Executive Summary

- The emergence of neo-banks in India and the UK reflects the increasing demand for digital financial services. The dawn of the digital age in the financial sector has paved the way for increased alliances between incumbents and ‘fintech’ organizations.

- Neo-banks, digital-only banks that operate primarily through mobile apps, have significantly impacted the financial sector in recent years. They are leveraging technologies such as artificial intelligence and machine learning to provide personalized financial solutions to customers.

- Over the last four years, nearly 36 neo-banks in India have been competing, acquiring customers, and creating a niche in the banking and financial sector. Similarly, in the UK, the three major neo-banks (Monzo, Revolut and Starling bank) are actively trying to gain a foothold in the banking industry.

Problem Statement

- Despite noteworthy gains, neo-banks are still subject to challenges and hurdles which pose a threat to their growth, sustainability, and public reputation. Several risks and threats highlighted in the paper include the threat of cyber-security and the lack of technological advancement in developing regions which hinder business performance.

- Other challenges directed at neo-banks include low investor confidence and low profit margins resulting in risk of default: problems exacerbated by the fragile and volatile nature of the current banking and financial services industries.

Role of Regulation

- To mitigate risks posed by these challenges, the role of regulators emerges as significant. Regulating bodies ensure adequate supervision and monitoring of neo-banks, providing a base of support through features such as regulatory sandboxes.

- In India, neo-banks provide financial services by partnering with licensed banks, as the Reserve Bank of India guidelines do not allow for complete digitalisation of banks. In the UK, a mix of organic licensing & partnerships had been the erstwhile strategies used by the neo-banks to enter markets.

- Despite their innovative nature, there are observable differences in the applicability and evolution of regulatory sandboxes across the two economies in consideration.

Table of Contents

| S. No. | Topic | Page No. |

| 1 | Introduction | 4 |

| 2.1 | Global Neo-bank Emergence | |

| 2.2 | Neo-bank Classification and Evolution | 5-7 |

| 2.3 | Payment Banks in India | 7-8 |

| 2.4 | Indian Neo-banks – Market Outlook | 8-11 |

| 2.5 | Market Drivers of Neo-banks in India | 11-12 |

| 2.6 | Best Practice Case Studies – India | 13 |

| 2.7 | UK Neo-banks – Market Outlook | 14-17 |

| 2.8 | Best Practice Case Studies – UK | 17 |

| 3 | Challenges for Neo-banks | 18-19 |

| 4.1 | Regulatory Framework | 20-21 |

| 4.2 | Regulatory Sandboxes | 23-24 |

| 4.3 | Regulatory Sandbox Comparison: UK vs India | 24-25 |

| 5 | Conclusion | 26 |

| 6 | Bibliography | 27-30 |

| 7 | Appendix | 31 |

Introduction

The banking and financial services industry has undergone significant changes and transformations with the advent of technology. Structured around the fundamental principles of managing monetary deposits and advances, the banking industry’s flirtation with technological progress has yielded improvements in both product proposition and delivery channels; encompassing an emerging digital landscape in which consumers can access a plethora of banking solutions via smartphones and electronic devices. The integration of technology has enabled banks and financial institutions to offer customers more convenient and efficient services while improving their operational efficiency and reducing costs.

One of the key areas where technology has had a significant impact is the development of digital banking channels. With the rise of smartphones and other electronic devices, consumers can access a wide range of banking services and products, including online banking, mobile banking, and digital wallets. These channels have made it easier for customers to manage their accounts, complete transactions, and access financial information from anywhere.

Banks and NBFC (Non-Banking Financial Companies) are investing heavily in Research & Development (R&D) capabilities with which to improve their digital, front-end offering to upcoming generations of consumers who prefer electronic services as compared to traditional bank offerings (Nocera, 2022). Keeping in line with this trend, an emerging wave of digital banks is threatening to challenge the dominion held over the financial and banking sectors by large, traditional banks (Doshi, 2021). Starting as a concept in the early 2000’s and fuelled by the global financial crisis and resulting distrust of traditional banks (2007-2008), digital banks have expanded at an accelerated pace over the last decade; particularly in large economies such as India and the UK (Sutton, 2023).

Chief among these new entities is a concept termed ‘Neo-bank’: a strictly online-only bank offering all services exclusively in the digital format (Team TMS, 2022). While neo-banks have been popular among audiences switching to digital platforms, their contrasting experiences in different economies have fuelled both scepticism regarding dynamics such as expansion, profitability, threat of competition and saturation, as well as optimism based on overall potential.

In catering to visible hurdles and challenges in the global application and acceptance of digital banking services, the role of regulatory authorities is outlined as pivotal. The strength of regulation via applicable laws and policies, as well as the ability to successfully enforce these regulations, can define the successful integration and expansion of digital banks in the financial sectors of an economy. In addition to assessing the digital banking landscapes across both India and the UK, the strengths and practices of regulatory authorities are also analysed in order to determine best practices. A key component of the regulatory measures is a concept termed ‘Regulatory Sandboxes’ which could serve as a vital element for neo-bank growth and sustainability across developed and developing countries alike.

Global Neo-bank Emergence

Neo-banks have emerged globally due to a combination of factors, including advancements in technology, changes in consumer behaviour, and regulatory reforms. They have become a growing part of the global financial industry through an ability to offer a customer-centric, digitally focused banking experience. This industry has experienced significant growth globally, both in terms of total players and size of their respective customer bases.

Neo-banks gained momentum in the US over the past decade: growth chiefly supported by regulatory reforms and technological advancements. The Office of the Comptroller of the Currency (OCC, 2018) issued a special-purpose national bank charter for fintech companies in 2018. This charter allowed fintech companies to operate nationally without banking licenses. The US can be classified as a technological powerhouse, home to some of the leading technology companies: many having entered the banking market. In 2018, Google, for instance, launched Google Pay, which allows users to make payments and manage their money (Baxi, 2019). Consumer demand also played an important part, as many American consumers view traditional banking as outdated and inconvenient. Chime, one of the largest neo-banks in the US, reported over 12 million accounts in 2021 (Chime, 2021).

Europe has served as another hub of significant growth for the neo-bank industry. Like the US, regulatory reforms paved the way for this expansion. In 2018, the European Union implemented the Second Payment Services Directive (PSD2), which requires banks to expand their payment infrastructure to third-party providers. This has facilitated the emergence of neo-banks, yielding their access to customer data. Advancements in technology are evident, as Europe is home to leading fintech companies. Revolut, a leading neo-bank founded in the UK in 2015, has since expanded to over 35 countries. Neo-banks have attracted several customers, particularly younger generations which value convenience and innovation. N26, a German neo-bank, reported over 7 million customers in 2021 (N26, 2021).

Though this growth was prevalent in developed economies, recent recessionary pressures, and low investor confidence, among other factors, have put neo-banks in a precarious position (Dawkins, 2020). While neo-banks are emerging in developing countries, the same threats are applicable in those markets: depicting a vulnerable industry in need of reform (Bakhtar, 2023).

Neo-banks Classification and Evolution

As the evolution of the digital banking industry is relatively recent, with the phenomenon being in its preliminary stages as compared to the legacy of traditional banking, the exact classification of ‘Digital Banks’ and ‘Neo-banks’ is often difficult, with both terms being used interchangeably. As per generally accepted terminology, neo-banks are classified as banks exclusively offering online services and solutions, serving as a subset of digital banking organizations (Noronha, 2022). This positions a neo-bank as a direct competitor to the traditional bank.

Some noteworthy features exclusive to neo-banks include the following:

- Customers can perform banking transactions entirely from smartphones and computers,

- Accessible by everyone at any time regardless of location through respective electronic devices, (example being the N26 paperless sign-up process which takes up to eight minutes and is an end-to-end digital process),

- Digitalizing all aspects of banking (financing, loans, investments, and insurance),

- Incurring lower cost overheads due to digital operations resulting in lower fees.

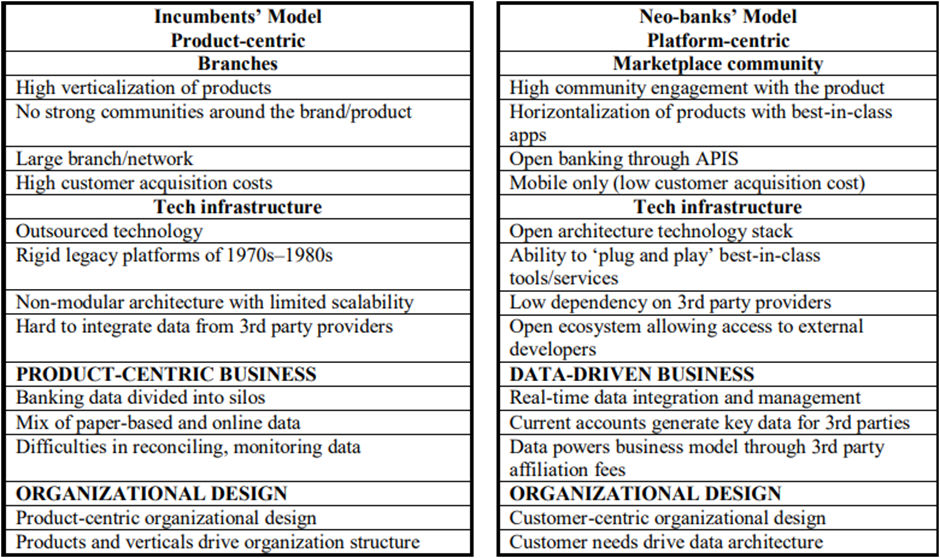

Digital banking organizations, holistically, offer a wide variety of digital services via alternative channels that can even take the form of branch-based ATM’s and automated kiosks. Digital banks can also partner with incumbent banks to provide fintech enabled services. Under this model, financial services are provided via a sponsored banking license (Ballard, 2018). The nature and scope of these digital organizations, including neo-banks, however, varies in different economies. Keeping this in mind, this paper observes the evolution and growth of neo-banks and associated digital banking services in India, an emerging economy, as well as the UK, a developed economy (Walden and Strohm, 2021).

