the SFB branch network (62%) is in the semi-urban and urban areas. SFB lending and to an extent deposit-taking, does not see rural centres being serviced more than what is already being done by existing banking models (except for RRBs) (Figures 6 and 7). SFBs’ credit picture sees a geographic skew with only 17% of credit accounts and 20% of credit amount in the rural and semi-urban areas.

Assessing whether the SFBs have met their mandate of serving the underserved or not can be done by looking at how many of the unbanked centres are now being served by the SFBs. However, the publicly available data is limited to the locations which are ‘banked’, i.e., have at least one operational bank branch. Therefore, to analyse the reach of the SFBs, we adopt a different metric for locations – ‘underbanked’ for those locations which have five or fewer bank branches. The share of SFB branches in underbanked locations constitutes only 21% of their total bank branches. The highest such proportion is that of Regional Rural Banks at 76% (Neelam, 2019). While this highlights a need for considerable improvement via investment in rural areas across the country – there is progress to show via penetration into rural areas which promote overall financial inclusion. These indicators paint a promising picture of enhanced micro credit access and financing access by small businesses and individual borrowers all over India. These advances are poised to benefit from digital expansion and digital infrastructure improvements in India. Already the SFB sector constitutes a large share

Considering the SFBs’ choice of business and expansion strategy, it thus brings to question how well the business-model-level regulatory prescriptions help in fulfilling a financial inclusion mandate. A deeper analysis with more and better data that can give a granular understanding of benefits at the customer level is required to understand how many of the previously unbanked/underbanked populations are being catered to by SFBs.

Success Stories and Case Studies

There have been several success stories and case studies highlighting the positive impact of digitalization in Indian Small Finance Banks. A few noteworthy examples are as below.

- Ujjivan Small Finance Bank

Ujjivan Small Finance Bank is one of the prominent small finance banks in India. It focuses on providing financial services to the unbanked and underbanked segments of society, including micro and small enterprises, low-income individuals, and women entrepreneurs.

Case Study: Ujjivan Small Finance Bank supported Ramesh, a small-scale farmer in a rural village. Ramesh wanted to expand his agricultural business but lacked access to formal credit. Ujjivan Small Finance Bank offered him a small loan with reasonable interest rates, along with financial literacy training. With the loan, Ramesh invested in modern farming techniques, purchased quality seeds, and increased his productivity. As a result, his income improved significantly, and he was able to provide a better life for his family (Abrar, 2023).

- Equitas Small Finance Bank

Equitas Small Finance Bank is known for its focus on serving the urban and rural low-income population through various financial products and services. They emphasize financial inclusion and aim to empower individuals with financial resources and tools.

Case Study: Equitas Small Finance Bank assisted Sunita, a micro-entrepreneur running a small tailoring business from her home. Sunita had limited capital and lacked access to formal banking services. Equitas Small Finance Bank provided her with a microloan to purchase a sewing machine and raw materials. They also offered financial literacy training and guidance on marketing her products. With the support of Equitas, Sunita expanded her business, gained more clients, and improved her income, ultimately leading to financial stability for her family (Agarwal, 2023).

These case studies illustrate the positive impact of small finance banks in India, enabling individuals from underserved communities to access financial services and achieve economic empowerment. Small finance banks play a crucial role in providing loans, savings accounts, and other financial products tailored to the specific needs of micro and small enterprises, low-income individuals, and marginalized populations.

Challenges and Limitations

Despite advancements in digitalization, Small Finance Banks (SFBs) in India face significant challenges and limitations in their digital transformation efforts. One major challenge is the digital divide in the country. While digital infrastructure has improved, there are still sections of the population, particularly in rural and remote areas, with limited access to digital devices, internet connectivity, and digital literacy. This creates a barrier to adopting and using digital banking services for a significant portion of the population (Kangayan and Dhevan, 2020).

The increased reliance on digital platforms exposes customers and banks to cybersecurity risks and data breaches. SFBs must invest in robust security measures, including encryption, multi-factor authentication, and regular security audits, to protect customer data and maintain trust in their digital services. Compliance with data privacy regulations, such as the Personal Data Protection Bill, is also crucial. SFBs need reliable and scalable technology infrastructure to support their digital banking operations. This includes robust core banking systems, secure servers, data centres, and uninterrupted connectivity. Upgrading and maintaining such infrastructure can be costly, particularly for small and emerging banks, and requires strategic planning and investment (Singh and Wasdani, 2016).

