Executive Summary

- Digital lending has emerged as a response to the demand for convenient financial services driven by technological advancements. It has evolved differently across regions, with the US and Europe embracing online lending platforms, while Africa and Asia have seen growth through mobile money platforms and digital banking.

- Key drivers include filling the credit gap, online platforms, data analytics, smartphone adoption, and regulatory support.

- Digital lending has revolutionized the loan origination process, improved access to credit, fostered financial inclusion, and stimulated innovation. It has also played a role in boosting economic growth and supporting small-scale enterprises. Future success depends on technology, regulations, and customer needs.

Digital Lending in the UK

- The UK digital lending market is thriving, projected to reach USD 4.0 billion by 2027. It encompasses peer-to-peer lending, crowdfunding, and invoice financing. Established banks like HSBC, as well as fintech lenders such as OakNorth, offer digital solutions.

- The sector faces challenges related to data privacy, cybersecurity, and borrower default. Regulatory bodies like the Financial Conduct Authority ensure fair practices.

- With high internet and mobile penetration, the landscape fosters growth. Digital lenders must prioritize innovation, customer experience, and pricing to stay competitive.

- Regulations by the Financial Conduct Authority, Consumer Credit Act, GDPR, and AML requirements safeguard consumers and data.

Digital Lending in India

- Digital lending in India has witnessed significant growth due to various factors. The ease of obtaining loans through digital platforms has contributed to the flourishing digital lending ecosystem in the country.

- The Reserve Bank of India (RBI) has played a crucial role in legitimizing and regulating digital lenders. The market for digital lending in India is substantial, driven by a large market, increasing demand for credit, and a favourable regulatory environment.

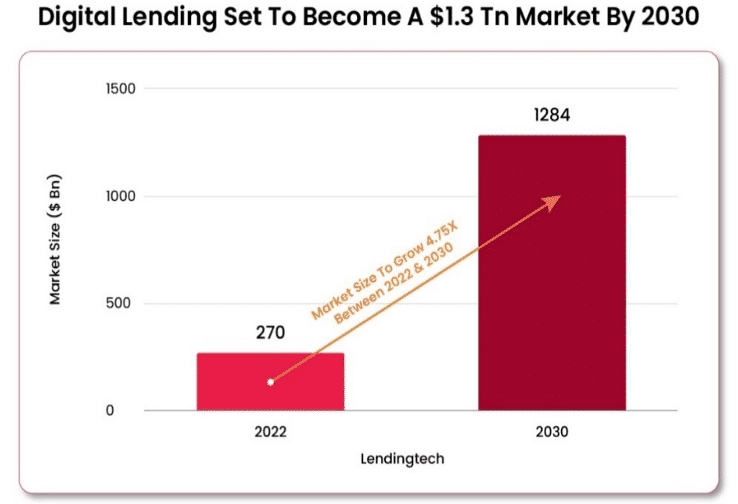

- The sector has attracted significant funding from domestic and international investors, with digital lending startups securing a significant portion of fintech funding. The market outlook for digital lending in India is optimistic, with projections estimating it to become a USD 1.3 trillion opportunity by 2030.

Table of Contents

| S. No. | Topic | Page no. |

| 1 | Introduction | 4-5 |

| 2 | Understanding Digital Lending | 5-13 |

| 2.1 | Global Evolution | 5-8 |

| 2.2 | Growth Drivers | 8-11 |

| 2.3 | Lending Process and Impact | 11-13 |

| 3 | Digital Lending in the UK | 13-21 |

| 3.1 | Sector Overview | 13-14 |

| 3.2 | Changing Digital Lending Landscape | 14-15 |

| 3.3 | Performance by British Fintech Lenders | 15-18 |

| 3.4 | Digital Lending by Banks – Performance and Challenges | 18-20 |

| 3.5 | Regulation and Regulatory Bodies | 20-21 |

| 4 | Digital Lending in India | 21-27 |

| 4.1 | Sector Overview | 21 |

| 4.2 | Digital Lending Funding Trends | 21-23 |

| 4.3 | Changing Digital Lending Landscape | 23-25 |

| 4.4 | Regulation and Role of RBI | 26 |

| 4.5 | Regulatory Impact on Borrowing | 27 |

| 5 | Future of Digital Lending | 27-31 |

| 5.1 | Recent Fintech Sector Volatility | 27-29 |

| 5.3 | The Way Forward | 29-30 |

| 6 | Conclusion | 30-31 |

| 7 | Bibliography | 32-37 |

| 8 | Appendix | 38-40 |

Introduction

As the world of finance is increasingly embracing a digital revolution, one encompassing improvements across all fields of digital financing, an important consideration is to be given to the field of financial lending. Lending, which involves the provision of funds to borrowers based on their creditworthiness, is an integral part of the financial ecosystem. Traditionally, the lending process involved borrowers submitting loan applications, lenders assessing their eligibility based on various factors, and funds being disbursed to borrowers upon approval. Borrowers would repay the loan and the accrued interest over an agreed-upon period until the entire amount was fully repaid. Digital lending refers to the practice of using technology, such as online platforms, mobile apps, and algorithms, to streamline and automate the lending process. Digital lending has become increasingly popular in recent years as it allows borrowers to apply for loans and access funds quickly and easily without having to visit a physical bank or lender (Ravikumar, 2019). Digital lending platforms typically use data analysis and algorithms to evaluate borrowers’ creditworthiness, assess risk, and determine the terms of the loan. This allows lenders to make faster lending decisions and offer loans to a wider range of borrowers who may not have access to traditional banking services.

Digital lending is rapidly emerging in India due to the growing popularity of online banking and the increasing number of people who have access to smartphones and the internet. The Indian government has also been pushing for financial inclusion and digitalization of the economy, which has created a favorable environment for the growth of digital lending in the country (Prabhakar and Webber, 2020). Digital lending has evolved rapidly in the UK in recent years, driven by the growth of online banking, the availability of alternative financing options, and the increasing use of technology in financial services. Digital lending in the UK has created a more convenient and accessible way for borrowers to access credit, as well as providing investors with new opportunities to lend money and generate returns (Langley et. al., 2019).

Digital lending platforms may offer a variety of loan types, including personal loans, business loans, student loans, and mortgage loans. Borrowers can often apply for loans online and receive a decision within minutes, and if approved, receive funds directly to their bank account. However, it’s important to note that digital lending can also carry risks, such as higher interest rates and fees, and potential for data breaches or fraud. As with any financial decision, it’s important to carefully consider the terms and risks before borrowing through a digital platform.

Expanding digital lending into new markets is another significant trend on the horizon. As technology continues to advance and internet penetration grows globally, digital lending platforms have the potential to reach underserved markets, including those with limited access to traditional banking services. This expansion can contribute to greater financial inclusion by providing individuals and businesses with previously unavailable credit opportunities.

The future of digital lending holds great promise, fueled by technological advancements and evolving consumer behaviors. Several key trends will likely shape the trajectory of digital lending in the coming years, further revolutionizing the industry. Artificial Intelligence (AI) and Machine Learning (ML) are poised to play a pivotal role in the future of digital lending. These technologies enable lenders to harness vast amounts of data and employ advanced algorithms for credit assessment, risk analysis, and decision-making processes. AI and ML algorithms can analyze various data points, including alternative data sources, to assess borrowers’ creditworthiness more accurately and efficiently. However, data privacy and security will be paramount concerns for the future of digital lending. As the volume of digital transactions and data grows, protecting borrowers’ sensitive information becomes increasingly important. Stricter regulations and enhanced security measures will be necessary to safeguard consumer data and build trust in digital lending platforms.

Digital Lending: Global Evolution

Digital lending emerged as a response to the growing demand for convenient and accessible financial services facilitated by advancements in technology. With a rise in technological advancements, including the rise of the internet, mobile devices, and digital platforms, new opportunities are subsequently created for delivering financial services in a more efficient and user-friendly manner (Aye, 2020). These advancements laid the foundation for the emergence of digital lending. These technological advancements are well documented in UK-India Fintrade’s first policy paper which covers the rise of digital institutions and neo-banks across developed and developing countries (Arun et. al., 2023).

The pattern of global evolution in digital lending, arguably, follows a similar trajectory to that of technological infrastructure. Digital lending has evolved differently in various regions, including the United States, Europe, Africa, and Asia. This variance can be attributed to the degrees of capital accumulation, technological infrastructure, education, and digital literacy in these regions (Cornelli et. al., 2021).

In the United States, digital lending has experienced significant growth and innovation. This growth, illustrated in Figure 1, began with the emergence of online marketplace lenders, also known as peer-to-peer lenders, which disrupted traditional lending models (Correa, 2023). These platforms directly connect borrowers with individual or institutional investors, offering faster loan processing and more flexible lending criteria. Over time, traditional financial institutions also entered the digital lending space, either by partnering with fintech platforms or developing their own online lending solutions. The digital lending landscape in the U.S. now includes a wide range of players, from traditional banks to alternative lenders, utilizing advanced technology, data analytics, and automation (Dixit, 2019).