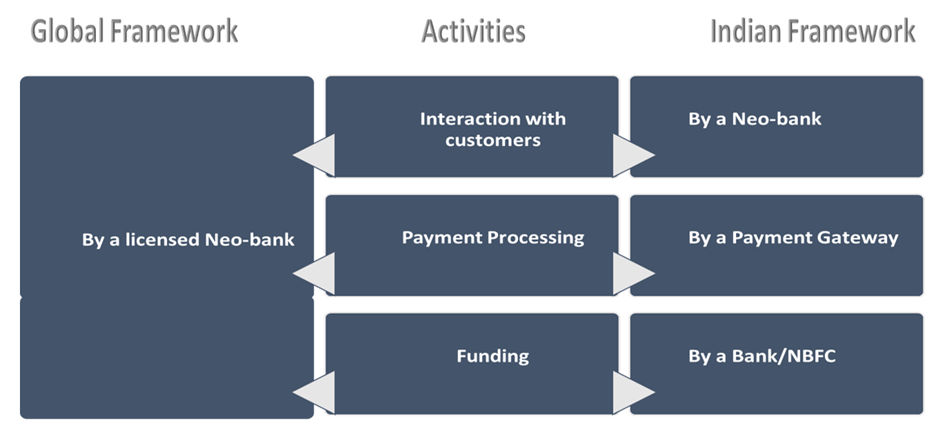

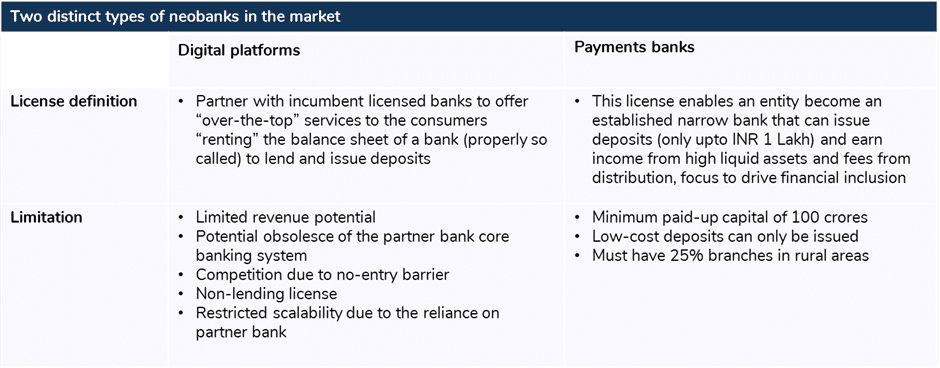

In India, there are instances of payment banks categorised as new age ‘neo-banks’ that nevertheless maintain at least a 25% physical footprint. This classification of activities being catered by different institutions is demonstrated in Figure 1 and illustrates the emerging yet hybrid nature of the neo-bank in India. As opposed to global framework emphasizing end-to-end operational control by neo-bank management, their respective dependencies on other financial institutions in the Indian economy is a cause of concern to be addressed.

In contrast, owing to the earlier emergence of digital banking solutions, the UK has established itself as a hub for fintech services and is host to neo-banks which are fully functional organizations capable of facilitating end-to-end business needs without the need for traditional bank partnership (Temelkov, 2020). These organizational capabilities are illustrated in Table 1 below, showcasing the relative strengths which the Neo-banking model possesses (open tech architecture, real-time data integration and customer-centric design) in contrast to the traditional model.

These features are evident in several leading neo-banks in the country, with prime examples including Starling Bank, Monzo, Revolut, Monese, Tandem Bank and Atom (Pay Space, 2020). There are differing trajectories and scope of operations exhibited by each organization. Starling and Monzo serving as dedicated online banks, though limited in operations to the UK, while Monese has expanded operations to more than thirty overseas markets.

Revolut awaits a digital banking license as of 2023, having offered online services prior to that without a license (Isaac, 2023). Tandem Bank provides a digital platform for consumers looking to use their own bank accounts rather than opening a new account for them, while Atom provides its own account opening services though of a limited nature. These characteristics further contribute to the advanced nature of the British fintech infrastructure (WhiteSight, 2020), while also stress upon the loosely defined nature of neo-banks and digital banks in general. A closer look at neo-bank sectors in both Indian and British economies is then essential to further grasp the concept.

Payments Banks in India

In order to understand the depth of fintech infrastructure in India, neo-banks must be analysed under the domain of ‘Payments Banks’. These institutions, offering exclusive online services, are slowly gaining significant recognition. They are recognised as ‘Payments Banks’ under Section 22 of the Banking Regulation Act, 1949. While these banks can accept current account deposits, and savings account deposits of up to INR 100,000, issue ATM or debit cards, and offer retail and intra-banking transactions services; they cannot issue loans, credit cards or other forms of advances toward customers and clients alike (Gupta, 2020).

In 2019, however, Paytm – a poignant example of a payments bank – collaborated with Citibank to launch the country’s first unlimited cashback credit card, offered to limited customers based on their digital behaviour. This initiated a growing trend of partnering with traditional banking organizations in order to provide respective services. While attractive, this model prevented the financial sector from expanding its customer base further as, in order to access services provided by a payments bank, customers must have had an existing bank account with a traditional bank (Goel, 2020). To counter this, in December 2019, the Reserve Bank of India issued guidelines for on-tap licensing of Small Finance Banks (SFBs) in the private sector. This manoeuvre allowed for targeting unserved and underserved small business units and micro industries, giving rise to the full-fledged neo-bank (Mohapatra, 2021).

RBI backed guidelines enabled payments banks, such as Fino, Airtel and Paytm, as well as Non-Banking Financial Companies (NBFCs) to apply for an official licence. Despite encouraging improvements, the regulations imposed by the Indian government posed a series of limitations on the performance of neo-banks. Full-fledged Payments Banks were subject to a track record of conducting business for 5 years in addition to a minimum paid-up capital of INR 200 crore (2 Bn) while organizations offering digital platforms by partnering with traditional banks are subject to structural limitations marked by an inability to lend and susceptible to competition (Shashidhar, 2020); features summarized in Table 2.

Indian Neo-banks – Market Outlook

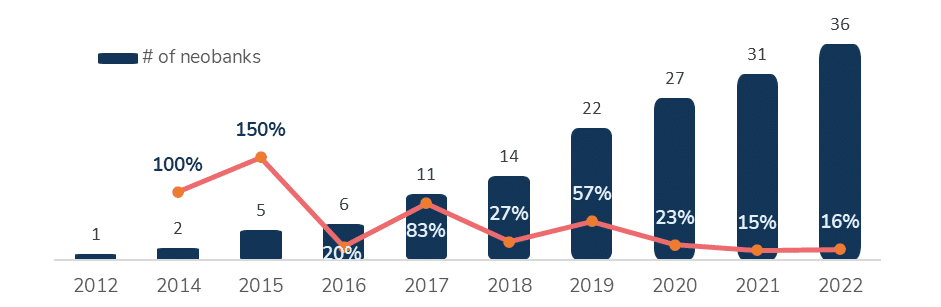

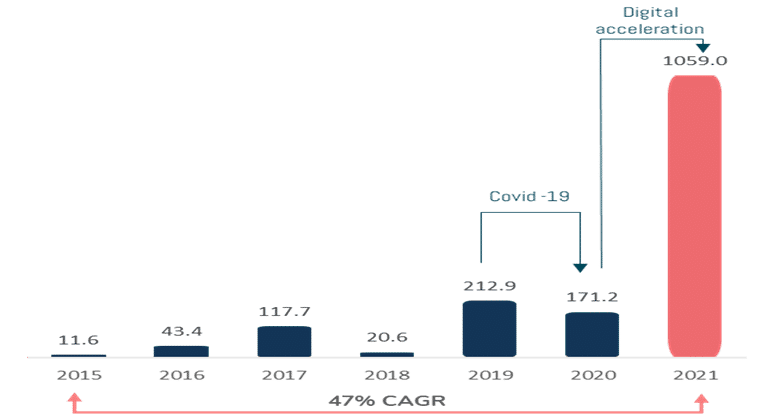

Given their recent introduction, a common observation deduced can be that Indian neo-banks have just scratched the surface, setting the stage for explosive future growth. Over the last four years, 36 neo-banks have been competing, acquiring customers, and creating a niche in the banking and financial sector (Joad, 2023). They are growing to 43% CAGR (Compound Annual Growth Rate), establishing a competitive ecosphere in digital banking (Figure 2).