Promoting digital banking services also requires efforts to enhance digital literacy among customers. Many individuals, especially those from low-income and rural backgrounds, may need to become more familiar with using digital platforms for financial transactions. SFBs must undertake customer education programs to familiarize their target audience with digital banking services and provide practical training on mobile apps, internet banking, and other digital tools (Hardik, 2023).

SFBs operate in a highly regulated environment, and ensuring compliance with various regulations, such as customer identification, transaction monitoring, and data protection, can be complex. Adhering to evolving regulatory frameworks, such as RBI cybersecurity and data localization guidelines, requires ongoing monitoring and investment in compliance infrastructure. Overcoming these challenges and limitations requires a holistic approach involving collaboration between SFBs, regulators, technology providers, and the government. Addressing the digital divide, strengthening cybersecurity measures, investing in technology infrastructure, promoting digital literacy, and maintaining regulatory compliance are crucial steps toward successful digitalization in Indian SFBs (Hardik, 2023).

SFB Outlook in India

The future outlook for small finance banks in India is optimistic, shaped by several factors:

- Increasing Financial Inclusion: SFBs will continue to promote financial inclusion by serving underserved and unbanked populations. These banks will help bridge the gap by providing access to formal banking services, including savings accounts, credit facilities, and other financial products. Government initiatives like the Pradhan Mantri Jan Dhan Yojana will further support the growth of SFBs.

- Digital Transformation: SFBs are expected to undergo further digital transformation, leveraging technology to offer innovative digital banking solutions, such as mobile banking, online account management, and digital payment services. Digital channels enable SFBs to reach remote areas and enhance operational efficiency.

- Expansion of Service Offerings: As SFBs mature, they will likely expand their product and service offerings. Beyond essential banking services, they may diversify into insurance, wealth management, and investment products, catering to the evolving needs of their customer base and providing comprehensive financial solutions.

- Collaboration with Fintech Companies: SFBs will increasingly collaborate to leverage their technological expertise and innovative solutions. Partnerships with fintech firms can enhance digital capabilities, improve customer experience, and offer new services, including efficient loan underwriting and digital credit scoring.

- Regulatory Support: Regulatory bodies like the RBI support SFBs and have introduced measures to promote their growth. Relaxed regulations, like priority sector lending targets, facilitate the expansion of SFBs.

- Focus on Risk Management and Governance: As SFBs grow in scale and complexity, there will be an increased emphasis on risk management practices and robust governance frameworks. Investments in strong risk management systems will contribute to the long-term sustainability and stability of SFBs.

In conclusion, the future of small finance banks in India appears promising, driven by efforts to promote financial inclusion, digital transformation, collaboration with fintech companies, regulatory support, and a focus on risk management and governance. These factors position SFBs to serve as essential pillars of the Indian banking ecosystem, catering to the needs of underserved individuals and contributing to the country’s overall economic growth.

Digitalization in Small Finance Banks – UK

Overview of SFBs in UK

As mentioned earlier, the UK’s need for a dedicated SFB sector prevents a direct comparison with India. However, microfinance and SME banking can be analyzed to gauge the appetite for small business financing in the UK and its future potential in light of the digital revolution. Microfinance, a concept originating from developing countries, has gained traction in the UK to provide financial services to underserved individuals and small businesses.

In the UK, microfinance and SME banks operate as specialized financial institutions catering to the needs of individuals and businesses with limited access to traditional banking services. These banks aim to promote financial inclusion and support economic growth by offering small loans and savings accounts (Cowling et al., 2016). A preference among small businesses, particularly non-family businesses, for external credit financing is showcased in Figure 9. While family businesses may be relatively sceptical about using external funding, there is a growing trend to move away from traditional banking structures and adopt more flexible modes of financing, such as micro and SME banking.

The microfinance sector in the UK comprises a diverse range of institutions, including community development finance institutions (CDFIs), credit unions, and social lenders. These organizations differ in their ownership structure, funding sources, and target customer segments. CDFIs, for example, are nonprofit organizations that focus on lending to disadvantaged communities, while credit unions are member-owned financial cooperatives (Ashta and Herrmann, 2021).