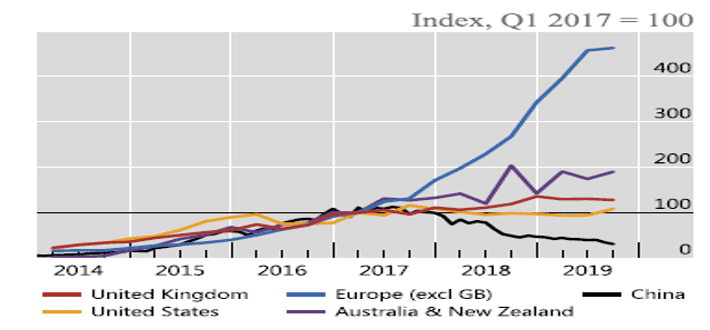

Digital lending in Europe has experienced significant growth as numerous countries have embraced online lending platforms. Peer-to-peer lending has gained popularity, providing individuals and businesses with alternative funding sources. Additionally, Europe has witnessed the rise of digital banks and neo-banks that offer online lending services in conjunction with other banking products. This trend reflects the increasing demand for convenient and accessible financial services in the region. Additionally, regulatory frameworks such as the European Union’s Payment Services Directive 2 (PSD2) have facilitated open banking and encouraged innovation in lending (Gupta, 2019). Figure 2 illustrates the growth of fintech credit across developed economies, highlighting marginal gains for US and UK in comparison to massive growth in continental Europe.

In contrast to the developed world, factors of growth in technological infrastructure are arguably not so enhanced in developing economies. However, recently there are promising signs in Africa and Asia. In Africa, digital lending has emerged as a powerful tool to promote financial inclusion, especially in regions with limited access to traditional banking services. Mobile money platforms, such as M-Pesa in Kenya (Johnen, 2023), have played a significant role in enabling digital lending by leveraging mobile technology and agent networks. These platforms allow users to access loans, make repayments, and conduct financial transactions through their mobile devices. The rapid growth of mobile phone penetration and mobile money adoption has facilitated the expansion of digital lending services across the continent (Muli, 2020; Chen et. al., 2023).

Asia, likewise, has witnessed a remarkable evolution of digital lending, driven by the region’s large population, increasing smartphone penetration, and growing digital infrastructure. In countries like China, digital lending platforms such as Alipay and WeChat Pay have transformed the financial landscape, providing access to credit, loans, and other financial services to millions of users (Klein, 2020). In India, digital lending has gained momentum with the emergence of digital lending platforms, leveraging alternative data sources and advanced technology for credit assessment (Experian, 2023). Governments and regulators in Asia are also taking steps to promote responsible lending practices and protect consumers in the digital lending space (Pazarbasioglu et. al., 2020). A study by Karaman et. al. (2021) examines the loan performance of fintech borrowers compared to bank borrowers in Turkey. Analysing data from 5.5 million consumer loans provided by the fifth-largest private commercial bank in Turkey and its fintech subsidiary, the study finds that fintech borrowers tend to be younger, more educated, have higher income and savings, pay lower interest rates, and possess better credit histories than traditional bank borrowers. Moreover, fintech borrowers are less likely to default on their loans.

Similarly, Hendriyani and Raharja (2019) explores the role of financial technology (Fintech) startups in peer-to-peer lending, bridging the gap between traditional banking and individuals who struggle to access capital from banks. Technological advancements have made financial facilitation more convenient, faster, and cost-efficient. In Indonesia, which is the focus of the paper, fintech has a significant opportunity, supported by government regulations such as Authority of Financial Services Number 77/POJK.01/2016 (Hendarta et. al., 2020). The findings generally indicate that companies have implemented strategies to attract customers in the digital finance era.

Overall, digital lending has evolved differently in each region, influenced by local market conditions, technological advancements, regulatory environments, and the specific needs of consumers and businesses in those areas. In order to understand and forecast the future outlook of the sector, it is hence essential to reflect on growth drivers which have escalated the potential for digital lending business and platforms.

Digital Lending: Growth Drivers

A significant factor which facilitated the rise in digital lending was in filling the credit gap. As traditional lending institutions often had lengthy application processes, strict eligibility criteria, and limited reach, they left a significant portion of the population underserved or excluded from accessing credit. Digital lending aimed to bridge this credit gap by leveraging technology to streamline processes and reach a wider customer base (Chakrabarty, 2022). Other factors also played an important role in boosting the evolution of digital lending, such as the creation of online lending platforms.

These platforms leveraged technology to automate loan application, underwriting, and disbursement processes (Basha et. al., 2021). Platforms incorporated data analytics, algorithms, and alternative credit assessment methods to make lending decisions quickly and efficiently. The widespread adoption of smartphones further accelerated the growth of digital lending by allowing borrowers to access loans on-the-go, while lenders could efficiently manage loan portfolios and engage with customers through mobile channels (Morgan, 2017).

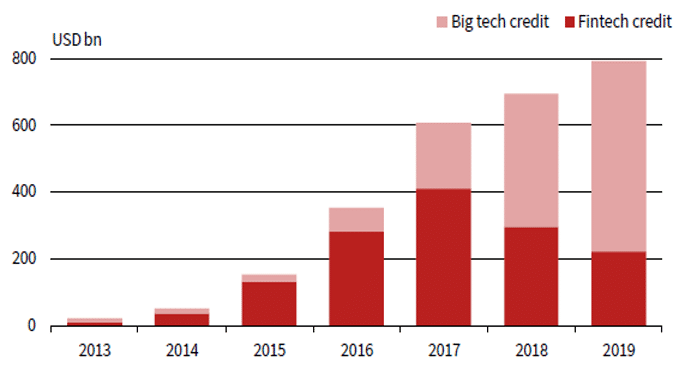

The use of data to structure digital lending solutions is observable in Figure 3 via an illustration of the growth of the lending portfolio by Big Tech corporations (Amazon, Meta) which handle vast amounts of customer data. Governments and regulatory bodies further fuelled the growth in digital lending by recognizing its’ significance and formed regulations to ensure consumer protection, fair practices, and risk management. Regulatory frameworks were established to promote responsible lending, data privacy, and transparency in digital lending operations (Mckinsey and Company, 2019).

When assessing the presence of fintech and big tech companies in credit markets worldwide, Cornelli et. al. (2023) analyses data from 79 countries between 2013 and 2018 with the study finding digital lending platforms to be more prevalent in countries with higher GDP per capita, greater banking sector mark-ups, and less stringent banking regulations. Additionally, they are more developed in countries with favourable business environments, advanced investor protection disclosure, efficient judicial systems, and well-established bond and equity markets. The findings suggest that fintech and big tech credit complement existing forms of credit rather than replacing them. As argued by Morgan (2017), digital lending, a key aspect of the fintech industry, utilizes technology to automate loan origination processes and make underwriting 3decisions based on the vast amount of data available from online activities. This eliminates the need for customers to visit physical branches and enables streamlined loan approvals. Some of the early enablers of digital lending include peer-to-peer lending and alternative credit assessments. Peer-to-peer lending (P2P) platforms revolutionised lending by connecting borrowers directly with individual lenders online. P2P lending platforms facilitated loan transactions, allowing borrowers to access funds and lenders to earn interest on their investments (Kagan, 2023). This streamlined process allowed borrowers quick access to funds and competitive interest rates while lenders could earn interest on their investments. P2P platforms facilitated the entire loan transaction, including credit assessment, bypassing traditional intermediaries. Similarly, digital lending embraced alternative data sources such as transaction history, social media profiles, and digital footprints to assess the creditworthiness of individuals or businesses. This enabled lenders to serve individuals with limited credit history or excluded by traditional credit scoring models.

While innovative, P2P lending is not without its drawbacks and limitations, as exhibited in the case of the crisis and near collapse of this market in 2016 in China. Huang and Pontell (2023) specifically focuses on the recent peer-to-peer (P2P) online lending crash in China and examines it through the lens of white-collar crime theory and financial Ponzi schemes that are encouraged with lax regulation where scheme sponsors steal from lenders of funds. The Chinese P2P e-lending boom started in 2007 and burgeoned to over 3,464 firms by 2015 when major fraud and subsequent crack down on perpetrators by the Chinese state led to a large number of these firms going out of business leaving only 343 firms with massive recorded losses to creditors by 2019. A major example of malpractice took place in 2016, marked by the Ezubao Ponzi scandal, in which USD 7.3 Bn was stolen from 900,000 investors by individuals controlling the firm (Xinhua, 2017). The number of P2P platforms ultimately had fallen to zero by November 2020, as per the China Banking and Insurance Regulatory Commission (CBIRC) (Gu et. al., 2022). The paper emphasizes the importance of adopting a proactive approach to combat financial crime rather than relying solely on reactive measures. It recommends implementing comprehensive and transparent financial regulation and law enforcement as part of a proactive system of compliance. This approach is believed to be more effective in preventing and addressing white-collar crime in the online lending industry.

This sharp rise and subsequent fall of P2P lending in China has also been well documented in Gong et. al. (2020) which offers implications for digital lending platforms to strive to reduce default risk. Huang (2018) similarly documents China’s online peer-to-peer (P2P) lending market which experienced rapid growth, becoming the largest in the world due to factors such as widespread internet access, ample funds, and unmet financial needs. However, numerous challenges forced government intervention via restrictions on business models, registration requirements, information disclosure rules, and lending limits. This experience offers potential for improvement in the industry for future sustainability.

One can also argue for the presence of external factors such as Covid-19 and the resulting rise in online presence which fuelled digital lending facilities, as argued by Alber and Dabour

(2020). This observation is in contrast to Cornelli et. al. (2021) which cautioned against the impact of Covid-19 pandemic on emerging credit models. The authors, however, cite other factors in contributing to digital lending, such as higher GDP per capita (though at a declining rate), higher banking sector mark-ups, and less stringent banking regulations. As per the paper, fintech credit reached USD 223 billion, while big tech credit reached USD 572 billion in 2019. Understanding the various growth drivers and factors which boost digital lending is essential to analyse its’ future scope and application across both UK and India. At the same time, it is important to understand the impact that the sector has had on boosting economic growth.