In 2021, it is estimated that neo-banks acquired 350 million customers, with 290 million out of the total customers coming in from 47% of the neo-banks. Despite the ground-breaking success in fintech evolution brought about by neo-banks, as evidenced by the growth in their annual numbers, India’s significant hurdle lies in the lack of formal digital-only banking licenses (Gupta, 2020). As a result, standalone digital banks and challenger banks do not exist in the country. At the heart of the entire digital banking structure in India is the inability of the institution to function without a sponsored banking licence, which serves to distinguish between the global and Indian neo-banking models. As a result, partnering with traditional banks and have unconventionally fuelled the growth of India’s neo-banking sector.

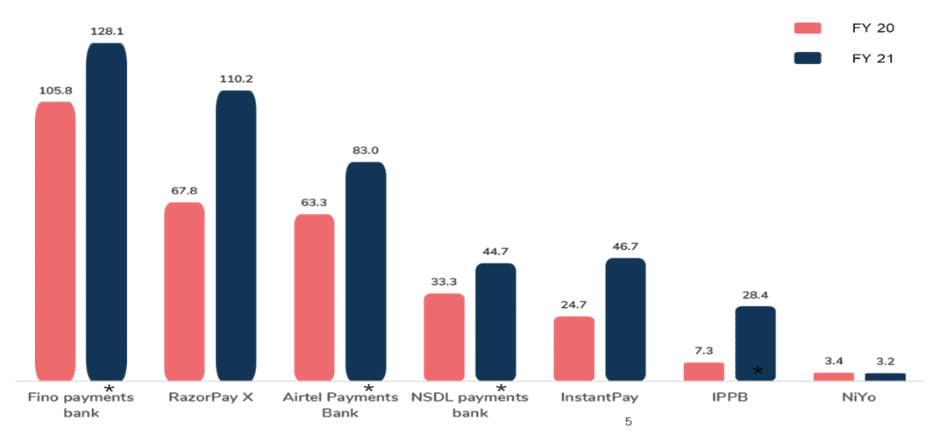

Fino Payments Bank is a poignant example of an Indian neo-bank success story, becoming the first APAC neo-bank to go public (Panchal, 2016). It successfully raised USD 150 Mn against a total valuation of US$ 700 Mn and reported annual revenues worth USD 128.1 Mn in 2021 (Figure 3). Given these impressive growth figures and growth in revenues exhibited across the board, the neo-bank market emerges as a potential hotspot for investors. Under the investment model, companies can expect a substantial influx of funding to come, as illustrated by the highest funding based on total valuation of USD 1.05 Bn in 2021 (Figure 3).

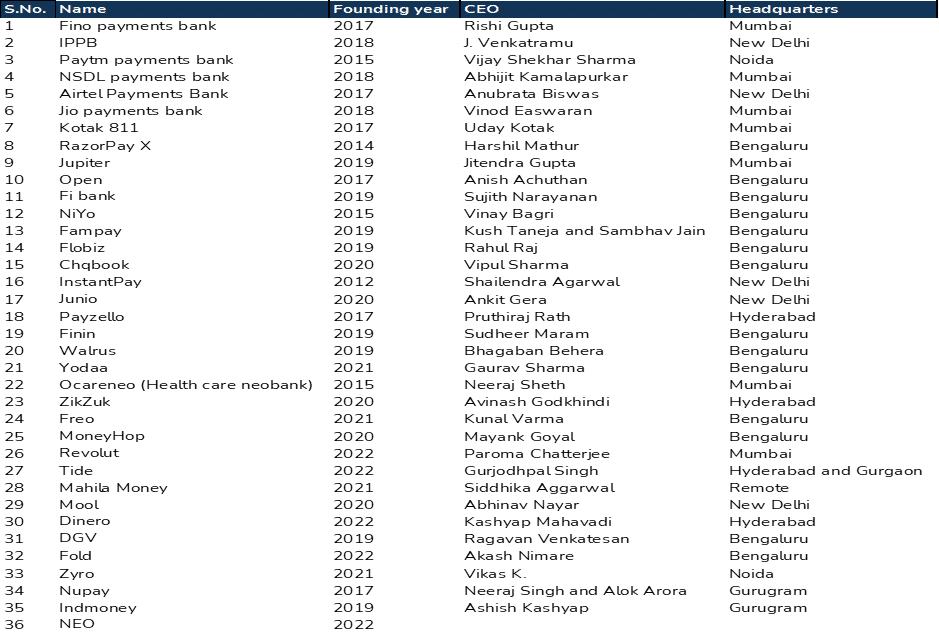

Examples of significantly funded Indian neo-banks include Jupiter, Open Financial Technologies, Razorpay, Fino Payments Bank and Niyo. In the last 7 years, neo-bank growth registered approximately 47% CAGR, with a slight dip in 2020 and backed by an exponential rise in 2021, as can be linked to Covid-19 pandemic induced fluctuations. These increments in funding value – illustrated in Figure 4 – portray a highly optimistic future for the neo-banking model in India as well as the global domain.

A close-up on snapshot of valuation for top-performing neo-banking companies reveals significant gains made by Razorpay and Open: two examples of popular neo-banks offering digital banking services to the Indian population at large. These recorded valuations were in excess of US$ 1.0 Bn as of 2021 (illustrated in Figure 5). This funding success is, in part, attributed to the aggressive funding strategies employed by both organizations.

Another important insight lies in the target market and customer base preferred by these neo-banks, as Razorpay and Open both focus on SME clients in addition to retail segments; highlighting the potential that can be realized by extending digital banking solutions to businesses and commercial clients as well as individual consumers (MSME Desk, 2022). These figures showcase potential for further expansion and increased funding in the neo-bank and fintech sectors for the World’s most populated and one of the largest economies.

Market Drivers for Neo-banks in India

Considering various market dynamics and customer needs, six key drivers can be recommended to fill gaps in conventional banking, ushering in a new age for digital platforms to improve customer lives. A number of these drivers, particularly financial inclusion, open banking technology and data monetisation, have matured in the context of the Indian economy while others need further improvement. An overview of these drivers and their respective components is provided below.

- Financial inclusion

- Access to multiple financial products and services at low costs,

- Avenues to seek financial credit based on personal need and capability,

- Generate annualised interest income over and above core earnings.

- Regulatory initiatives

- Create a favourable environment to establish and operate digital banks,

- Boost economic prosperity by creating jobs in IT, banking, and fintech domains.

- Open banking technology

- Allow data sharing ease with third-party providers for an efficient marketplace,

- Enable providers (insurance, wealth) to attach services to banking products.

- Data monetization

- Use data from social media, e-commerce activity to build personalised products,

- Integrate databases with banking interface for efficient customer remediation.

- Non-traditional competitors

- Low to no-entry barriers for non-banking players to establish a digital bank,

- Influx of telecom and tech companies in the banking and financial industries,

- Create stiff competition driven by product innovation and customer experience.

- Cloud technology

- Divestiture from monolithic legacy infrastructure to agile, scalable platforms,

- Quick and secure access to core banking backend and frontend interfaces.

One of the main benefits of the Indian strategy of partnering with core financial and banking companies manifests in neo-banks thriving on these partner ecosystems. Banking as a service (BaaS) is now a strong revenue strategy for incumbents, which as a result are white labelling their financial solutions. Meanwhile, neo-banks are building products and services over these solutions with a revenue-based strategy composed of fee-based income from third-party merchant partnerships (Joad, 2023).

Though these benefits are noteworthy, the limitations highlighted with the partnership model are also considerable, with stringent regulations preventing long-term profitability and sustainability of payments banks. Sponsored traditional banking licenses allow a neo-bank to open accounts, establish UPI and QR-based payment channels, and accept deposits.

To further enrich the product portfolio, they can also rely on strategic partnerships with insurance and lending companies, with noteworthy examples including top insurance players such as Bharati AXA, Tata AIA, Aviva, Birla Sun Life, Punjab National Bank, Kotak Life Insurance, ICICI Prudential Life Insurance, and Bajaj Allianz (Khairnar, 2023). This highlights the need for the central bank and associated authorities to consider this proposal in the future.

Best Practice Case Studies – India

1. Niyo Global – https://goniyo.com/

The strategy of success for Niyo Global has been to boost customer wealth with robo-advisory and integrated tools. Niyo bank has over 4 million individual users processing more than USD 3 Bn of transactions annually, valued at approximately USD 134 Mn (2020) and USD 3.2 Mn in revenue (2021) (Pugh, 2022).

- Bite sized wealth management – helps its users invest in mutual funds and domestic equities with its popular features like zero percent forex markup and invest the change, which rounds up a customer’s spending and invests a part of it.

- Banking the underbanked – provides zero-balance prepaid cards for blue-collar workers. It also issues travel cards in partnership with SBM and DCB Bank.

- Driving growth with partner ecosystem – acquired Bengaluru-based startup Index to boost its wealth management platform (2021) and mutual fund startup Goalwise (2020).

2. Fampay – https://fampay.in/

Fampay, unlike Niyo, prioritized a policy structured around the young adults segment, an example being digitalising piggy banks for teens. FamPay has over 5 million individual users and has been averaging a 100% month on month growth (Hariharan, 2021).

- Building products to support teens – focuses on a niche customer segment. The saving account, debit card, spending analytics are all customised to complement.

- Focus on security – created a product that empowers teenagers with financial independence and gives parents the choice to monitor their child’s transactions. The physical debit card is a numberless card and transactions are managed through the app.

- FamPay community – provides an in-app exclusive community to help them learn, earn, and grow. The community conducts regular engagement activities such as ‘test your financial knowledge’ quiz, ask an expert, and look for relevant courses.