Three prominent microfinance companies in the UK that have had a significant impact in the past:

- Grameen Bank UK: Grameen Bank UK is a microfinance institution that follows the principles of Nobel laureate Muhammad Yunus’s Grameen Bank model. It aims to alleviate poverty and empower disadvantaged individuals by providing them with access to financial services and opportunities to start their own businesses (Banna et. al., 2022).

- Big Issue Invest: Big Issue Invest is a social enterprise that supports small and medium-sized enterprises (SMEs) and social enterprises through access to finance and investments. It offers loans, equity investments, and other financial products to organizations that have a positive social or environmental impact (Disse and Sommer, 2020).

- Fair Finance: Fair Finance is a microfinance company that provides affordable loans and financial advice to individuals and small businesses who may have limited access to traditional banking services. They focus on promoting financial inclusion and supporting the growth of underserved communities and businesses.

Regulatory Environment and Support for Digitalization

The regulatory environment in the UK promotes the growth and stability of microfinance banks while safeguarding consumer interests. The Financial Conduct Authority (FCA) is the primary regulatory body overseeing the operations of microfinance institutions. It sets standards for conduct, prudential requirements, and consumer protection. In the UK, there has yet to be a specific regulatory framework for microcredit. Non-bank lenders, such as community development finance institutions (CDFIs) and credit unions, can lend directly to individuals and businesses. CDFIs operate under the Consumer Credit Act, while several laws regulate credit unions (Lu, 2018; Omarini, 2017).

The UK government and regulatory bodies support digitalization efforts within the microfinance sector, recognizing technology’s potential to enhance access to financial services and improve operational efficiency. Initiatives such as the Open Banking framework have facilitated the integration of digital solutions in microfinance banks, allowing for greater innovation and customer-centric services (Lund and Wright, 1999).

However, the sector faces the challenge of adapting regulations originally designed for large banks that do not proportionally apply to small non-bank lenders. As a response, policy strategies should focus on lobbying for proportionate regulation and building evidence of the negative impact that regulatory burdens impose on microlending and its social impact (Howorth et al., 2003).

Success Stories and Case Studies

The microfinance sector in the UK boasts numerous success stories and case studies that demonstrate the positive impact of microfinance on individuals and small businesses. These stories highlight how microfinance banks have helped entrepreneurs start businesses, provided loans to individuals with limited credit history, and supported community development projects. These success stories inspire and showcase microfinance’s potential to empower underserved populations and stimulate economic growth. Two notable success stories include:

- Five Lamps

Five Lamps is a microfinance company in the UK that provides financial services and support to individuals and businesses in underserved communities. They offer affordable loans, savings accounts, and business support services to help individuals and entrepreneurs achieve their financial goals.

Case Study: Five Lamps supported Jane, a single mother with a passion for baking, in starting her own bakery business. Jane had limited access to traditional financing options due to a lack of collateral and credit history. Five Lamps provided her with a microloan to purchase baking equipment and supplies, and also offered business mentorship and financial management guidance. With Five Lamps’ support, Jane successfully launched her bakery, expanded her customer base, and improved her financial stability (Smith, 2023).

- Responsible Finance

Responsible Finance is a network of community-based finance providers in the UK that promotes responsible lending and financial inclusion. They offer microloans, business support, and financial education to individuals and businesses with difficulty accessing mainstream financial services.

Case Study: Responsible Finance supported Mark, a young entrepreneur with a vision to open a sustainable clothing store. Mark faced challenges in securing funding from traditional banks due to his limited business experience and unconventional business model. Responsible Finance provided him with a microloan, business coaching and mentoring. With their support, Mark successfully launched his sustainable clothing store, attracting environmentally conscious customers and contributing to the community (Gordon, 2023).

Challenges and Limitations

While microfinance in the UK has made significant strides, it also faces challenges and limitations. Limited funding sources, high operating costs, and the need for ongoing regulatory compliance pose challenges to microfinance banks. Additionally, reaching remote and marginalized communities remains a hurdle, requiring innovative approaches and partnerships to ensure access to financial services (Binks and Ennew, 1997; Gordon, 2023).

The digital divide and low levels of financial literacy can limit the adoption and effectiveness of digital banking services. Microfinance banks need to address these challenges by providing financial education, improving accessibility, and tailoring their digital solutions to the specific needs of their target customer segments (Heffernan, 2006).