Lending Process and Impact

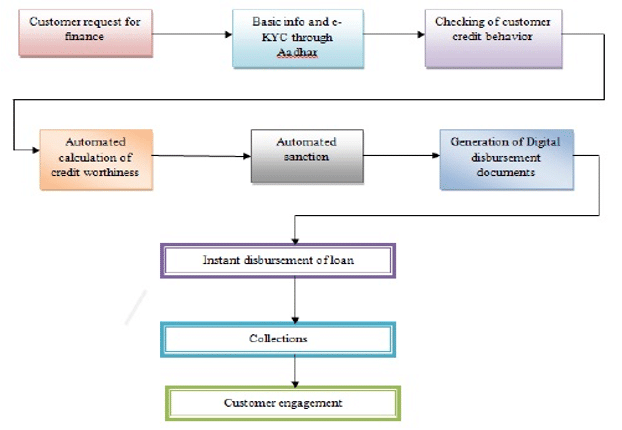

Digital lending builds upon the foundation of the paper-based lending process used by banks and financial institutions before the advent of digital technology. In this modern approach, borrowers apply for loans through online platforms. Lenders employ advanced technology and data analytics to assess the borrower’s creditworthiness. Once approved, loan terms are finalized electronically, and funds are disbursed digitally. Borrowers make repayments online, making the entire process more efficient, convenient, and streamlined than traditional lending methods. This step-by-step process is showcased in Figure 4.

Digital lending has arguably had a significant impact on the lending landscape. It has revolutionized the loan origination process by leveraging technology to provide faster and more efficient services. It has simultaneously improved access to credit for individuals and businesses, especially those underserved by traditional financial institutions. Additionally, digital lending has fostered financial inclusion, empowered borrowers with more control and convenience, and stimulated innovation in the financial sector (Rubini, 2018).

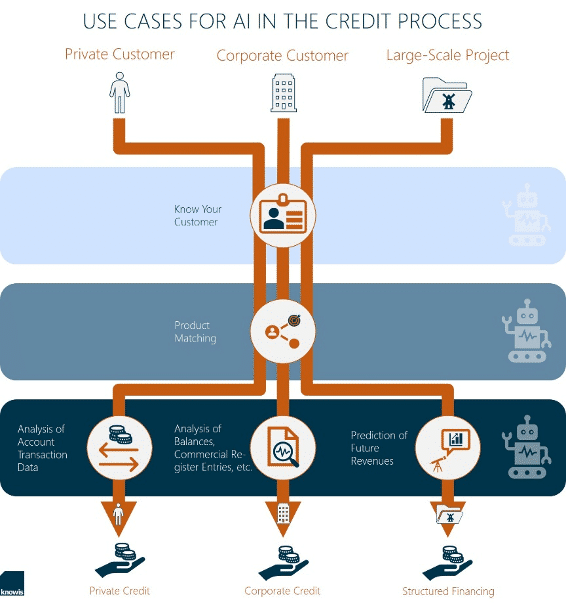

As previously discussed, incorporating AI and ML further enhances the streamlined digital lending process. AI and ML expedite and streamline the end-to-end mechanism and efficiently handle lending requests from diverse stakeholders, including private customers, corporate customers, and large-scale projects. These optimized process flows, illustrated in Figure 5, enable lending platforms to cater effectively to stakeholders, fostering their growth, profitability, and business potential. Stewart et al. (2018) state that digital lending can promote financial inclusion by offering faster, more affordable, and engaging financial services to underserved clients. Governments are actively promoting digital lending models to extend high-quality financial services to marginalized communities, and financial service providers (FSPs) can leverage digital lending to gain competitive advantages and meet evolving customer expectations. Damodaran et al. (2019) highlight the case of India’s rapidly growing economy and government-led digitization efforts that have transformed commerce and attracted investments. However, ensuring that unorganised and small-scale enterprises are included in the digital transformation is important. Digital lending platforms have emerged as a solution, particularly for Micro, Small, and Medium Enterprises (MSMEs), providing funding and support to address their unique challenges and streamline procedures. Stulz (2019) highlights an intriguing aspect of digital lending evolution in large banks. Contrary to Bill Gates’ statement in 1994 about banks facing extinction in the internet age, the author argues that banks have increased in size and value since then. Banks have capitalized on technological advancements, brand names, and reputations to invest in and expand their digital lending portfolios.

These studies underscore the potential of digital lending to drive financial inclusion, support economic growth, and transform the banking industry, demonstrating the various benefits and opportunities associated with the digital lending landscape.

Digital Lending in the UK

Sector Overview

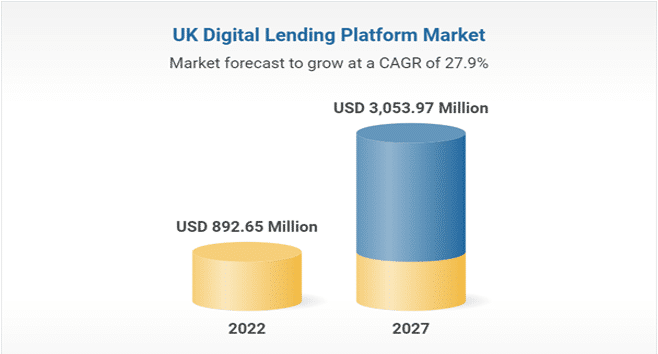

The origins of digital lending in the UK can be traced back to the introduction of Zopa, a peer-to-peer lending platform offering personal loans in 2005 (Neuwirth, 2022). Over time, the U.K. peer-to-peer lending market has evolved into a marketplace model, expanding its focus to include lending platforms catering to small and medium-sized enterprises (SMEs) and property lending. The government has been supportive of the sector, implementing a dedicated regulatory framework since 2014 (FCA, 2019).The UK’s Digital Lending Platform Market was valued at approximately USD 892.65 million in 2022, with expectations to reach USD 3,053.97 million by 2027, exhibiting a compound annual growth rate (CAGR) of 27.89% (Business Wire, 2022). The UK’s lending fintech ecosystem is vibrant, hosting disruptive companies that leverage the latest technologies to streamline the traditionally outdated and non-transparent lending process. This technological integration has empowered lenders to enhance payment processing speed and provide personalized experiences tailored to the needs of loan and mortgage seekers.

The UK digital lending market has seen significant growth in recent years, with several players and new entrants offering a range of products. According to a report by the Cambridge Centre for Alternative Finance (2021), the UK’s online alternative finance market grew by 35% in 2020, despite challenges posed by the Covid-19 pandemic. Peer-to-peer lending, crowdfunding, and invoice financing are among the most popular types of digital lending products in the UK. Figure 6 illustrates the substantial growth forecast for digital lending in the UK till 2027, highlighting a growth to an estimated USD 4.0 Billion portfolio.

In addition, the UK government has introduced several initiatives to support the growth of digital lending, such as the British Business Bank’s ENABLE Funding program, which provides funding to alternative lenders that lend to small and medium-sized businesses (Butler, 2023). However, as with any emerging market, digital lending in the UK also faces challenges, such as concerns around data privacy and cybersecurity, as well as the risk of default by borrowers. The Financial Conduct Authority (FCA) has introduced regulations to ensure digital lending platforms operate in a fair and transparent manner and borrowers are protected.

Changing Digital Lending Landscape

The widespread availability of high-speed internet and the rapid adoption of smartphones have contributed to the growth of the digital landscape in the UK. Today, a large portion of the population has access to online services and uses mobile devices for various activities. This has coincided in a similar rise in e-commerce and online retail services (Turner, 2017). A report titled ‘Digital 2023 – The United Kingdom’ highlights digital adoption among the British population, with 87.66 million cellular mobile connections, 66.11 million internet users and 57.10 million active social media users: all three indicators registering growth (Digital 2023 – the UK, 2023). The adoption of digital payment methods, such as mobile wallets, contactless cards, and online payment platforms, has become widespread. This shift has made transactions more convenient and accelerated the move towards a cashless society. Similarly, there is increased scope for fintech and digital banking services. The UK has become a global hub for financial technology ‘fintech’ innovation, as highlighted in the Kalifa Review of UK Fintech (Kalifa Review, 2021).

Digital banking services have gained popularity, providing customers with access to banking services through mobile apps and online platforms (Dietz et. al., 2023).

It can be argued that the digital evolution is not only restricted to financial services or online retail services but also transcends to other industries. Digital entertainment and streaming services such as Netflix, Amazon Prime and Channel 4, and social media forums such as Instagram, Facebook, Tiktok and Snapchat are prime examples of an ever-expanding digital evolution. Government adoption of digital services via applications such as HMRC app, Gov.UK ID check app and Immigration app also constitutes a focus on digitizing public services, making them accessible online. This includes services related to healthcare, education, and more (UK Digital Strategy, 2022).

The digital lending landscape in the UK is experiencing rapid growth, fuelled by changing consumer behaviour, technological advancements, and regulatory initiatives. Similar to India, the UK is witnessing a significant expansion of the digital lending market, with more consumers embracing digital platforms for accessing credit. According to Deloitte, the UK alternative lending market was valued at £7.3 billion in 2020 and is projected to reach £17 billion by 2025 (Deloitte, 2021). Digital lenders are also exploring innovative lending models like marketplace lending, which connects borrowers with a network of individual and institutional lenders. Other models, such as invoice financing, supply chain financing, and factoring, are also gaining traction (Bank of England, 2021-2023).