3. Paytm payments bank – https://paytm.com/

A third case study focuses on one of the largest payments bank in India. As a strategy for enlarging and enriching its customer base, Paytm focused on creating a one stop-shop for customer’s financial needs. Paytm payments bank has over 100 million users, with more added every month (Rai, 2023).

- A unique value proposition – created an end-to-end products stack with personalised and gamified value-added financial services such as insurance, credit services, and expense management tools to make the customer’s journey more holistic.

- Ecosystem strategy – built an entire consumer ecosystem where users can manage their lives end to end without having to flip through a host of apps.

- Strong background – being the largest e wallet player in the country, Paytm enjoys the advantage of default conversion of existing wallet customers into account holders.

UK Neo-banks Market Outlook

On the other side of the development and geographical sphere, in UK a monumental loss in consumer confidence for traditional banks can still be felt; owing to instances of recent cyber-attacks which led to a reduction in operations by seven large banks (Ring, 2017; Collinson, 2017). Further impact on consumer confidence was brought about by the global financial crisis of 2007-2008 and resulting government-backed bailouts of large banks (The Economist, 2019).

To bring about change in a 150-year-old long consumer perception of banks and financial institutions could be a difficult task. However, recent development, marred by incidents of low consumer confidence discussed, possibly allowed for an expedited revolution in the banking and financial sectors. These developments further benefitted from an open regulatory environment, though the resulting situation of significant market saturation also makes it harder for new players to enter the digital banking market (Kumar and Chakraborty, 2022).

As it stands, there are more than 20 neo-banks functioning in the UK, with a few of these registered in Ireland, Germany, Netherlands, Hongkong, France and Finland. Monzo, Starling Bank, Revolut and Monese are commonly cited as the top performing banks, with Wise, Monzo and Revolut included in the top 15 neo-banks in the US. Furthermore, in terms of rankings, Atom Bank, Wise, Monzo, Oaknorth, Revolut, Starling Bank, Curve, Monese are all in the top 20 neo-banks in the Europe. These examples showcase the advanced fintech and neo-banking landscape in the country and its regional surroundings (England, 2023).

Despite developments in the UK fintech economy, there is room for significant expansion. The three largest UK neo-banks – Revolut, Monzo, and N26 – have a combined customer base of just 2.5 million, while Lloyds – the largest traditional bank – has 30 million clients. Understanding this under-representation highlights a core problem of trust. Despite public reservations regarding traditional banks and their inability to provide best value for money, they are trusted enough to keep customer money safe. However, this claim is further subject to revision owing to increasing risk posed by lacks in cyber-security. With a progressive regulatory landscape, the UK emerged as ground-zero for digital-focused challenger banks such as Monzo, Starling and Revolut which aimed to win customers in a market dominated by the big 4 traditional banks (HSBC, Lloyds, Barclays, NatWest) (Livingston, 2022).

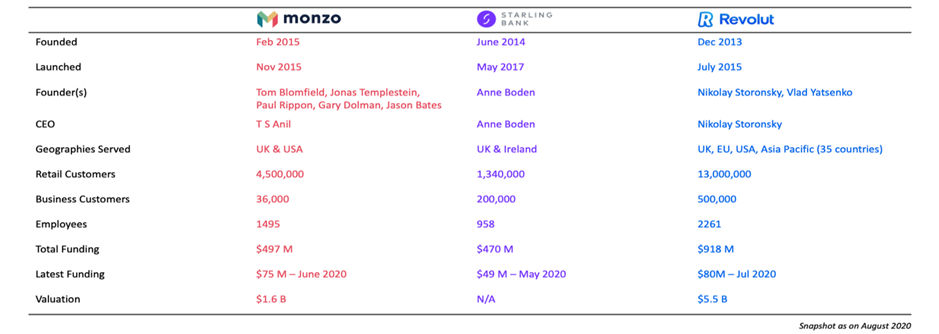

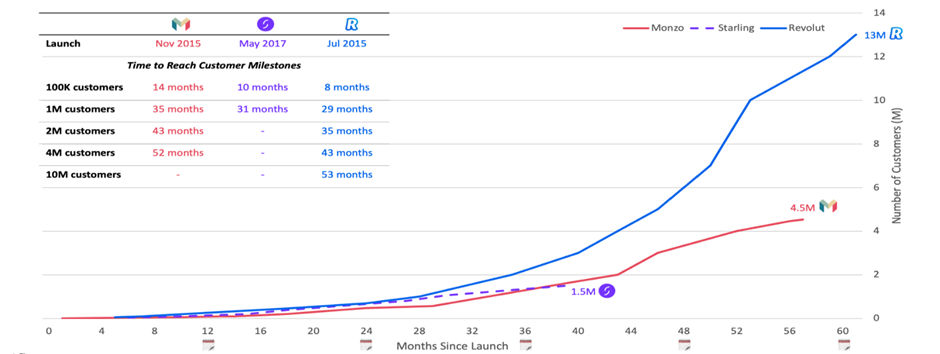

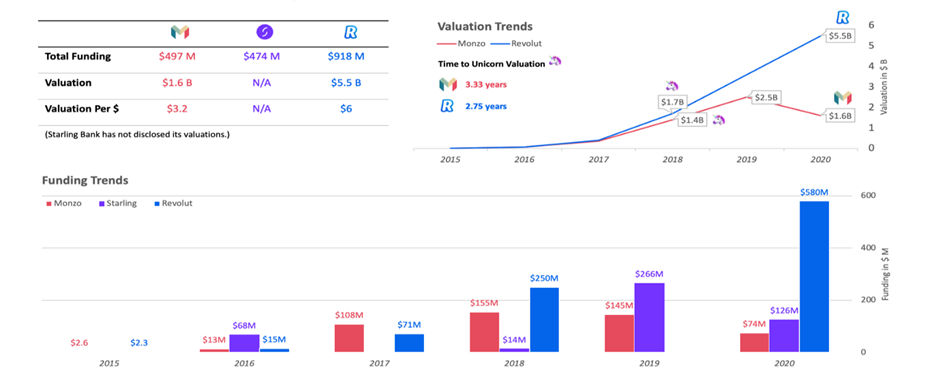

Table 4 compares three large neo-banks in the UK, showing different strategies of operations by each in terms of markets served. Revolut’s aim of emerging as a global neo-bank stands in contrast to the Starling Bank strategy of only serving in the British Isles (Mason, 2023). Figure 6 showcases gains by Revolut in achieving the fastest customer milestones and enjoying exponential customer growth aided by rapid expansion. Starling bank is shown as the second fastest neo-bank to acquire 1 million users.

Revolut is also classified as the most funded and most valued neo-bank in the comparison. It witnessed a 3x jump in valuation to US$ 5.5 Bn in a recent fundraise, while Monzo conversely witnessed a 40% downgrade to total valuation of US$ 1.6 Bn (Figure 7). Compared to the four UK traditional banks, neo-banks lag in terms of pure-play financial metrics like net interest margin and loan deposits. While their revenue growth is high, they operate at net loss due to high operating expenses, a cause for concern considering future sustainability (Pantos, 2023).

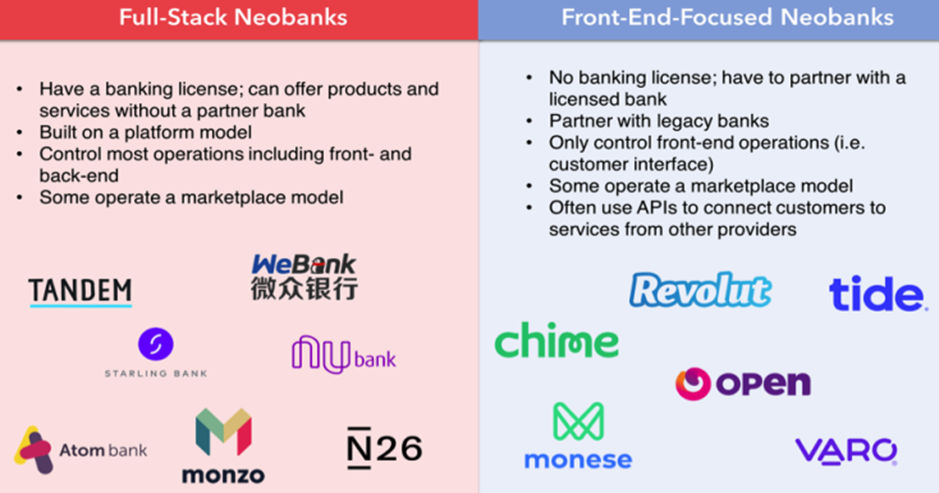

In comparison to the Indian model of partner banks offering digital services by liaising with traditional banks, British fintech regulations allow for neo-banks to apply for full-fledged banking licenses. However, as stressed upon through examples of UK neo-banks, different structures and objectives have resulted in two categories: full-stack and front-end-focused. Table 4 shows examples of each category, along with their respective features. The categorization of Monese, Open and Tide as front-end-focused neo-banks (Revolut awaits an imminent banking license) highlights their respective business models as suited for growth and sustainability via partnerships with licensed and legacy banks (Rogers, 2021).

In the discussion on pros and cons of a full-stack neo-bank with a banking license as opposed to a front-end partnering company, there is perhaps not one definite winner. Both systems have been applied to great success in the UK. In India, while the latter definitely has achieved great success, it remains to be seen whether neo-banks can emulate the same by functioning independently; subject to the government’s decision to start issuing digital banking licenses.