Outlook for Small Finance and Microfinance in the UK

While the UK may not have a dedicated Small Finance Bank sector like India or other emerging economies, the future outlook for microfinance targeting SMEs and individuals in the UK is promising. This trajectory can be attributed to several factors emphasizing financial inclusion, the acceleration of the FinTech revolution, and regulatory support.

- Continued Emphasis on Financial Inclusion: The UK government and regulatory bodies remain committed to promoting financial inclusion and reducing the access gap. Microfinance institutions will continue to play a vital role in providing financial services to underserved individuals and small businesses, ensuring they have access to capital, savings, and other financial products.

- Integration of Technology: Technology will continue to drive the microfinance sector. Microfinance institutions will embrace digitalization, leveraging innovative technologies such as artificial intelligence, machine learning, and blockchain to enhance operational efficiency, expand service offerings, and improve customer experiences. Adopting digital banking solutions will enable more efficient and convenient access to financial services for microfinance customers.

- Collaboration with FinTech Companies: Microfinance institutions will increasingly collaborate with fintech companies to leverage their expertise and technologies. Partnerships with fintech firms can facilitate the development of innovative solutions, such as alternative credit scoring models, digital lending platforms, and tailored financial advice tools. These collaborations will enhance the effectiveness of microfinance institutions in serving their target customer segments.

- Enhanced Data Analytics: Microfinance institutions will leverage data analytics to gain insights into customer behaviour, preferences, and creditworthiness. Advanced data analytics tools and techniques will enable more accurate risk assessment and personalized product offerings. Microfinance institutions can use these insights to design and deliver customized financial solutions that cater to the specific needs of their customers (Siwale and Godfroid, 2022).

- Regulatory Support and Innovation: The regulatory framework in the UK will continue to evolve to support the growth and innovation of microfinance institutions. Regulatory bodies will likely encourage experimentation and foster a conducive environment for digital innovations in the microfinance sector. Initiatives such as Open Banking will further promote collaboration and integration between microfinance institutions and other service providers (Srinivas and Mahal, 2017).

- Sustainability and Social Impact: Microfinance institutions in the UK will increasingly focus on sustainable and responsible lending practices. There will be a greater emphasis on measuring and reporting social impact, ensuring that microfinance activities contribute to individuals’ and communities’ overall well-being and economic empowerment. Environmental, Social, and Governance (ESG) considerations will play a crucial role in shaping the future direction of microfinance.

Conclusion

In summary, the future of microfinance in the UK looks promising, driven by the integration of technology, regulatory support, collaboration with fintech companies, and a continued emphasis on financial inclusion. By embracing digitalization, leveraging data analytics, and promoting responsible lending practices, microfinance institutions will be well-positioned to positively impact individuals, businesses, and communities across the UK.

Comparative Analysis: Small Finance Banks in India and Microfinance in the UK

Analyzing Small Finance Banks (SFBs) in India provides valuable insights into the sector’s growth and performance, especially in digitalization. As of 2023, the SFB sector has shown substantial revenue increments and increased profitability, with four listed banks (AU, Equitas, Ujjivan, Suryoday) indicating strong market confidence. The regulatory environment, with specific mandates from the Reserve Bank of India (RBI), emphasizes priority sector lending and minimum capital requirements, ensuring compliance with prudent norms.

Digitalization initiatives, influenced by the government and the RBI, have played a crucial role in shaping the SFB landscape. Key policies such as Pradhan Mantri Jan Dhan Yojana (PMJDY), Unified Payments Interface (UPI), and Aadhaar-based services have transformed the sector’s digital transformation. Notably, SFBs have maintained profitability despite stringent regulatory mandates, and microfinance remains a significant component of their loan portfolio, contributing to India’s improving financial inclusion scores.

However, challenges persist, such as the concentration of SFB operations in urban and semi-urban areas, indicating a need for further penetration into rural centres. Assessing their mandate of serving the underserved, SFBs’ reach in underbanked locations remains at 21%, suggesting room for improvement, particularly in rural areas. The success stories of Ujjivan Small Finance Bank, Equitas Small Finance Bank, and others illustrate the positive impact of microfinance on individuals and small businesses.

The challenges in India’s SFB sector include the digital divide, cybersecurity risks, and compliance complexities. To address these, SFBs must invest in digital literacy programs, robust security measures, and scalable technology infrastructure. The outlook for SFBs in India appears optimistic, driven by ongoing efforts for financial inclusion, digital transformation, regulatory support, and a focus on risk management and governance.