Furthermore, sustainability is a growing focus in the digital lending industry. Lenders are increasingly offering green loans and financing options for sustainable projects. Initiatives like the UK’s Green Finance Initiative aim to promote the growth of green finance and support the transition to a low-carbon economy. However, ensuring effective supervision and regulation of these sustainability initiatives may present challenges (Retail Banker International, 2022).

Performance by British Fintech Lenders

In 2020, IBS Intelligence published a list of five fintech lenders and their notable innovations in the digital lending market (Bhattacharya, 2020). These innovations propelled them to establish a significant market presence in the UK, further fuelled by the increased adoption of digital transactions during the Covid-19 pandemic. However, since the lending boom of 2020, each of these five parties has encountered unique outcomes. A detailed analysis of each party’s performance is provided below.

OakNorth

OakNorth Bank is a British financial institution specializing in lending services for small and medium-sized businesses as well as property loans. Recently, the company received approval from the British Business Bank for an additional allocation under the Coronavirus Business Interruption Loan Scheme (CBILS). Since the Covid-19 induced lockdown began on March 23, the bank has approved more than £600 million in loans to support UK businesses.

Co-founded by Rishi Khosla and Joel Perlman, OakNorth Bank gained regulatory approval in 2015. In 2019, the bank reported a pre-tax profit of £65.9 million. OakNorth Bank focuses on providing flexible and accessible debt financing ranging from £500,000 to £50 million. With teams operating in various locations including London, Manchester, Bristol, Birmingham, Leeds, and East Anglia, the fintech lender has achieved regional diversity (Khairnar, 2022).

Iwoca

Iwoca is a London-based fintech company that operates an online lending platform, offering credit facilities to small businesses in the UK and Germany. The company recently secured funding through the government’s Future Fund scheme. Iwoca plans to collaborate with UK banks to enhance access to finance for small and medium-sized businesses (SMBs) through the Coronavirus Business Interruption Loan Scheme (CBILS).

Iwoca aims to work with banks to expedite the application process for businesses that have been waiting for more than two weeks for feedback. Founded in 2011 by Christoph Rieche and James Dear, Iwoca utilizes digital solutions, including its website, lending API, and Open Banking, to simplify and accelerate loan approval, offering loans of up to £250,000 to small and micro businesses (Fintech Finance, 2023; Kuziemko, 2021).

B-North

B-North, a UK-based SME lending bank, aimed to provide excellent borrowing experiences for small and medium-sized businesses. Additionally, the bank planned to offer competitive savings products to retail consumers and business customers in the UK. In order to enhance customer onboarding, compliance capabilities, and expedite business lending, B-North had partnered with the RegTech platform TruNarrative. This collaboration built upon B-North’s previous partnerships with Mambu for core banking solutions and nCino for loan origination workflow. The integration of these technology solutions aimed to streamline operations, improve customer experience, and ensure regulatory

compliance However, on account of failing to secure a Series B license, the bank had to seize operations, with LHV UK having purchased its SME lending portfolio (Finextra, 2022).

Funding Circle

Funding Circle is a peer-to-peer lending marketplace provider that allows the public to lend money directly to small and medium-sized businesses. The UK-based small business loan platform recently teamed up with Starling Bank to offer £300 million of loans to SMBs under the Coronavirus Business Interruption Loan Scheme (CBILS).

In April, Funding Circle became the first P2P lending platform to be accredited to deliver CBILS. The platform paused all non-CBILS lending from retail and institutional investors to focus on supporting the scheme. It was approved to deliver emergency funding to businesses impacted by Covid-19. The lender continues to build on this growth, with former executive having recently raised GBP 7 Mn for SME lending startup Triver (Kleinman, 2023).

Funding Xchange

Funding Xchange is an SME lending marketplace and intelligent decisioning platform that serves over 10,000 customers a month. Founded in 2014, Funding Xchange aims to bring transparency and efficiency to small business lending. It refers small businesses declined credit by their bank to other sources of funding. It recently announced the appointment of various advisors to its board in the light of its upcoming launch of Credit-as-a-Service proposition for banks and lenders. Funding Xchange and Experian announced the launch of an online service for banks in a bid to enable businesses affected by the pandemic.

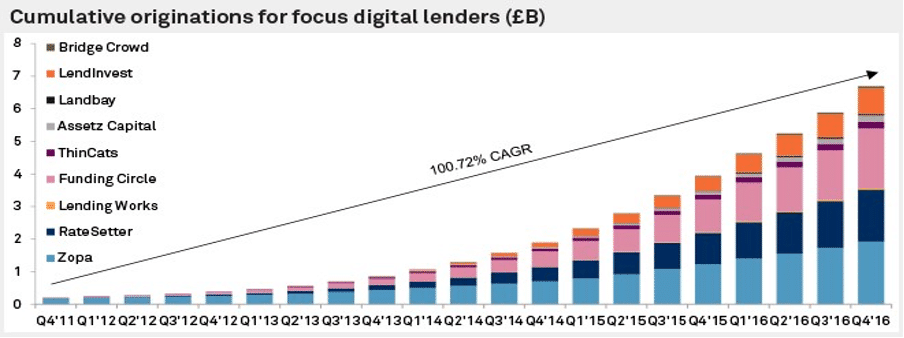

Most of these lenders continues to record business growth, however there are concerns cited of borrower distress in the UK owing to the cost-of-living crisis and inflation, due to which these lenders can suffer (Gaw, 2022). Not all stories are positive either, as is reflected in the case of B-North. Figure 7 showcases annual growth in the digital lending business by most platforms in the UK, indicating a positive, upward trend.

| Lender Name | Founding Year | Nature of Operations |

| Assetz Capital | 2012 | Property-secured loans to businesses |

| B-North | 2018 | UK-based SME lending bank, now defunct |

| Bridge Crowd | 2012 | Peer-to-peer bridging loans secured over UK property |

| Funding Circle | 2010 | Lending marketplace allowing public to lend money |

| Funding Xchange | 2014 | SME lending marketplace, intelligent decisioning platform |

| Iwoca | 2011 | Independent company custom-built for small businesses |

| Landbay | 2014 | UK fintech company operating mortgage lending platform |

| Lending Works | 2014 | Peer-to-peer platform connecting investors with borrowers |

| LendInvest | 2012 | Largest online property investing and lending business |

| OakNorth | 2015 | Provides loans, and business and personal savings accounts |

| ThinCats | 2010 | Business loans to mid-sized UK businesses using capital |

| RateSetter | 2010 | Personal loan provider, pioneer of peer-to-peer lending |

| Zopa | 2005 | World’s first peer-to-peer lending company, now full bank |

Digital Lending by Banks – Performance and Challenges

Digital lending has experienced significant growth within big banks in the UK as they adapt to technological advancements and changing consumer preferences. Traditional banks, including Barclays, HSBC, Lloyds Bank, NatWest, Santander, and Nationwide Building Society, have introduced digital lending platforms to offer customers convenient and streamlined loan application processes. These platforms enable customers to apply for personal loans and mortgages online, eliminating the need for physical visits and paperwork. While big banks are relatively new to the digital lending market, there is potential for expansion and further development (Green, 2019; Finextra, 2017).

In addition to established banks, digital banks, and neo-banks such as Revolut, Monzo, Starling Bank, N26, and Atom Bank also offer digital lending services. However, compared to traditional banks and dedicated lending platforms, digital banks primarily focus on personal loans, with a limited digital lending portfolio. The presence of multiple financial service providers in the digital lending space creates competition, emphasizing the importance of innovation, customer experience, and competitive pricing for attracting a larger market share to drive profitability and growth (Krauser, 2022).It is worth noting that Policy Paper 1 by Arun et al. (2023) discusses the product diversification efforts undertaken by neo-banks in the UK, indicating the potential for these digital banks to expand their lending offerings in the future.

Despite advancements in the digital lending infrastructure and a promising growth outlook, the sector faces various obstacles and challenges that pose significant threats, such as data security and privacy. As digital lenders collect and process personal and financial data, it becomes imperative to prioritize data security and protect customer information from unauthorized access and cyber threats. The risk of fraud and identity theft is also a major concern, as digital lending platforms may be vulnerable to fraudulent activities, including loan application fraud and identity theft. Implementing robust authentication and verification processes becomes essential to mitigate these risks. Moreover, a lack of customer trust poses a significant hurdle, as potential borrowers may hesitate to utilize digital lending services due to concerns about data privacy, security, or a lack of familiarity with online lending platforms (Kale, 2021).

Furthermore, digital lenders face challenges that directly impact their performance. One such challenge is the ability to conduct effective credit risk assessments. Accurately evaluating borrowers’ creditworthiness remains a persistent challenge in digital lending. Developing robust credit risk models and algorithms to assess borrowers’ creditworthiness is crucial for maintaining loan quality and minimizing default rates. Additionally, lending platforms must ensure compliance with regulations and consumer protection laws. Navigating the complex and time-consuming process of meeting the requirements set by regulatory authorities is a significant challenge (González Páramo, 2017).

Other external challenges include the threat of a competitive landscape. The digital lending space in the UK is becoming increasingly crowded, with various players offering similar services. Digital lenders must differentiate themselves through innovative offerings, competitive interest rates, and superior customer experience to stand out in the market. Economic downturns or uncertainties can also impact borrower repayment capabilities and increase default rates. Lenders need to closely monitor economic indicators and adapt their lending practices accordingly. Lastly, there is the threat of market volatility, as changes in interest rates, regulations, or market conditions can influence the profitability and viability of digital lending platforms (Sommer, 2021).