Best Practice Case Studies – UK

1. Starling Bank – https://www.starlingbank.com/

Started in 2014, the bank was envisioned as a full-fledged digital bank offering financial solutions and services. Starling Bank offers several services suited to customer and business needs alike (Cocheo, 2021; Hendelmann, 2021).

- Banking-as-a-Service – provides end-to-end services helping customers manage day-to-day tasks, goals, and financial expectations.

- Regional specialization – the bank aims to establish a strong footprint in the UK and entrench its customer base in the country with no immediate plans of rapid expansion.

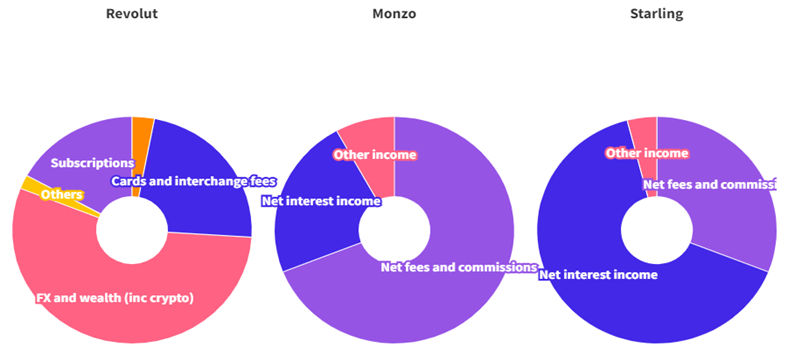

- Multiple revenue streams – income is earned through a variety of services, including subscriptions; interchange fees; interest, overdraft, transfer, and referral fees.

2. Revolut – https://www.revolut.com/en-BE/

Founded in 2015, Revolut has favoured an expansive approach, entering overseas markets including Europe and the US while operating without a banking license until recently.

- Payments leader – designed and launched Revolut Pay with the aim of becoming a leader in the payments industry and preferred platform for merchants and businesses.

- Multinational presence – operating in 28 countries to date, the fintech player is close to becoming a global leader in fintech services (Mason, 2023; Reynolds, 2022).

Challenges for Neo-banks

Despite emerging prospects for fintech and digital banking services worldwide, there are significant challenges for neo-banks to cope with. Profitability is a major challenge, proving difficult for a majority of startups. Most neo-banks with a sponsored banking license do not have full customer ownership and work on revenue-sharing models with incumbents, resulting in paper-thin operating margins, as has been highlighted as a recurring theme of the partnership model. In addition, operational control under a partnership model is also restricted as there is significant intervention by the partnering legacy bank which, in most cases, has greater autonomy and decision-making authority. There are also default and insolvency risks associated with this model as the negative performance of a partnering bank can impact the results of the neo-bank, although this can also impact in the opposite manner (Temelkov, 2020).

In the Indian context, drawbacks aside, payments banks enjoy greater flexibility and autonomy. They can create a loan book with high CASA ratios, accelerating their revenue contribution. As per the latest figures, payments banks reported an average net profit of USD 3.0 Mn. Fino Payments Bank and Airtel Payments Bank earned highest net profits in 2021, with USD 2.73 Mn and USD 5.8 Mn, respectively (Gupta, 2020).

Conversely, even the full-stack model is susceptible to obstacles. Due to pricing their services below cost to attract new customers and investing significantly in licencing, UK neo-banks like Monzo and Starling are struggling to achieve break-even points. Revoult, the first neo-bank to achieve a monthly break-even point, is unable to monetize their service (O’Brien, 2023). Neo-banks must figure out a method to efficiently monetize their service while continuing to be a compelling alternative if they aim to continue competing in the long run. This raises the crucial question of whether neo-banks must just acquire more customers in order to become profitable, or whether they must fundamentally alter their business model (Bakhtar, 2023).

Lack of relative capital is another problem. Despite the fact that neo-banks are drawing significant investment, such as USD 250 Mn raised by Revoult last year, this amount is little in comparison to the funding available to traditional banks. It seems doubtful whether neo-banks will be able to effectively compete in the long run when traditional banks have much more capital to invest unless they can either attract significantly more investment or develop a truly distinctive product (Paige, 2023). This problem is echoed across neo-banks in Europe (Dawkins, 2020) and is attributed to the shutdown of German company ‘Hufsy’, ‘Soon’ in France and ‘Zuno’ in the Czech Republic (Dadan and Singh, 2022); highlighting the fragile nature of the industry in general.

Holistically, there are additional challenges which impact the neo-banking and digital banking sectors, as well as the fintech sector at large. One of the prime threats takes the form of increased instances of cyber-attacks and cyber-crime which can severely impact consumer confidence. These attacks can also result in operational losses that many fledgling neo-banks can be unable to contain resulting in bankruptcy and insolvency. Since neo-banks operate on a strictly online basis, with little to no physical presence, they are more susceptible to these threats compared to traditional banks and must have adequate security investment and measures in place to tackle such problems (Koibichuk, 2021).

The success of neo-banks is contingent upon the technological prowess of an economy. Technological infrastructure must be advanced enough to encompass digital payments, strong network coverage and a consumer segment proficient in using digital services (Sung and Leong, 2019). In developing economies, such as India, this can prove a major hurdle. Despite improvements in education and infrastructural development, these problems are still visible. As a result, widespread acceptance of neo-banking services is elusive. This problem reverberates across societies not yet classified as ‘cash-less’ (Okunevych and Hlivecka, 2018).

As far as the threat of competition is concerned, neo-banks face resistance from traditional banks which are also embracing, launching, and advancing their own digital platforms for end-to-end services and solutions that can enable customer retention and business growth. The inevitable saturation of service providers in the financial markets can subsequently stifle profits and reduce the motivation for business expansion (Nurbaev et. al., 2022).

In the highly volatile and uncertain fintech industry, forecasting future growth and profitability for any neo-bank can be a challenge. The novice industry is already marred by instances of fraud, bankruptcy, and insolvency, as reflected in the collapse of crypto-currency giant FTX in 2022 (Hern and Milmo, 2022). Even traditional commercial banks are not immune to the threats of operating in the financial sector, as witnessed by the collapse and subsequent acquisition of Silicon Valley Bank in the US in early 2023 (Elliott, 2023) and Swiss banking giant Credit Suisse (Levine, 2023); both incidents occurring in early 2023. This depicts a grim financial landscape through which at-risk neo-banks must navigate.

Keeping these concerns in mind, it is the role of the regulator, which is of vital importance, ensuring neo-banks are protected substantially in order to protect their interests, as well as those of the customers they serve (Louis and Jang, 2022). Understanding the regulatory framework across UK and India, can help evaluate relative strengths and weaknesses for further improvement.

Regulatory Framework

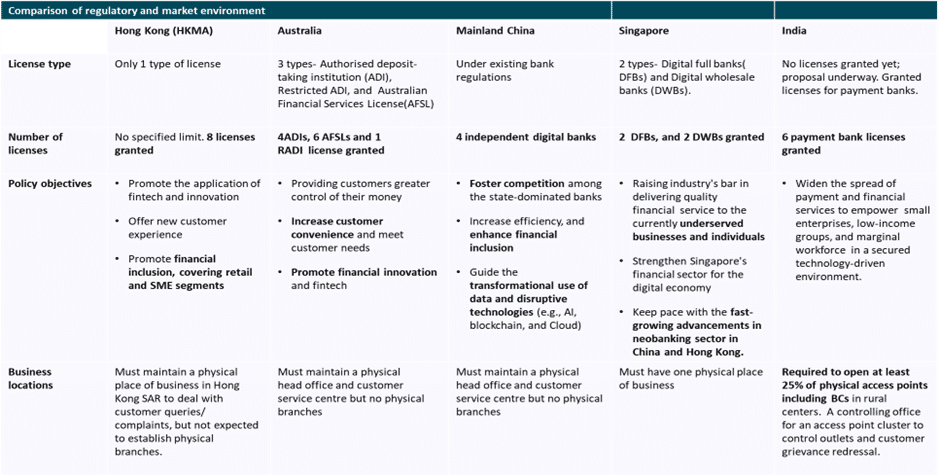

The success and expansion of fintech and neo-bank companies depends largely on the quality of regulations exhibited in the hosting economy. Effective regulations can protect neo-banks and the fintech sector from many of the challenges, threats and risks identified. In addition, they can also protect customer rights and privileges by making the businesses comply with set norms and practices. Table 6 illustrates the regulatory landscape for neo-banks in leading Asia Pacific economies; highlighting the underdevelopment in licensing capabilities by India as compared to Hong Kong, Australia, China, and Singapore. A key observation is the requirement by Indian neo-banks to maintain a physical operational presence, unlike in other economies where physical presence is limited to a corporate office.