In the UK, the microfinance sector has gained traction to support underserved individuals and small businesses. The absence of a dedicated SFB sector prompts an analysis of microfinance and SME banking, which operate as specialized financial institutions promoting financial inclusion. Noteworthy microfinance organizations like Grameen Bank UK, Big Issue Invest, and Fair Finance have demonstrated positive impacts through case studies.

The regulatory environment, overseen by the Financial Conduct Authority (FCA), supports the growth of microfinance institutions in the UK. The Open Banking framework facilitates the integration of digital solutions, enabling innovation and customer-centric services. Success stories from Five Lamps and Responsible Finance highlight the sector’s role in empowering individuals and supporting community development.

Challenges include limited funding sources, high operating costs, and the digital divide. To address these, microfinance institutions in the UK need ongoing efforts in financial education, accessibility improvement, and tailored digital solutions. The future outlook remains promising, driven by a commitment to financial inclusion, technology integration, collaboration with fintech, enhanced data analytics, regulatory support, and a focus on sustainability and social impact.

In summary, the dual analysis of Small Finance Banks in India and microfinance in the UK underscores these institutions’ pivotal role in promoting financial inclusion and supporting economic development. Both regions show promise in leveraging digitalization, regulatory support, and innovative collaborations to enhance the reach and impact of microfinance institutions. Addressing challenges will be crucial for ensuring these financial entities’ sustained growth and positive social impact.

Bibliography

Abbasi, K., Alam, A., Du, M. A., & Huynh, T. L. D. (2021). FinTech, SME efficiency and national culture: evidence from OECD countries. Technological Forecasting and Social Change, 163, 120454.

Abrar, Peerzada (2023). Alternate financing poised to capitalise on $570 bn SME credit opportunity. Business Standard, https://www.business-standard.com/industry/sme/alternate-financing-poised-to-capitalise-on-570-bn-sme-credit-opportunity-123082400815_1.html.

Agarwal, Paak (2023). FINANCIAL INCLUSION THE WAY FORWARD IN NEW-AGE BANKING FOR INDIA’S SMES, STARTUPS. Your Story Financial Report, https://yourstory.com/2023/10/techsparks-new-age-banking-sme-startup-mabel-chacko-hardika-shah.

Ashta, A. (2018). News and trends in Fintech and digital microfinance: Why are European MFIs invisible?. FIIB Business Review, 7(4), 232-243.

Ashta, A., & Herrmann, H. (2021). Artificial intelligence and fintech: An overview of opportunities and risks for banking, investments, and microfinance. Strategic Change, 30(3), 211-222.

Banna, H., Mia, M. A., Nourani, M., & Yarovaya, L. (2022). Fintech-based financial inclusion and risk-taking of microfinance institutions (MFIs): Evidence from Sub-Saharan Africa. Finance Research Letters, 45, 102149.

Beaumont, P., Tang, H., & Vansteenberghe, E. (2022). Collateral Effects: The Role of FinTech in Small Business Lending. In Proceedings of the EUROFIDAI-ESSEC Paris December Finance Meeting.

Binks, M. R., & Ennew, C. T. (1997). The relationship between UK banks and their small business customers. Small business economics, 9, 167-178.

Cowling, M., Liu, W., & Zhang, N. (2016). Access to bank finance for UK SMEs in the wake of the recent financial crisis. International Journal of Entrepreneurial Behavior & Research, 22(6), 903-932.

Dang, T. T., & Vu, H. Q. (2020). Fintech in Microfinance: a new direction for Microfinance institutions in Vietnam. Asian Journal of Business Environment, 10(3), 13-22.

Dapp, T. F. (2017). Fintech: the digital transformation in the financial sector. Sustainability in a Digital World: New Opportunities Through New Technologies, 189-199.

Disse, S., & Sommer, C. (2020). Digitalisation and its impact on SME finance in Sub-Saharan Africa: Reviewing the hype and actual developments (No. 4/2020). Discussion Paper.

Dorfleitner, G., Forcella, D., & Nguyen, Q. A. (2022). The digital transformation of microfinance institutions: an empirical analysis. Journal of Applied Accounting Research, 23(2), 454-479.

Fersi, M., Boujelbéne, M., & Arous, F. (2023). Microfinance’s digital transformation for sustainable inclusion. European Journal of Management and Business Economics.