Regulation and Regulatory Bodies

Digital lending activities in the UK are subject to a regulatory framework to ensure consumer protection, responsible lending practices, and data privacy. The Financial Conduct Authority (FCA) is the regulatory body overseeing financial services, including digital lending. The FCA sets standards and requirements that digital lending platforms must adhere to, promoting fair treatment and consumer protection. The Consumer Credit Act of 1974 and subsequent amendments provide a legal framework for consumer credit activities, including regulations related to credit provision, disclosure of terms, interest rates, and consumer rights.

To safeguard data privacy, digital lending platforms in the UK must comply with the General Data Protection Regulation (GDPR) and the Data Protection Act 2018. These laws govern personal data collection, use, storage, and protection, ensuring borrowers’ information is handled securely and with consent. Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations are also in place to prevent money laundering and terrorist financing. Digital lending platforms must verify borrowers’ identities, conduct due diligence, and report suspicious activities.These regulations collectively provide greater customer protection while enabling lending facilities for trustworthy customers, mitigating the risks of adverse selection and moral hazard. As a digital lending provider, it is crucial to ensure customers’ ability to repay their loans in the future, supported by the relevant rules and regulations.

In addition, the UK government is tightening regulations on buy now, pay later (BNPL) loans to prevent borrowers from taking on unaffordable debts. Lenders will be required to conduct affordability checks and ensure fairness. The Financial Conduct Authority must approve providers, and borrowers can escalate complaints to the Financial Ombudsman Service. Similar rules will also apply to other forms of short-term interest-free credit. These regulatory measures aim to protect consumers and foster the safe growth of the innovative lending market in the UK, particularly amid inflation concerns and the need to support struggling borrowers.

Overall, these lending regulations create a secure environment for digital lending in the UK, promoting trust and encouraging lenders to offer services while providing borrowers with opportunities for personal and business financing.

Digital Lending in India: Sector Overview

Compared to the UK, the scope of digital lending in India is arguably not far behind. Compared to a cumbersome loan application process that symbolised the traditional lending mechanism, ease of getting a loan sanctioned digitally has made digital lending flourish in India. As per the Rudra (2022) interview with CEO of Indifi Technologies Alok Mittal, 2022 was a remarkable year for digital lending in India, a phenomenon attributed to multiple factors. One is Indian market’s resilience and agility due to which businesses across the board have picked up again. Advancement in technology and digital capabilities is another factor, along with trust in using digital services. These factors have combined to ensure digital lending is an accessible business decision (Rudra, 2022).

Mr. Mittal highlighted the role played by RBI in providing the regulatory framework for digital lenders play in the economy and in setting up guardrails so that growth in lending does not result in excessive defaults as experienced in China and there is more protection for loan providers. The Data Protection Bill, the Account Aggregator framework, and the RBI guidelines for Loss Sharing Arrangements in digital lending have been seen to be positive steps (Rudra, 2022, see also Appendix 1). Thus, an integral role is played by the central regulator, Reserve Bank of India (RBI), in guaranteeing effective supervision and monitoring across the fintech industry for e-lending platforms, digital banks and neo-banks (Arun et. al., 2023).

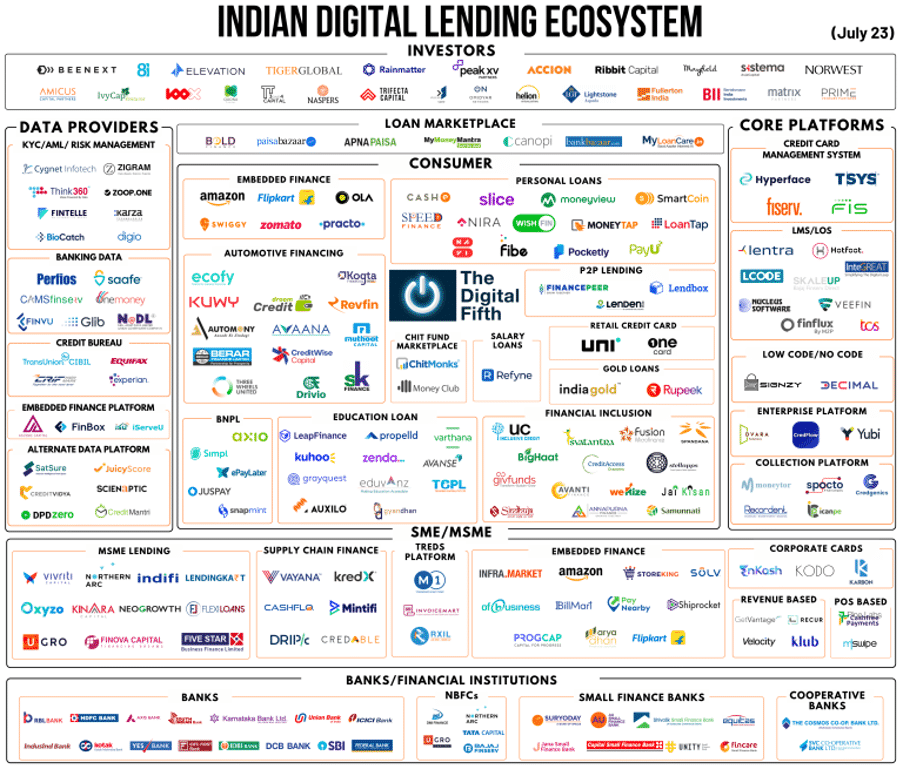

The Indian digital lending scene now has upwards of 100 companies or institutions giving out loans of about USD270 billion. Digital lending covers many segments of the economy from consumer loans (including personal loans, automotive financing, student loans, gold loans, Buy now Pay Later); SME & MSME loans and other business loans loans like invoice discounting; Financial Inclusion e-lending such as Jai Kisan, Avanti etc (The Digital Fifth 2023, see also Appendix 2).

Digital Lending Funding Trends

The funding potential for digital lending in India is significant, driven by various factors contributing to the country’s rapid credit demand and the government’s focus on financial

inclusion and digital financial services. One key factor is the presence of a vast market opportunity. With a population of over one billion people, a substantial portion of which remains underserved by traditional financial institutions, there is a largely untapped market that digital lending platforms can cater to (Chand, 2022).

The growing population also translates into an increasing demand for credit. As the Indian economy continues to expand, individuals and businesses seek access to credit. Digital lending platforms offer a convenient and efficient way to fulfil this demand by leveraging technology for quick and easy credit provision, making them an appealing choice.

Furthermore, the regulatory environment in India has played a significant role in fostering the growth of digital lending. The Reserve Bank of India (RBI) has taken proactive measures to support the digital lending sector, such as introducing peer-to-peer (P2P) lending platform guidelines and establishing a Regulatory Sandbox for fintech startups. These regulatory initiatives provide a conducive framework for digital lending platforms to operate and grow within a regulated environment, ensuring consumer protection and promoting industry innovation. This has helped to create a favourable regulatory environment (Wadhwa, 2023).

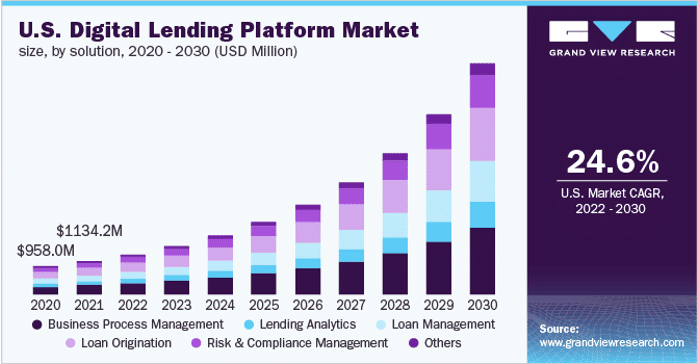

The collective impact of these factors has led digital lending platforms in India to attract significant funding from domestic and international investors. According to KPMG, the Indian fintech industry raised a substantial amount of USD 3.7 billion in funding in 2019, with a considerable portion allocated to digital lending. The funding prospects for digital lending in India remain significant, as the industry is poised for sustained growth in the coming years, as depicted in Figure 9. However, as the industry evolves, digital lending platforms must address concerns such as data privacy, cybersecurity, and regulatory compliance to ensure long-term sustainability (KPMG, 2019).

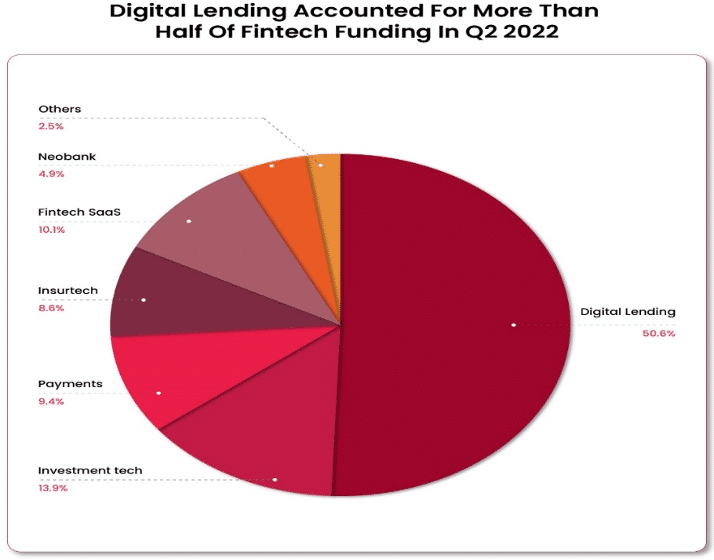

From 2014 to Q2 2022, the overall fintech ecosystem secured a total funding of USD 6.49 billion across 447 deals. During Q2 2022 (April-June), the digital lending segment witnessed the highest influx of funds, raising USD 902 million through 28 deals. It accounted for 50.6% of the total funding in the fintech sector and 33% of the funding deals during the quarter. Digital lending startups constituted half of the top 10 fintech funding deals in Q2 2022, securing USD 340 million across five deals. Remarkably, these digital lending startups raised over a third of the total funding through only 17% of the deals (Bundhun, 2023).