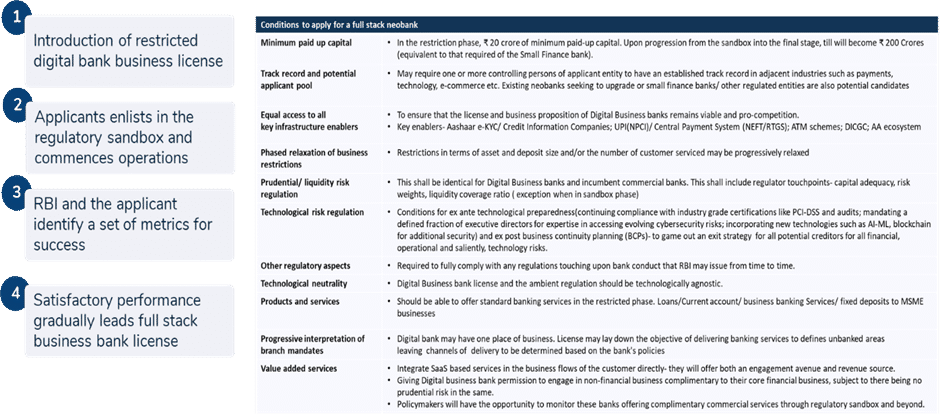

NITI Aayog, the apex public policy think-tank of the Government of India, drafted a licensing policy that will allow the RBI (Reserve Bank of India) to grant digital banking licenses. This draft, and the underlying policy, is under review, with a formal policy expected to be released imminently. Illustrated in Table 7, it is contingent on a step-by-step process that enables limited initial operations followed by full stack business performance subject to applicants meeting the required criteria set by the evaluator.

This phenomenon gives light to a core component of the regulatory process i.e., the ‘Regulatory Sandbox’. For most business startups and new ventures, a recurring issue manifests as the volatility associated with initial business operations. If not managed correctly, they can result in early defaults, acquisitions and resulting closures. In this regard, a gradual process of business evaluation through initial limitations and gradual ease of restrictions can achieve better results for the business. Hence, Regulatory Sandboxes can be as beneficial for the businesses in emerging from the initial volatile phase as they can be for the regulators in ensuring compliance (Brown and Piroska, 2022).

In addition to having a robust policy for guaranteeing effective supervision and monitoring of neo-banks, there must be an authority responsible and capable of performing these duties. The Reserve Bank of India (RBI) and its UK counterpart, the Financial Conduct Authority (FCA) are both institutions responsible for enacting these duties. In addition to laws and policies exclusive to neo-banks, other relevant circulars which have been issued over time which can have implications for their performance (Lauren, 2022). The RBI has issued several circulars in this regard which regulate aspects of the neo-bank sector, such as the need for a license, managing risk and ensuring data protection (overview in appendix).

Regulatory Sandboxes

As previously touched upon, Regulatory Sandboxes (RS) allow for firms/innovators to test their regulated financial product with real consumers for a short period of time. Testing occurs under the supervision of the regulator, with the aim being to enable faster development and deployment of regulated financial products into the market while ensuring that consumer interests are protected (Vanamali, 2022).

There are several objectives with which regulatory sandboxes can aim to boost development in fintech and neo-bank industries (Goo and Heo, 2020), encompassing the following:

- Identify consumer protection safeguards to be built into new products,

- Enable viability test to identify the impact of business model in the market,

- Enable a cheaper option to test and bring the product to market,

- Enable faster rollouts.

Regulatory Sandboxes are a distinct feature as compared to full-fledged licenses. They are designed for the testing of ‘innovative products’ in the market that may require certain regulations to be waived or introduced for consumer benefit. In this regard, they yield a number of benefits for the parties involved.

Sandboxes allow firms to live test products in the market under ‘restricted authorisation’. These tests have well defined parameters that allow for any unforeseen failures to be contained to a small section of the market. For example, the number of customers that the firm can sell to maybe restricted during the test period. Firms can test and tweak their innovative and untested products while allowing regulators to monitor their implications and consider regulatory changes for the benefit of consumers (Kapoor, 2021).

Regulatory Sandbox Comparison: UK vs India

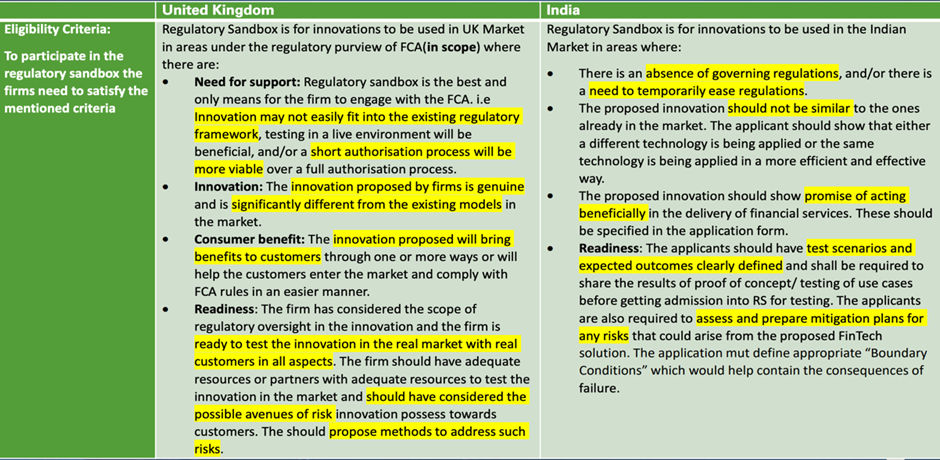

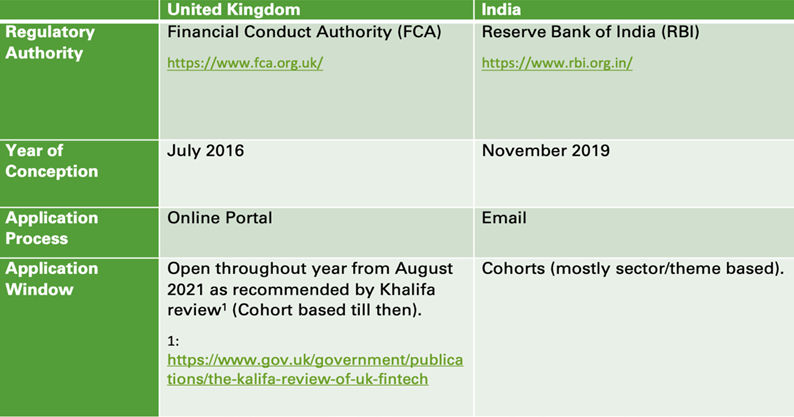

Ignoring differences in tone in reports between FCA and RBI, there are a few major differences between RS in India and the UK. Sandboxes in the UK are currently open throughout the year and are open to diverse set of themes and sectors (Hall, 2021). RS in India, however, are mostly theme/sector based. Furthermore, there is a minimum capital requirement for participation in India. While it has been stated in the RBI’s Enabling Framework for RS that this may be waived, it has also been stated that this would be considered as an important and necessary condition when a large number of firms apply to participate in RS during a particular cohort.

The FCA mentions features like ‘Signposting’, ‘Informal Steer’, and ‘Individual Guidance’ being available to firms. RBI’s Enabling Framework for RS doesn’t mention any such tools being available for applicants. In India, the RBI had issued a ‘Draft Enabling Framework for Regulatory Sandbox’ in 2018 which in turn was refined into ’Enabling Framework for Regulatory Sandbox’ in 2019 after receiving feedback from the general public. The RBI employs RS technique for assessing the performance of new financial innovations and test its acceptance among the target customers or general public. This was used as preliminary test for issuing licenses to ‘Small Finance Banks’ and ‘Payments Banks’ (Mohapatra, 2021).

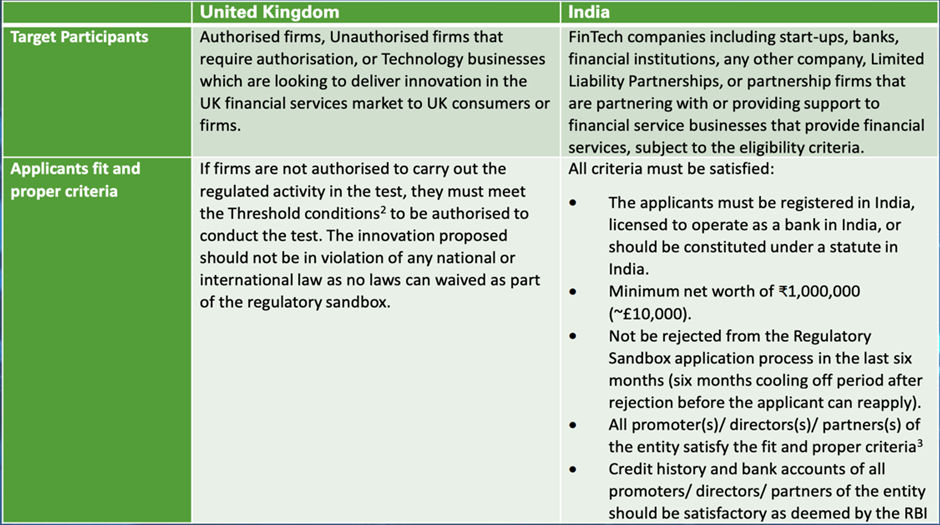

In the UK, RS are applicable in areas where there is innovation, readiness, need for support and intervention and a general sense of consumer benefit from protection by regulation (Brear, 2019). These elements are also evident, though in less detail, in the Indian model. As far as the eligibility criteria is concerned, RS in the UK instructs participants to meet the threshold conditions as part of an eligibility criteria. In comparison, the eligibility criteria for a financial startup to be part of RS in India is more specific (Shashidhar, 2020) and defined as below:

- Net worth of at least INR 1.0 Mn,

- Satisfactory credit score / history of promoters and directors,

- Promoters and directors of the entity meeting the prescribed ‘fit and proper’ criteria.