Geeta, M., & Sivanand, C. N. (2020). Micro Finance and Impact of Digitalization. International Journal of Management (IJM), 11(7).

Globe Newswire (2023). Global Microfinance Strategic Market Report 2023-2030: How Microfinance Can Live Up to Expectations & Unlock a Promising Narrative? FinTech Futures, https://www.fintechfutures.com/techwire/global-microfinance-strategic-market-report-2023-2030-how-microfinance-can-live-up-to-expectations-unlock-a-promising-narrative/.

Gogisetti, D. V. N. R. (2021). ‘Small Finance Banks’,’Payment Banks’,’Challenger Banks’ and’Bad Banks’–Will they Revolutionize the Traditional Banking of India?. Challenger Banks’ and’Bad Banks’–Will they Revolutionize the Traditional Banking of India.

Gogolin, F., Lim, I., & Vallascas, F. (2021). Cyberattacks on small banks and the impact on local banking markets. Available at SSRN 3823296.

Gonzalez-Vega, C., Schreiner, M., Meyer, R. L., Rodriguez-Meza, J., & Navajas, S. (1996). BancoSol: The challenge of growth for microfinance organizations (No. 1209-2016-98497).

Gopal, M., & Schnabl, P. (2022). The rise of finance companies and fintech lenders in small business lending. The Review of Financial Studies, 35(11), 4859-4901.

Gordon, Paul (2023). The top challenges for UK SMEs in 2023. Lloyds Banking Group Report, https://www.lloydsbankinggroup.com/insights/the-top-challenges-for-uk-smes-in-2023.html.

Hardik, N. (2023). Digitalisation promotes adoption of soft information in SME credit evaluation: the case of Indian banks. Digital Finance, 1-32.

Heffernan, S. (2006). UK bank services for small business: How competitive is the market?. Journal of Banking & Finance, 30(11), 3087-3110.

Howorth, C., Peel, M. J., & Wilson, N. (2003). An examination of the factors associated with bank switching in the UK small firm sector. Small Business Economics, 20, 305-317.

Hryckiewicz, A., Korosteleva, J., Kozlowski, L., Rzepka, M., & Wang, R. (2022). Bank financial innovation and SMEs lending: do we experience a transformation in a bank-SME relationship?.

Irwin, D., & Scott, J. M. (2010). Barriers faced by SMEs in raising bank finance. International journal of entrepreneurial behavior & research, 16(3), 245-259.

Joshi, G., Kohli, B., & Nalawade, S. (2021). Are small finance banks acting as catalysts for financial inclusion in India? A phenomenological study. Qualitative Research in Financial Markets, 13(5), 655-671.

Kangayan, S., & Dhevan, K. (2020). A Study on Review of Sustainability of Small Finance Banks in India. UNNAYAN: International Bulletin of Management and Economics, 12(2), 125-140.

Khanchel, H. (2019). The Impact of Digital Transformation on Banking. Journal of Business Administration Research, 8(2), 20.

Kiganda, E. O. (2014). Effect of macroeconomic factors on commercial banks profitability in Kenya: Case of equity bank limited. Journal of Economics and Sustainable development, 5(2), 46-56.

Kumar, Rashmi (2023). India’s small finance banks use tech to tackle inclusion. Asia Money, https://www.asiamoney.com/article/2bsn62ljttth8or7kim0w/south-asia/indias-small-finance-banks-use-tech-to-tackle-inclusion.

Lodha, Vaibhav (2023). How lending-first approach can redefine SME financing. The Economic Times, https://economictimes.indiatimes.com/small-biz/sme-sector/how-lending-first-approach-can-redefine-sme-financing/articleshow/100783368.cms?from=mdr.

Lu, L. (2018). Promoting SME finance in the context of the fintech revolution: A case study of the UK’s practice and regulation. Banking and Finance Law Review, 317-343.

Lund, M., & Wright, J. (1999). The financing of small firms in the United Kingdom. Bank of England Quarterly Bulletin, 39(2), 195-201.

Mărăcine, V., Voican, O., & Scarlat, E. (2020, July). The digital transformation and disruption in business models of the banks under the impact of FinTech and BigTech. In Proceedings of the International Conference on Business Excellence (Vol. 14, No. 1, pp. 294-305).