The data and statistics reveal significant potential for growth and sustainability in the digital lending sector in India. Coupled with favourable regulatory improvements, technological advancements and population growth in India contribute to a promising picture for digital lending, as can be inferred from the share of total fintech funding in figure 10. The total share of funding for digital lending amounted to 50.6%, roughly half of the total.

Changing Digital Lending Landscape – India

According to Inc42’s latest report ‘State of Indian fintech Ecosystem Q3 2022 InFocus: Neobanks’, digital lending in India is projected to present a significant market opportunity, reaching USD 1.3 trillion by 2030. The market size of digital lending is expected to grow at a CAGR of 22% between 2022 and 2030, expanding from USD 270 Bn in 2022. This nearly 5 times increase is driven by favourable socioeconomic factors throughout the decade (Kashyap, 2022).

Fintech lending is anticipated to outperform other major sectors, including enterprise-tech and edtech, in terms of the number of companies achieving a valuation of over USD 1.0 billion, known as ‘soonicorns’. Currently, the fintech sector boasts 33 soonicorns, with 39% operating in the digital lending segment. The digital lending sector comprises two unicorns, Yubi (formerly CredAvenue) and Oxyzo. Integrating Unified Payments Interface (UPI) with credit cards is expected to enhance the popularity and usage of credit cards in India (Boston Consulting Group, 2018).

The outlook for fintechs, both globally and in India, appears promising in 2023. Initiatives such as Ocen, open banking, and account aggregators seek to enhance credit enablement and foster a symbiotic relationship between incumbents and financial institutions. It is predicted that digital lending fintechs will continue to thrive and grow in the coming year, particularly as credit penetration increases, especially in developing economies like India. Embedded finance platforms and niche fintechs are expected to attract more funding. In the UK, digital lenders are poised for expanded growth, supported by new savings account options, ongoing regulatory and government support, and a proven ability to provide capital to small businesses despite uncertainties related to Brexit.

The digital lending landscape in India is rapidly evolving, driven by factors such as technological advancements, changing consumer behaviour, and regulatory initiatives. Some ways in which the digital lending landscape is changing in India include an increased adoption of digital lending platforms. With the rise of smartphones and internet connectivity, more and more consumers are turning to digital lending platforms.

An emphasis on alternative data for credit scoring by digital lenders has resulted in effective results. These alternative data sources, such as social media activity and mobile phone usage, aim to assess overall creditworthiness. This allows lenders to serve customers who may not have a traditional credit history. Additionally, a growing focus on customer experience allows lenders to have a competitive advantage. As competition in the digital lending space heats up, lenders are focusing more on providing a seamless and personalized customer experience. This includes instant loan approvals, flexible repayment options, and digital documentation.

A snapshot by The Digital Fifth points to the highly developed and integrated digital lending ecosystem in India. As per the illustration, consumer lending organizations are supported by core platforms and data providers. Additionally, there are SME / MSME lending organizations and banks / other FI’s which contribute as digital lending providers. A last category of the ecosystem is investing organizations providing fintech funding. Details of these stakeholders are provided in the Appendix 2.

Overall, the digital lending landscape in India is changing rapidly, creating new opportunities for lenders and borrowers alike. However, it is also creating challenges, such as data privacy and security concerns, which will need to be addressed to ensure long-term sustainability. As with any emerging market, digital lending in India also faces several challenges, such as lack of regulation, data privacy concerns, and the risk of default by borrowers. The Indian government has been working to address these issues by introducing new regulations and guidelines for digital lending platforms to ensure that they operate in a fair and transparent manner while protecting the interests of borrowers (Singh, 2021).

Fake lending applications pose a significant threat in the digital lending industry. These apps collaborate with defunct non-banking financial companies (NBFCs) to fraudulently obtain licenses for digital lending businesses. They create virtual merchant IDs with payment aggregators to facilitate money transactions. These apps target customers, offering high-interest loans and excessive processing fees. They also illegally access personal data, leading to privacy breaches. In the event of non-payment, these apps resort to public humiliation, causing severe consequences, including suicides. The proceeds of these crimes are usually transferred out of India (Ranjan, 2022)

To combat this issue, the Enforcement Directorate (ED) has conducted searches and seized funds from payment aggregators linked to these fake lending apps. The agency is also investigating crypto exchanges to trace the proceeds of crime. Recognizing the growing threat, Finance Minister Nirmala Sitharaman chaired a meeting, resulting in the Reserve Bank of India (RBI) being tasked with creating a whitelist of approved digital lending apps. The Ministry of Electronics and IT (MeitY) will ensure that only whitelisted apps are available for download, aiming to enhance consumer protection and combat fraud.

Regulation and Role of RBI

In India, digital lending platforms typically use a combination of data analytics, artificial intelligence, and machine learning algorithms to assess the creditworthiness of borrowers and make lending decisions. Digital lending platforms have become popular among small and medium businesses, and individual borrowers lacking access to traditional banking services (Mastropietro and Blini, 2022). Several digital lending startups have emerged in recent years, being classified under two main categories (RBI, 2021).

| Digital Lending Apps / Platforms (DLAs) | Lending Service Provider (LSP) |

| Mobile and web-based applications with user interface that facilitate digital lending | An agent of a Regulated Entity which carries out one or more of lender’s functions |

| DLAs will include apps of the Regulated Entities (REs) as well as those operated by Lending Service Providers (LSPs) | Operations include customer acquisition, underwriting support, pricing support, servicing, monitoring, recovery of specific loan or loan portfolio on behalf of REs |

In June 2022, the Reserve Bank of India (RBI) banned fintech companies without a banking licence from loading credit lines into their prepaid payment instruments (PPIs), sending a shockwave across the digital lending ecosystem. (Shah, 2022). The move resulted in many companies such as slice, One Card, Jupiter and Kreditbee changing their business models to comply with the new regulations. To further boost the United Payments Interface (UPI), the National Payments Corporation of India (NPCI) is working to link credit cards with the real-time payment system. The process is currently in its pilot phase, with RuPay Credit Cards being linked with UPI first. It is likely to include a 2% merchant discount rate, opening the avenues for the much-needed monetisation from UPI (Sharma, 2021).

The RBI also issued digital lending guidelines based on the recommendations of a working group to mitigate the concerns surrounding the lending ecosystem. These concerns include engagement of third parties, mis-selling, data privacy breaches, unfair business conduct, high interest rates and unethical recovery practices. An overview of RBI guidelines and initiatives are presented in Appendix 1.

Regulatory Impact on Borrowing

The new RBI guidelines introduced various changes including imposing restrictions on existing loan disbursement and repayment fund-flows, prohibiting grant of credit on e-wallets, regulating collection of fees by lending apps, mandating compulsory reporting of all digital loans to the credit bureaus, and regulating collection and usage of customer data by fintech companies among others (Ramdas and Mishra, 2023).

One useful instrument which mitigates risk for lenders is a first loss default guarantee. FLDG arrangements involve regulated lenders mitigating credit risk through fintech companies that provide customers for their loans. The RBI is concerned about the systemic risks posed by relying on unregulated fintech companies for FLDG. However, restricting FLDG arrangements without viable alternatives could hinder digital lending growth, and affect loan terms and pricing. The new guidelines discourage the use of pool accounts for loan fund-flows. Direct fund-flows between customers and lenders may make loan repayments cumbersome for retail consumers without payment aggregators’ involvement (Ramdas and Mishra, 2023).

The RBI’s restriction on granting loans into e-wallets has hindered consumers who relied on customized digital lending products tied to their prepaid wallets. These guidelines limit the role of fintech companies in providing seamless digital lending services. To ensure future growth and preserve the innovative user experience, regulatory clarifications are necessary to address these issues (Mathi, 2023).

Overall, regulatory improvements in digital lending benefit borrowers by increasing credit availability, ensuring fair practices, and protecting customer data. Clear regulations instil confidence in lenders, fostering innovation and competition. Addressing privacy and security concerns enhances cybersecurity, creating a secure lending environment. Overall, well-designed regulations promote access to credit, consumer protection, and innovation while providing a clear framework for lenders to build trust with customers.

Future of Digital Lending

Recent Fintech Sector Volatility

With a funding slowdown being experienced by other sectors, the writing is on the wall for a correction in the fintech segment as well. After a watershed year in 2021, which saw fintech startups raising $8 Bn across 280 deals, the funding momentum has slowed down. During the first three months of 2022, fintech funding fell by 44% and remained flat in Q2 2022.

The number of funding deals remained almost constant during Q4 2021 and the first two quarters of 2022, representing a fall in average ticket size in the sector. Besides the negative investor sentiment globally, a rapid change in the regulatory landscape within India’s fintech ecosystem is also behind the decline in funding (Kashyap, 2022). While digital lending has several advantages, it also faces several challenges and risks that must be addressed to ensure the long-term sustainability of the industry. Many of these challenges have been discussed in the context of both economies under consideration: UK and India. Some of the overarching key challenges and risks include cybersecurity, operational, and data privacy risks.