Further details of the overall eligibility criteria and applicant profiles are provided in the appendix. From an overall perspective, RS in both countries is loosely defined for the same objectives. However, while it has been established that they seek to grow the fintech sector, there are claims to the contrary amid calls for eased regulation and relaxation of stringent policies in both economies.

In order to stimulate growth of neo-banks in the UK, the British government faces calls to ‘break the chains’ of financial regulation (Hornstein, 2022). The ‘financial services and markets’ bill, structured during Britain’s EU membership, which will partially replace the regulatory framework for the finance industry, is now being passed in the UK. The government may take advantage of the new bill to get rid of regulatory barriers for banking startups (Schilling de Carvalho, 2022).

Similarly, the RBI also faces calls for eased restrictions, although they are less frequent in a fintech landscape which is not yet that defined or expansive. The main criticism manifests in a call for the government to ease the mandatory criteria of having minimum physical branches for issuing full-fledged digital banking licenses (Gupta, 2020).

Conclusion

The global fintech industry is continuously evolving – subject to the endless possibilities technological advancements can yield. At the same time, it is also highly volatile and vulnerable to various risks and threats. These threats range from specific impacts such as cyber-attacks and lack of consumer and investor confidence, to global prevailing events such as the continuing fall-out from the Covid-19 pandemic, inflation and the cost-of-living crisis, and the Ukraine war and resulting political blocs. Keeping these risks in mind, a sustainable and prosperous future of the fledgling global neo-bank sector cannot be conclusively determined.

With the increased threat of competition from traditional legacy banks and their efforts to embrace the digital revolution, it cannot even be maintained that neo-banks can successfully dismantle traditional banks as the leader in the banking industry. However, there are indications to be optimistic, as evidenced from the substantial in both numbers of neo-banks and their customer bases across two economies: India and the UK. In catering to an ever-growing population of tech-savvy consumers, neo-banks can benefit from tremendous business potential. Partnering with NBFC’s offering a host of financial solutions can also enable neo-banks to diversify revenue streams while ensuring customer retention as a one-stop platform.

As far as the preferred neo-banking model is concerned, there are both benefits and drawbacks associated with either being a full-stack online-bank or entering into a partnership with a traditional bank in a front-end capacity. This is maintained in analysing examples of both types of neo-banks in the UK, while also scrutinizing the partnership model which is prevalent in India. A better approach for any new business venture then would be to thoroughly scrutinise the prevailing market conditions as well as internal factors before making an informed decision on organizational structure and strategy (Rocchi, 2022).

In safeguarding the sustainability and growth of neo-banks, while also ensuring customer safety through effective supervision and monitoring, the role of regulatory authorities is of prime importance. Through the ‘Regulatory Sandbox’ approach, both the FCA in the UK and the RBI in India stand to gain by fostering neo-banks in their infancy and allowing them to develop as a business. In India, the next step for neo-banks and regulator alike, is the introduction of full-stack digital banking licenses to enable further fintech penetration in the worlds most populated country. Though promising, the exact outcome of this venture remains to be seen.

Bibliography

Cocheo, S. (2021). Starling Bank’s Dead-Serious Strategy: Growing Into a Megabank Rival. The Financial Brand, https://thefinancialbrand.com/news/fintech-banking/starling-banks-dead-serious-strategy-growing-into-a-megabank-rival-anne-boden-neobank-fintech-119499/.

Collinson, Patrick (2017). Alleged mastermind behind bank cyber-attacks extradited to UK. The Guardian, https://www.theguardian.com/uk-news/2017/aug/30/alleged-mastermind-daniel-kaye-lloyds-bank-cyber-attacks-extradited-uk.

Bakhtar, M. (2023). Is the neobank bubble about to burst?. Fintech Magazine, https://fintechmagazine.com/articles/is-the-neobank-bubble-about-to-burst.

Ballard, Barclay (2018). The unstoppable rise of neobanks. World Finance, https://www.worldfinance.com/banking/the-unstoppable-rise-of-neobanks.

Brear, D. M. (2019). What the U.S. Can Learn from U.K. Fintechs and Neobanks. The Financial Brand, https://thefinancialbrand.com/news/digital-banking/challenger-bank-neobank-fintech-regulator-sandbox-89922/.

Brown, E. and Piroska, D. (2022) Governing Fintech and Fintech as Governance: The Regulatory Sandbox, Riskwashing, and Disruptive Social Classification, New Political Economy, 27:1, 19-32, DOI: 10.1080/13563467.2021.1910645

Doshi, S. (2021). Neo-banks: disruption at play?. KPMG Special Report, https://kpmg.com/in/en/home/insights/2021/08/neo-banks-digital-customer-client-experience-disruption-mantra.html.

Elliott, L. (2023). SVB collapse presents central banks with a big headache. The Guardian, https://www.theguardian.com/business/2023/mar/14/svb-collapse-presents-central-banks-with-a-big-headache.

England, J. (2023). Europe’s neobanks are outpacing legacy banks in app adoption. Fintech Magazine, https://fintechmagazine.com/banking/europes-neobanks-are-outpacing-legacy-banks-in-app-adoption.

Finnovate (2018). Neo-Banks: Performance and New Ideas, Finnovate Research – Ideas for financial innovation, October 2018.

Gahlot, S. (2021). Neo-banks and their confluence with India’s Financial Landscape. Vinod Kothari Consultants, https://vinodkothari.com/2021/12/neo-banks-and-their-confluence-with-indias-financial-landscape/.

Goel, V. (2020). India, the new hub of neobanks. Twimbit, https://twimbit.com/insights/india-the-new-hub-of-neobanks.

Goo, J.J. and Heo, J.Y. (2020). The impact of the regulatory sandbox on the fintech industry, with a discussion on the relation between regulatory sandboxes and open innovation. Journal of Open Innovation: Technology, Market, and Complexity, 6(2), p.43.

Gupta, H. (2020). What are Neobanks & Payment banks?. Medium, https://medium.com/@g.hemant2007/what-are-neobanks-payments-bank-7f0f6c800c3c#:~:text=Neobanks%20are%20the%20financial%20institutions,physical%20branches%2C%20unlike%20traditional%20banks.

Hall, Ian (2021). UK regulatory sandbox shifts to ‘always open’ status. Global Government Fintech, https://www.globalgovernmentfintech.com/uk-regulatory-sandbox-shifts-to-always-open-status/.

Hariharan, Sindhu (2021). Fintech startup FamPay raises $38 million in Series A. Times of India, https://timesofindia.indiatimes.com/business/india-business/fintech-startup-fampay-raises-38-million-in-series-a/articleshow/83565550.cms.

Hendelmann, V. (2021). The Starling Bank Business Model – How Does Starling Bank Make Money?. Product Mint, https://productmint.com/starling-bank-business-model-how-does-starling-bank-make-money/#:~:text=Starling%20Bank%20makes%20money%20via,U.K.’s%20leading%20challenger%20banks.

Hern, A. and Milmo, D. (2022). What do we know so far about collapse of crypto exchange FTX?. The Guardian, https://www.theguardian.com/technology/2022/nov/18/how-did-crypto-firm-ftx-collapse.

Hornstein, O. (2022). UK must ‘break chains’ of regulation to boost neobanks say MPs. UKTN, https://www.uktech.news/fintech/neobanks-regulation-mps-20220831.

Isaac, A. (2023). Fintech firm Revolut moves closer to UK banking licence after first annual profit. The Guardian, https://www.theguardian.com/business/2023/mar/01/uk-fintech-firm-revolut-much-delayed-accounts-reveal-first-annual-profit.

Joad, U. (2023). What are the Top 15 Neo-banks in India?. Fi Money, https://fi.money/blog/posts/what-are-the-top-15-neo-banks-in-india.

Kapoor, Sheersh (2021). Regulatory Sandbox Explained: How RBI is moderating FinTechs’ disruption in BFSI. ETBFSI, BFSI.com from The Economic Times, https://bfsi.economictimes.indiatimes.com/news/policy/regulatory-sandbox-explained-how-rbi-is-moderating-fintechs-disruption-in-bfsi/87098591.

Khairnar, S. (2023). New “cross-border neobank” in India: moneyHOP. Fintech Futures, https://www.fintechfutures.com/2023/02/new-cross-border-neobank-moneyhop-launches-in-india/.

Koibichuk, V. (2021). Innovation technology and cyber frauds risks of neobanks: gravity model analysis. Marketing i menedžment innovacij.

Kumar, S. and Chakraborty, R. (2022). The UK Big Banks’ Bet on FinTech. WhiteSight, https://www.whitesight.net/post/the-uk-big-banks-bet-on-fintech.

Lauren, F.A.H.Y. (2022). Regulator reputation and stakeholder participation: A case study of the UK’s regulatory sandbox for fintech. European Journal of Risk Regulation, 13(1), pp.138-157.

Livingston, Z. (2022). UK Neobanks: A Summer of Highs and No’s. E Week UK, https://www.eweekuk.com/fintech/uk-neobanks-analysis-summer2022/.

Louis, J.E. and Jang, B. (2022). A Comparative Legal Study on Neobank Between South Korea and Indonesia. Journal of Law and Policy Transformation, 7(1), pp.109-123.