Meyer, L. H. (1998). The present and future roles of banks in small business finance. Journal of Banking & Finance, 22(6-8), 1109-1116.

Miles, Rebecca (2023). How the rise of digital platforms is meeting unmet needs for SME banking. Intelligent SME Tech, https://www.intelligentsme.tech/2023/07/18/how-the-rise-of-digital-platforms-is-meeting-unmet-needs-for-sme-banking/.

Mohanty, J. J. (2018). Leveraging Small Finance Bank (SFB) In Achieving Financial Inclusion in India. International Journal of Business and Management. Invention (IJBMI) ISSN (Online): 2319–8028, ISSN (Print): 2319, 801.

Mujeri, M. K. (2020). Digital Transformation of MFIs: A Post Covid-19 Agenda for Bangladesh (No. 63). InM Working Paper.

Omarini, A. (2017). The digital transformation in banking and the role of FinTechs in the new financial intermediation scenario.

Panchal, Salil (2023). The Slice-NE SFB merger shakes up banking landscape. Forbes India, https://www.forbesindia.com/article/take-one-big-story-of-the-day/the-slicene-sfb-merger-shakes-up-banking-landscape/88819/1.

Pytkowska, J. (2020). Microfinance in Europe: Survey Report. European Union, 1.

Pytkowska, J., & Korynski, P. (2017). Digitalizing microfinance in Europe. Microfinance Centre, 1-12.

Raj, B., & Upadhyay, V. (2020). Role of FinTech in Accelerating Financial Inclusion in India. In 3rd International Conference on Economics and Finance organised by the Nepal Rastra Bank at Kathmandu, Nepal during February (pp. 28-29).

Rao, P., Kumar, S., Chavan, M., & Lim, W. M. (2023). A systematic literature review on SME financing: Trends and future directions. Journal of Small Business Management, 61(3), 1247-1277.

Ravikumar, T. (2019). Small Finance banks and financial inclusion in India. Small.

Reuters Report (2023). India’s Jana Small Finance Bank resubmits documents for $70 million IPO. Reuters, https://www.reuters.com/business/finance/indias-jana-small-finance-bank-resubmits-documents-70-mln-ipo-2023-07-31/.

Schweitzer, M., & Barkley, B. (2017). Is’ Fintech’Good for Small Business Borrowers? Impacts on Firm Growth and Customer Satisfaction.

Sharma, Aprajita (2023). Small Finance Banks Back In The Game. Fortune India, https://www.fortuneindia.com/long-reads/small-finance-banks-back-in-the-game/113291.

Singh, C., & Wasdani, P. (2016). Finance for micro, small, and medium-sized enterprises in India: Sources and challenges.

Siwale, J., & Godfroid, C. (2022). Digitising microfinance: on the route to losing the traditional ‘human face’of microfinance institutions. Oxford Development Studies, 50(2), 177-191.

Smith, Oliver (2023). Tide claims 10% market share of UK SMEs. Alt FI, https://www.altfi.com/article/tide-claims-10-market-share-of-uk-smes.

Srinivas, V., & Mahal, R. (2017). Digital transformation: the next big leap in microfinance. PARIDNYA-The MIBM Research Journal, 47-56.

Srivastava, Samar and Panchal, Salil (2023). Out of the woods: How Small Finance Bank staged a smart recovery. Forbes India, https://www.forbesindia.com/article/take-one-big-story-of-the-day/out-of-the-woods-how-small-finance-bank-staged-a-smart-recovery/85153/1.

Temelkov, Z., & Gogova Samonikov, M. (2018). The need for fintech companies as non-bank financing alternatives for sme in developing economies. International Journal of Information, Business and Management, 10(3), 25-33.

Viritha, B., & Mariappan, V. (2016). Anti-money laundering practices in banks: customer’s awareness and acceptance in India. Journal of Money Laundering Control, 19(3), 278-290.

Wagenvoort, R. (2003). SME finance in Europe: introduction and overview. EIB Papers, 8(2), 11-20.

Zreik, M., Marzuki, S. Z., & Iqbal, B. A. (2023). Deepening Financial Inclusion through Digitization: A Case Study of Microfinance in China. ASEAN Entrepreneurship Journal, 9(2), 9-21.

Appendix

Operating Guidelines for Small Finance Banks (RBI, 2016)

Source – RBI (Reserve Bank of India)