Digital lending platforms face various risks and challenges. Cybersecurity risks, including hacking, data breaches, and fraud, can compromise customer information and trust, leading to regulatory consequences. Compared to traditional lenders, digital lending platforms may have higher credit risk due to limited access to credit history and financial information, resulting in higher default rates and loan losses. Operational risks such as system failures, technology disruptions, and vendor risk can disrupt business operations and harm the platform’s reputation.

Moreover, privacy concerns arise as digital lending platforms collect and process sensitive customer data. Data breaches can cause reputational and financial damage, along with regulatory fines and legal actions. The evolving regulatory landscape poses compliance challenges for digital lenders, as unclear regulations make it difficult to understand and adhere to the rules. This lack of regulatory clarity creates a challenging operating environment for digital lending platforms.

In addition to the volatility experienced by the fintech sector in 2022, the commercial banking industry suffered similar hurdles in the early months of 2023. Examples of such failures include the collapse of Silicon Valley Bank (SVB) and Credit Suisse, cited in policy paper 1 as having overall positive and negative influences on the neo-banking sector. Dwindling customer confidence in big banks and digital banks can, similarly, have both positive and negative impacts on digital lending (Elsaid, 2021; HES Fintech, 2022).

Trust and perception are key factors which can determine lack of confidence in digital lending platforms. If customers have lost confidence in big banks or digital banks, they may be sceptical about engaging with any financial institution, including digital lenders. Loss of trust in digital lending platforms can stem from customers’ lack of confidence in big banks and concerns about data privacy and unethical practices. This reluctance to engage with financial institutions hinders accurate credit assessment and may lead to increased regulatory scrutiny. However, decreased confidence in established banks can drive borrowers to alternative lending options, such as customer-centric digital lenders. By addressing pain points experienced with big banks and prioritizing transparency, accountability, and data privacy, digital lenders can rebuild customer confidence and promote financial inclusion. The overall impact of banking industry volatility and customer trust on digital lending remains uncertain, but advancements in technology and digital literacy offer potential benefits for the industry.

The Way Forward

Compared to India, the global scenario 2022 could have been more favourable. The digital lending ecosystem experienced a mixed year, with positive and negative developments. However, significant changes have occurred in the industry over the past year. At the beginning of 2022, during the third wave of the global pandemic, there was a 50 per cent increase in digital adoption, particularly in India, where internet penetration played a crucial role. India made progress towards its goal of financial inclusivity with the growing prominence of UPI and IndiaStack. Despite these efforts, India still needs help in bridging the credit gap for thin-file citizens in tier-2/tier-3 cities and rural areas. This situation presents an excellent opportunity for fintech startups to tap into an underpenetrated market and capitalize on abundant growth opportunities (Karthik, 2022).

In 2022, the world witnessed the rise of significant fintech unicorns in the financial services sector. It was also the year when India’s fintech platform ‘Open’ became the country’s 100th unicorn. However, overall, fintechs experienced a decline in funding due to global macroeconomic issues. For instance, Swedish BNPL fintech ‘Klarna’ saw its valuation drop from $45 billion in 2021 to $6.5 billion in 2022. Consolidation trends, as seen in PhonePe’s acquisition of Zest and Cred’s acquisition of CreditVidya, contributed to the decline in funding within the Indian fintech landscape.

Despite the challenges mentioned, the future appears promising for digital lending. Technological advancements, data analytics, and automation are expected to drive continued growth and innovation. The focus will be on offering personalized loan options, faster approval processes, and improved customer experiences. Collaboration between traditional financial institutions and fintech companies will likely increase, leading to hybrid lending models (Williams, 2022; Krauser, 2022).

Digital lending presents significant opportunities in India and the UK, given the low penetration of formal finance and the increasing demand for credit. With its large population and expanding internet access in India, digital lending platforms are expected to leverage technological innovations such as AI and machine learning to provide credit access. Similarly, digital lending platforms in the UK will continue to expand, offering faster and more convenient credit access supported by data analytics and automation. However, regulatory challenges, data privacy concerns, and building customer trust remain important considerations in both countries. Collaborations between traditional banks and fintech firms are also expected to drive the growth of digital lending in the UK.

Conclusion

Digital lending has experienced substantial growth and transformation on a global scale, with our focus being on UK and India. This overview will outline the main drivers of this growth, the obstacles faced by the industry, and the regulatory landscape surrounding digital lending. Digital lending refers to providing loans through online platforms, bypassing traditional financial institutions. It has expanded significantly due to several factors. Firstly, technological advancements and the widespread use of smartphones have made financial services easily accessible, increasing digital connectivity. This has created a favourable environment for the flourishing of digital lending.

Furthermore, digital lending offers numerous advantages over traditional lending. It enables faster loan approval processes, streamlined operations, and reduced overhead costs, empowering lenders to provide competitive interest rates and enhance customer experiences. Moreover, digital lending platforms often leverage alternative data sources and advanced analytics to evaluate creditworthiness, expanding access to credit for underserved populations.

In the UK, digital lending has experienced remarkable growth. Fintech companies have emerged as key players in the market, offering innovative lending solutions. These firms utilize technology to simplify application and approval processes, cater to niche markets, and provide personalized loan products. The UK’s robust regulatory framework, overseen by the Financial Conduct Authority, has played a vital role in creating an enabling environment for digital lending growth.

In India, digital lending has undergone exponential growth driven by various factors. The widespread adoption of smartphones and the government’s initiatives for financial inclusion, such as Aadhaar (a biometric identification system) and Jan Dhan Yojana (a financial inclusion program), have propelled digital lending. Fintech platforms in India employ advanced data analytics, machine learning, and artificial intelligence to make credit decisions quickly and efficiently.

Despite its growth, the digital lending industry faces challenges. One significant concern is data security and privacy. The handling of sensitive financial and personal information necessitates robust cybersecurity measures to safeguard against data breaches. Additionally, managing credit risk and preventing fraudulent activities present ongoing challenges for lenders. Regulatory frameworks ensure consumer protection and foster a stable lending environment. Both the UK and India have implemented specific regulatory measures for digital lending. The Financial Conduct Authority regulates digital lending platforms in the UK to ensure fair lending practices and protect consumers. In India, the Reserve Bank of India oversees digital lending platforms, enforcing reasonable practices and establishing guidelines on interest rates and collection practices.

In conclusion, digital lending has experienced remarkable global growth and evolution. Technological advancements via increased digital connectivity, and improved credit accessibility, have contributed to this expansion. In the UK and India, digital lending has thrived due to supportive regulatory environments and the adoption of innovative technologies. However, challenges persist in data security, credit risk management, and fraud prevention, necessitating ongoing attention from industry participants and regulators.

Bibliography

Agarwal, S. and Zhang, J. (2020). FinTech, lending and payment innovation: A review. Asia‐Pacific Journal of Financial Studies, 49(3), pp.353-367.

Alber, N. and Dabour, M. (2020). The dynamic relationship between FinTech and social distancing under COVID-19 pandemic: Digital payments evidence. International Journal of Economics and Finance, 12(11).

Aye, T. (2020). Adoption of Fintech and Policy Recommendations: The Case For Digital Lending Platform in Myanmar.

Basha, M.M.J., Gupta, A., Raphael, P.D., Rajeev, V. and KVS, R.R. (2021). The Role of Digital Platforms in Revolutionizing the Lending Sector. International Journal of Innovative Research, 10(6).

Bank of England (2021). New forms of digital money. Bank of England official online publication, https://www.bankofengland.co.uk/paper/2021/new-forms-of-digital-money.

Bank of England (2022). Responses to the Bank of England’s Discussion Paper on new forms of digital money. Bank of England official online publication, https://www.bankofengland.co.uk/paper/2022/responses-to-the-bank-of-englands-discussion-paper-on-new-forms-of-digital-money.

Bank of England (2023). The digital pound: Technology Working Paper. Bank of England official online publication, https://www.bankofengland.co.uk/paper/2023/the-digital-pound-technology-working-paper.

BBC News. (2021). Buy now, pay later: UK tightens rules to protect consumers. Retrieved from https://www.bbc.com/news/business-55823225.

Bhattacharya, Megha (2020). 5 innovative FinTechs in the UK lending ecosystem. IBS Intelligence, https://ibsintelligence.com/ibsi-news/5-innovative-fintechs-in-the-uk-lending-ecosystem/.

Boston Consulting Group (2018). Global Challengers in Banking: India’s Digital Journey. Retrieved from https://www.bcg.com/publications/2018/global-challengers-banking-india-digital-journey.aspx.

Bundhun, R. (2023). Why India is experiencing a digital lending boom. N Business, https://www.thenationalnews.com/business/technology/2023/01/09/why-india-is-experiencing-a-digital-lending-boom/.

Busines Wire (2022). UK Digital Lending Platform Market to Reach $3.05 Billion by 2027 at a CAGR 2027 – ResearchAndMarkets.com. Business Wire, https://www.businesswire.com/news/home/20220722005132/en/UK-Digital-Lending-Platform-Market-to-Reach-3.05-Billion-by-2027-at-a-CAGR-2027—ResearchAndMarkets.com.

Butler, Ben (2023). British Business Bank Agrees Initial £175M ENABLE Guarantee. Insider Media, https://www.insidermedia.com/news/national/british-business-bank-agrees-initial-175m-enable-guarantee.

Cambridge Centre for Alternative Finance (2021). The United Kingdom Alternative Finance Report 2021.