Mason, E. (2023). Neobank Revolut Reports Profitable 2021 After Audit Criticism. Forbes, https://www.forbes.com/sites/emilymason/2023/03/02/neobank-revolut-reports-profitable-2021-after-audit-criticism/?sh=2c7051176b23.

Mohapatra, Karunakar (2021). RBI Regulatory Sandbox is Shaping the Future of Indian Banking. FinExtra, https://www.finextra.com/blogposting/22907/rbi-regulatory-sandbox-is-shaping-the-future-of-indian-banking.

MSME Desk (2022). Neobank for SMEs Open joins Razorpay, Mswipe, others to get RBI approval for payment aggregator license. Financial Express, https://www.financialexpress.com/industry/sme/neobank-for-smes-open-joins-razorpay-mswipe-others-to-get-rbi-approval-for-payment-aggregator-license/2812186/.

Nocera, G. (2022). Fintech revolution and traditional banks-what factors influence members of generation Z to place their trust in Fintech companies, specifically neobanks, over traditional banks as banking and financial service providers?: a case study on the banking application of the Swiss neobank Yuh.

Noronha, G. (2022). Neo Banking Vs Digital Banking. Fi Money, https://fi.money/blog/posts/neo-banking-vs-digital-banking#:~:text=The%20difference%20between%20neo%20banking,by%20providing%20suitable%20digital%20services.

Nurbaev, V., Au, C.H.A. and Chou, C.Y. (2022). Exploring the Critical Success Factors of Different Types of FinTech: A Beginning Case of Neobank.

O’Brien, A. (2023). Which UK neobank performed best in its latest results?. Sifted, https://sifted.eu/articles/uk-neobank-revolut-monzo-starling-financials/.

Okunevych, I.L. and Hlivecka, M.O. (2018). Neobank: bubble or paradigm shift?. Economic Bulletin of the National Mining University scientific journal, 61(61), pp.129-137.

Paige, W. (2023). Revolut and Varo face tumbling valuations as investor confidence in neobanks weakens. Insider Intelligence, https://www.insiderintelligence.com/content/revolut-varo-valuations-tumble.

Panchal, Salil (2016). FINO PayTech: The people’s bank. Forbes India, https://www.forbesindia.com/article/work-in-progress/fino-paytech-the-peoples-bank/44013/1.

Pantos, S. (2023). Designing Stress Tests for UK Fast-Growing Firms and Fintech. Risks, 11(2), p.31.

Pay Space Magazine (2020). Leading neobanks in the UK: top 6 digital-only banks. Pay Space Magazine, https://payspacemagazine.com/banks/leading-neobanks-in-the-uk-top-6-digital-only-banks/.

Pugh, Alex (2022). Indian neobank Niyo lands $100m Series C to boost product development. Fintech Futures, https://www.fintechfutures.com/2022/02/indian-neobank-niyo-lands-100m-series-c-to-boost-product-development/.

Rai, Saritha (2023). Paytm Posts Narrower Loss After Growth Push Boosts Sales. Bloomberg, https://www.bloomberg.com/news/articles/2023-02-03/paytm-posts-narrower-loss-after-growth-push-boosts-sales?leadSource=uverify%20wall.

Reynolds, J. (2022). Revolut aims to disrupt payments industry with Revolut Pay. Alt Fi, https://www.altfi.com/article/9816_revolut-disrupting-payments-industry-with-revolut-pay#:~:text=Nik%20Storonsky%2C%20co%2Dfounder%20%26,rapidly%20growing%20e%2Dcommerce%20market.

Ring, Suzi, (2017). U.K. Banks Aren’t Telling Regulators About All Cyber Attacks. Bloomberg, https://www.bloomberg.com/news/articles/2017-12-05/u-k-banks-aren-t-telling-regulators-about-all-cyber-attacks?leadSource=uverify%20wall.

Rocchi, J.M. (2022). How to Build a Leading So-Called Neobank and Pursue Its Growth?: The Case of the FinTech Nickel in Europe. In Cases on Digital Strategies and Management Issues in Modern Organizations (pp. 177-199). IGI Global.

Rogers, J. (2021). FinTech Disruption: What the impacts of Neobanks on the Irish retail banking consumer?.

Schilling de Carvalho, P. (2022). Retaining Influence in Post-Brexit International Financial Regulation: Lessons from the UK’s FinTech Framework. Journal of Financial Regulation, 8(1), pp.104-131.

Shashidhar, K.J. (2020). Regulatory sandboxes: decoding india’s attempt to regulate Fintech disruption. ORF Research Brief, Delhi.

Sung, A., Leong, K., Sironi, P., O’Reilly, T. and McMillan, A. (2019). An exploratory study of the FinTech (Financial Technology) education and retraining in UK. Journal of Work-Applied Management, 11(2), pp.187-198.

Sutton, J. (2023). The rise of the Neobanks in the UK. The Corporate Law Academy, https://www.thecorporatelawacademy.com/knowledge/the-rise-of-the-neobanks-in-the-uk/.

Team TMS (2022). What is a neobank?. Business Standard, https://www.business-standard.com/podcast/finance/what-is-a-neobank-122050600048_1.html.

Temelkov, Z. (2020). Differences between traditional bank model and fintech based digital bank and neobanks models. SocioBrains, International scientific refereed online journal with impact factor, (74), pp.8-15.

The Economist Special Report (2019). Neobanks are changing Britain’s banking landscape. The Economist, https://www.economist.com/special-report/2019/05/02/neobanks-are-changing-britains-banking-landscape?utm_medium=cpc.adword.pd&utm_source=google&ppccampaignID=18151738051&ppcadID=&utm_campaign=a.22brand_pmax&utm_content=conversion.direct-response.anonymou.

Vanamali, K. V. (2022). What is a regulatory sandbox?. Business-Standard, https://www.business-standard.com/podcast/economy-policy/what-is-a-regulatory-sandbox-122110800137_1.html.

Walden, Stephanie and Strohm, Mitch (2021). What Is A Neobank?. Forbes, https://www.forbes.com/advisor/banking/what-is-a-neobank/.

WhiteSight (2020). The UK Neo-Banks: A Comparative Analysis. WhiteSight, https://www.whitesight.net/post/the-uk-neo-banks-a-comparative-analysis.

Appendix

RBI Circulars

1. RBI Master Circular No. RBI/2016-17/17 on Mobile Banking transactions in India – Operative Guidelines for Banks dated 01.07.2016 (Master Circular on Mobile Banking Transactions)

Clause 6.1 of the Master Circular on Mobile Banking Transactions prohibits the provision of mobile banking services by those entities which are not licensed, supervised and without a physical presence in India.

As a resulting impact, neo-banks cannot provide mobile banking services independently as they do not possess a physical presence. Furthermore, they are not yet supervised or required to be licensed by the RBI.

2. RBI Master Circular No. RBI/2006/167 on Guidelines for Managing Risks and Code of Conduct in Outsourcing of Financial Services by Banks dated 03.11.2006 (Outsourcing Guidelines)

The Outsourcing Guidelines lay down a framework for managing the attendant risks in outsourcing of banking services by another entity, including neo-banks. They address a few risks associated with banks outsourcing financial services, to ensure that such banks maintain compliance with the requirements of RBI (maintenance of books, records, and information).

These guidelines resultingly direct banks to adopt sound and responsive risk management practices for effective oversight, due diligence, and management of risks arising from such outsourcing to neo-banks.

3. RBI Notification No. RBI/2010-11/217 on Guidelines for engaging of Business Correspondents dated 28.09.2010 (Guidelines for Business Correspondents)

The Guidelines for Business Correspondents enables banks to engage companies registered under the Companies Act, 1956/2013, excluding NBFCs, as business correspondents. Thus, the Guidelines for Business Correspondents enables neo-banks registered as a company to act as Business Correspondent for banks.

Various activities of a Business Correspondent are identified by the Guidelines, including identification of borrowers, preliminary processing of loan applications, submission of applications to banks, post-sanction monitoring, follow-up for recovery, and disbursal of small value credit. Neo-banks are predominantly engaged in such activities, and thus, would be governed by the requirements of the Guidelines for Business Correspondents.

4. RBI Notification No. RBI/2021-22/64 on Guidelines for Managing Risk in Outsourcing of Financial Services by Co-operative Banks dated 28.06.2021 (Outsourcing Guidelines for Co-op Banks)

The Outsourcing Guidelines for Co-op Banks stipulate the compliances to be followed by co-operative banks for outsourcing their financial activities to neo-banks in accordance with their obligation to both customers and the RBI.

These Guidelines have imposed restrictions on co-operative banks from outsourcing to neo-banks core management functions such as policy formulation, internal audit and compliance, compliance with KYC norms, credit sanction and investment management.

5. Information Technology Act, 2000 (IT Act) and the Information Technology (Reasonable Security Practices and Procedures and Sensitive Personal Data or Information) Rules, 2011 (IT Rules)

As neo-banks obtain, utilize, and communicate financial information of customers through online platforms to the banks, they are subject to the data protection compliances stipulated for Intermediaries under the IT Act.

Neo-banks are further required to maintain certain security standards as laid down by IT rules and ensure compliance with other mandates including implementing a privacy policy; mandatorily informing the user that their data is being collected and obtaining their explicit consent for collection of sensitive personal data; appointment of a grievance officer; enabling users to access, update and delete their information; and ensuring data collection as per law.

Regulatory Sandbox particulars for UK and India (Applicant Criteria, Eligibility Criteria).