Chakrabarty, Amitava (2022). How digital lending took off in 2022 and its future, scenario in 2023. Financial Express, https://www.financialexpress.com/money/how-digital-lending-took-off-in-2022-and-its-future-scenario-in-2023/2923882/.

Chen, A. J., Even-Tov, O., Kang, J. K., & Wittenberg-Moerman, R. (2023). Digital Lending and Financial Well-Being: Evidence from a Developing Economy.

Cornelli, G., Frost, J., Gambacorta, L., Rau, R., Wardrop, R. and Ziegler, T. (2021). Fintech and big tech credit: What explains the rise of digital lending?. In CESifo Forum (Vol. 22, No. 02, pp. 30-34). München: ifo Institut-Leibniz-Institut für Wirtschaftsforschung an der Universität München.

Cornelli, G., Frost, J., Gambacorta, L., Rau, P.R., Wardrop, R. and Ziegler, T. (2023). Fintech and big tech credit: Drivers of the growth of digital lending. Journal of Banking & Finance, 148, p.106742.

Correa, David (2023). Peer to Peer Lending Market Size, Current and Future Trends, Demand and Growth Rate of 29.7%. Newswires, https://www.einnews.com/pr_news/633751645/peer-to-peer-lending-market-size-current-and-future-trends-demand-and-growth-rate-of-29-7.

Damodaran, S., Kavin, S., Keerthi, K.U., Madhumathi, J. and Mythili, P.V. (2019). Empowering MSMEs through digital lending. In 2019 International Conference on Digitization (ICD) (pp. 249-253). IEEE.

Dietz, M. G., Kincses, A. and Ahmad, F. (2023). Value creation in banking. Mckinsey and Company, https://www.mckinsey.com/industries/financial-services/our-insights/banking-matters/value-creation-in-banking-a-cross-cycle-view-of-economic-value-generation-by-product-segment.

Dixit, Nimayi (2019). Double-Digit Growth, Complex Bank Relationships Lie Ahead For US Digital Lenders. S&P Global, https://www.spglobal.com/marketintelligence/en/news-insights/research/doubldigit-growth-complex-bank-relationships-lie-ahead-for-us-digital-lenders.

Dupas, P., Robinson, J. and Brailovskaya, V. (2022). The impact of digital credit in low-income countries. CEPR, https://cepr.org/voxeu/columns/impact-digital-credit-low-income-countries.

Elsaid, H.M. (2021). A review of literature directions regarding the impact of fintech firms on the banking industry. Qualitative Research in Financial Markets, (ahead-of-print).

Experian (2023). Fintech-led Digital Lending: Coming of Age. Experian Working Paper.

FCA (2019). FCA confirms new rules for P2P platforms. FCA, https://www.fca.org.uk/news/press-releases/fca-confirms-new-rules-p2p-platforms.

Finextra (2017). NatWest unveils online lending platform for SMEs. Finextra, https://www.finextra.com/newsarticle/30145/natwest-unveils-online-lending-platform-for-smes.

Finextra (2022). LHV UK to buy SME lending business of Bank North. Finextra, https://www.finextra.com/newsarticle/41109/lhv-uk-to-buy-sme-lending-business-of-bank-north.

Fintech Finance (2023). Banks Reining in SME Lending According to Iwoca Report. Fintech Finance News, https://ffnews.com/newsarticle/fintech/banks-reining-in-sme-lending-according-to-iwoca-report/.

Gaw, Kathryn (2022). Lenders urged to look for early signs of borrower distress. Peer2Peer Finance News, https://p2pfinancenews.co.uk/2022/11/15/lenders-urged-to-look-for-early-signs-of-borrower-distress/.

Gomber, P., Koch, J.A. and Siering, M. (2017). Digital Finance and FinTech: current research and future research directions. Journal of Business Economics, 87, pp.537-580.

Gong, Q., Liu, C., Peng, Q., & Wang, L. (2020). Will CEOs with banking experience lower default risks? Evidence from P2P lending platforms in China. Finance Research Letters, 36, 101461.

González Páramo, J.M. (2017). Financial innovation in the digital age: Challenges for regulation and supervision. Revista de estabilidad financiera. Nº 32 (mayo 2017), p. 9-37.

Green, Rachel (2019). HSBC launched a digital lending platform for online personal loans. Business Insider, https://www.businessinsider.com/hsbc-launches-new-digital-lending-platform-2019-8?r=US&IR=T.

Gu, Dingwei, Gui, Zhengqing and Huang, Yangguang (2022). Fintech Market and Regulation: Lessons from China’s Peer-to-peer Lending Platforms. HKUST Business School Research Paper No. 2022-065.

Gupta, Neeta (2019). Impact PSD2 will have on the Lending Industry. Medium, https://medium.com/akeo-tech/impact-psd2-will-have-on-the-lending-industry-2de8b9b7330c.

Hendarta, E., Sardjana, M. K., Kurnia, J. and Dewanda, E. P. (2022). Indonesia: Revamping the Peer-to-Peer Lending Industry. Global Compliance News, https://www.globalcompliancenews.com/2022/08/09/indonesia-revamping-the-peer-to-peer-lending-industry-29072022/.

Hendriyani, C. and Raharja, S.U.J. (2019). Business agility strategy: Peer-to-peer lending of Fintech startup in the era of digital finance in Indonesia. Review of Integrative Business and Economics Research, 8, pp.239-246.

HES Fintech (2022). White paper: Digital lending – how technology transforms banks. Fintech Futures, https://www.fintechfutures.com/2022/05/whitepaper-digital-lending-how-technology-transforms-banks/.

Huang, L., & Pontell, H. N. (2023). Crime and crisis in China’s P2P online lending market: a comparative analysis of fraud. Crime, Law and Social Change, 79(4), 369-393.

Huang, R. H. (2018). Online P2P lending and regulatory responses in China: Opportunities and challenges. European Business Organization Law Review, 19, 63-92.

Insights, A. (2018). Demystifying Digital Lending. How Digital Transformation Can Help Financial Service Providers Reach New Customers, Drive Engagement, and Promote Financial Inclusion.

Johnen, C. (2023). Financial Inclusion in Kenya: The Role of Mobile Financial Services.

Kagan, Julia (2023). What Is Peer-to-Peer (P2P) Lending? Definition and How It Works. Investopedia, https://www.investopedia.com/terms/p/peer-to-peer-lending.asp.

Kale, S. (2021). Digital Lending: Issues, Challenges and Proposed Solutions-April 2021.

Kandpal, V. and Mehrotra, R. (2019). Financial inclusion: The role of fintech and digital financial services in India. Indian Journal of Economics & Business, 19(1), pp.85-93.

Karaman, H.D., Savaser, T., Tiniç, M. and Tumer-Alkan, G. (2021). Financial technology in developing economies: A note on digital lending in Turkey. Economics Letters, 207, p.110012.

Kashyap, Hermant (2022). Digital Lending To Become A $1.3 Tn Market By 2030 In India. Inc42, https://inc42.com/buzz/digital-lending-become-1-3-tn-market-2030-india/.

Khairnar, Shruti (2022). OakNorth Bank buys 50% stake in specialist lender ASK Partners. Fintech Futures, https://www.fintechfutures.com/2022/10/oaknorth-bank-buys-50-stake-in-specialist-lender-ask-partners/.

Klein, A. (2020). China’s digital payments revolution. Brookings Institution, Washington.

Kleinman, Mark (2023). Former Funding Circle exec raises £7m for SME lending start-up Triver. Sky News, https://news.sky.com/story/former-funding-circle-exec-raises-7m-for-sme-lending-start-up-triver-12858982.

KPMG (2019). Fintech and Startups Fueling India’s USD 5 Trillion Economy. KPMG Report.

Krauser, Lilia (2022). Digital lending leads the way. Zendesk Blog, https://www.zendesk.co.uk/blog/digital-lending-leads-the-way/.

Kuchminskaya, T. (2022). What’s New in the Digital Lending Market in 2022? (Digital lending trends). Finextra, https://www.finextra.com/blogposting/22115/whats-new-in-the-digital-lending-market-in-2022-digital-lending-trends.

Kuziemko, C. (2021). Top 10 UK Fintech Lending Companies to Follow in 2021. STX Next, https://www.stxnext.com/blog/top-uk-fintech-lending-companies/.

Langley, P., Anderson, B., Ash, J. and Gordon, R. (2019). Indebted life and money culture: Payday lending in the United Kingdom. Economy and Society, 48(1), pp.30-51.

Mastropietro, F. and Blini, L. (2022). Why digital lending is the future for banks and SMEs. EY.

Mathi, S. (2023). Summary: RBI Issues Clarifications On Digital Lending Guidelines. Medianama, https://www.medianama.com/2023/02/223-rbi-faqs-digital-lending-guidelines/.

Mckinsey & Company (2019). The power of digital lending. Mckinsey & Company, https://www.mckinsey.com/industries/financial-services/our-insights/banking-matters/the-power-of-digital-lending.

Morgan, R. (2017). The top FinTech trends driving the next decade. American Bankers Association. ABA Banking Journal, 109(5), p.22.

Muli, A.K. (2020). Digital lending in Kenya; the case for regulation (Doctoral dissertation, Strathmore University).

Neuwirth, Suzie (2022). Zopa’s P2P brand sold and rebranded as Plata Finance. P2P Finance News, https://p2pfinancenews.co.uk/2022/07/08/zopas-p2p-brand-sold-and-rebranded-as-plata-finance/.